Seven years ago, before pharmacy e-vouchers became mainstream, we brought on a new client quickly started hearing complaints from members. Their out-of-pocket costs at the pharmacy counter had gone up, and in some cases, the increase was significant. From the member’s perspective, the new pharmacy benefit looked worse. They were not thinking about rebates, net cost, formulary intent, or the employer’s fiduciary responsibility. They only knew they were paying more than they had paid before.

When we reviewed the claims, the issue became clear. Under the prior arrangement, manufacturer assistance had been quietly reducing member copays through e-vouchers and coupon like programs. The savings made the prescription feel cheaper to the member, but the plan was often paying more because the voucher helped keep the patient on a higher-cost brand drug. The member liked the lower copay, the manufacturer protected the brand, and the transaction looked smooth at the pharmacy counter. The employer was left with the higher total cost.

That experience changed the way I looked at pharmacy e-vouchers. They are marketed as a patient affordability tool and sometimes they do help a patient fill a medication they might otherwise abandon. But for self-funded employers, the story is more complicated. A lower copay at the counter does not automatically mean a lower cost for the plan. In many cases, the e-voucher improves the member’s short term experience while weakening the employer’s ability to manage the pharmacy benefit in the long term interest of the plan.

What Pharmacy e-Vouchers Really Do

A pharmacy e-voucher is a manufacturer-funded discount delivered electronically during the prescription claims process. Unlike an old fashioned paper coupon or a copay card the member has to present, the e-voucher can be applied automatically. The member may not know why the cost dropped. The pharmacist may only see the claim response. The employer may not see the full transaction details unless its reporting specifically captures manufacturer assistance at the claim level.

The important point is where the voucher sits in the transaction. In many arrangements, manufacturers place e-vouchers through switch operators or claims routing infrastructure. That allows the voucher to be triggered inside the electronic pharmacy claim, often before the employer has a clear view of what happened. The pharmacy counter is no longer the control point. The discount can be embedded upstream in the claims process, which makes it easier for the manufacturer’s strategy to influence the final outcome without much visibility to the plan sponsor.

To the member, this feels like a benefit. A prescription that may have cost $100, $250, or more suddenly costs $25. The member leaves the pharmacy satisfied and any plan design meant to create cost awareness loses its impact. But the plan may still be paying a much higher amount than it would have paid for a preferred generic, biosimilar, therapeutic alternative, or lower net cost brand drug. The member sees the savings. The employer absorbs the economics behind the curtain.

When Copay Relief Becomes Cost Shifting

The dark side of e-vouchers is not the discount itself. The dark side is the way the discount can separate the member’s out-of-pocket cost from the plan’s total cost. Once those two numbers are disconnected, members naturally make decisions based on what they pay at the pharmacy counter. They do not have access to the plan’s net cost. They are not expected to run a fiduciary analysis before picking up a prescription. They respond to the price placed in front of them.

Manufacturers understand this better than anyone. E-vouchers are not random acts of generosity. They are market access tools designed to reduce prescription abandonment, protect brand utilization, and soften the effect of formulary controls. If a drug is placed on a non-preferred tier or faces competition from a lower cost alternative, an e-voucher can make the higher cost drug feel like the better deal to the patient. The manufacturer keeps the prescription. The member gets a lower copay. The plan may pay more.

This is where self-funded employers get hurt. Employers spend real money building formularies, prior authorization criteria, step therapy rules, tiered copays, and other plan design features. Those tools are not meant to create friction for the sake of friction. They are intended to guide members toward clinically appropriate, cost-effective therapy. When an e-voucher overrides the financial signal built into the plan design, it can quietly pull utilization in the opposite direction.

This also explains why members may push back when an employer moves to a more transparent, fiduciary model. If the prior arrangement allowed e-vouchers to reduce member copays on expensive drugs, the old plan may have felt better to the member even when it was worse for the employer. That creates a communication challenge. The employer may be improving governance and lowering total plan cost, while some members only see that they now pay more at the counter for certain brand drugs.

Why Employers Often Miss the Problem

Most employers do not receive enough detail to evaluate e-vouchers properly. Standard pharmacy reporting may show gross cost, ingredient cost, dispensing fee, member cost share, rebates, and total plan paid amounts. But it may not clearly show whether an e-voucher was used, how much manufacturer assistance was applied, whether the assistance counted toward the deductible or out-of-pocket maximum, and whether the claim supported or undermined formulary intent.

That lack of visibility is not a minor reporting gap. It prevents the plan sponsor from understanding who influenced the claim and who benefited from the transaction. The manufacturer may have used the voucher to keep the member on its brand. A switch, coupon processor, PBM, pharmacy, accumulator vendor, or other party may have earned a fee somewhere in the workflow. The member may have received short term relief. The employer may have paid a higher total cost without seeing the full chain of events.

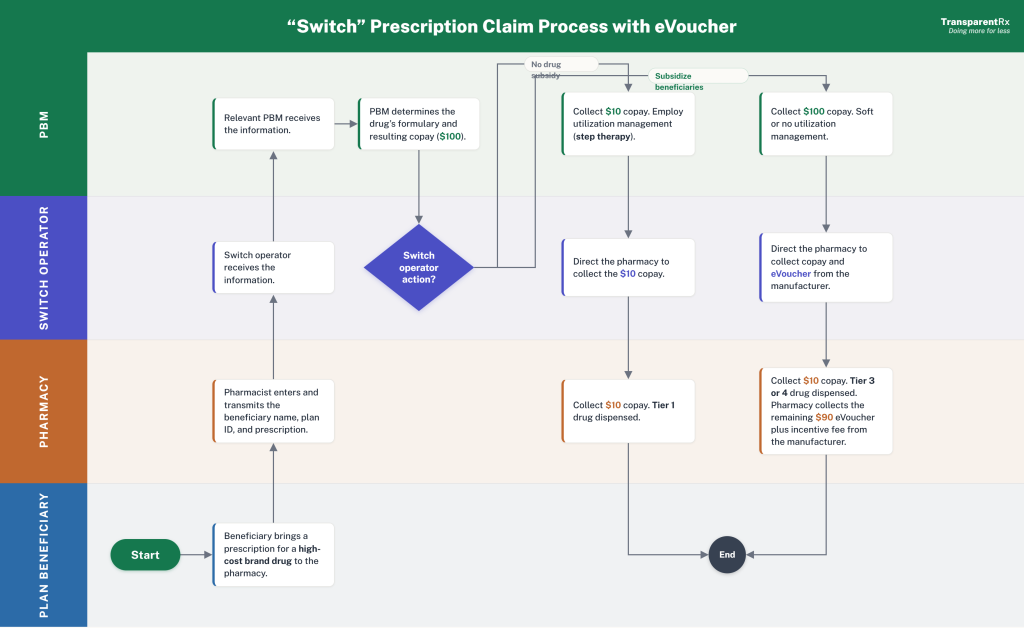

The attached e-voucher workflow illustrates why this matters. Pharmacy claims can pass through multiple entities before the final patient cost and plan paid amount are determined. When manufacturer assistance is introduced into that process, especially through electronic routing, the employer needs claim level visibility to understand the financial effect. Without it, the plan sponsor cannot tell whether the e-voucher helped the plan, helped the member, helped the manufacturer, or simply moved money around in a way that made the benefit harder to manage.

This becomes even more complicated when e-vouchers interact with copay accumulator or maximizer programs. In some arrangements, manufacturer assistance lowers the member’s cost at the pharmacy but does not count toward the deductible or out-of-pocket maximum. The patient may feel protected early in the year, then face a much larger bill once the assistance is exhausted. In other arrangements, maximizer programs are designed to capture more manufacturer assistance for certain specialty drugs. These programs can reduce plan cost in specific cases, but only if the employer understands the fees, member impact, vendor incentives, and claim-level financial flow.

The Fiduciary Standard for e-Vouchers

A self-funded employer does not need to oppose every form of manufacturer assistance. That would be too simplistic. Some members rely on assistance to afford necessary medications, especially when plan designs create high out-of-pocket exposure. The better position is not to ban e-vouchers blindly, but to demand full disclosure and measure whether the arrangement serves the plan and its members.

The fiduciary test should be straightforward. If manufacturer dollars touch the pharmacy benefit, the employer should know. If an e-voucher changes the member’s copay, the employer should know. If a rejected claim is converted into a paid claim through a manufacturer funded pathway, the employer should know. If any vendor earns revenue from the transaction, the employer should know. Hidden money has no place in a fiduciary model.

Self-funded employers should ask direct questions:

- Self-funded employers should ask direct questions:

- Which claims used e-vouchers or electronic manufacturer assistance?

- Which drugs and manufacturers were involved?

- Did the e-voucher support a preferred or nonpreferred drug?

- Did the assistance count toward the member’s deductible or out-of-pocket maximum?

- Were any rejected claims converted into paid claims?

- What fees were paid to the PBM, switch, coupon processor, pharmacy, or accumulator vendor?

- Can the plan audit this data at the claim level?

These questions are not anti-member. They are responsible benefit governance. Employers should require reporting that identifies e-voucher use at the claim level. Without this detail, the employer cannot judge whether the voucher improved affordability or weakened the plan’s cost management strategy.

Consultants and brokers should also be careful when comparing pharmacy benefit arrangements based only on member disruption. A plan that allows hidden e-vouchers may appear more member friendly in the short run, especially for people using high cost brand drugs. But if the plan is paying more to preserve those drugs, the employer deserves to know. Lower friction at the counter can come with a higher invoice behind the scenes.

The Bottom Line for Plan Sponsors

E-vouchers are attractive because they solve the problem members feel most directly: the cost they see at the pharmacy counter. But employers fund the benefit and their problem is broader. They must manage total drug spend, clinical appropriateness, vendor incentives, compliance risk, member affordability, and fiduciary oversight. Any program that improves one part of the experience while hiding the rest deserves scrutiny.

The most dangerous pharmacy benefit tools are not always the ones that look expensive. Sometimes, they are the ones that look helpful. E-vouchers can make a high-cost drug feel affordable while allowing the underlying price problem to remain untouched. They can make members believe one plan is better than another based on copay alone. They can also make it harder for employers to implement a disciplined, lowest net cost pharmacy strategy.

Employers should not confuse a lower copay with a better deal. They should not assume manufacturer assistance is free money. And they should not allow any third party to influence plan design without full transparency.

A pharmacy benefit built under a fiduciary standard of care requires visibility into every dollar, every incentive, and every transaction pathway. E-vouchers may have a place, but only when the plan sponsor can see what they are doing. When the member sees the discount and the employer pays the higher bill, the benefit is not being managed transparently. It is being managed around the employer.