When a plan sponsor decides to move medical benefit drugs to the pharmacy benefit as part of its total cost of care strategy, it shifts the focus from idea to execution. This is where benefit brokers and benefit directors can either create a smooth transition or inherit avoidable disruption. The move is not just a benefit design change. It is an implementation project involving vendors, providers, internal teams, and members. Done well, it can improve control, visibility, and savings. Done poorly, it can create confusion, provider pushback, and member dissatisfaction.

A good decision still needs a good rollout.

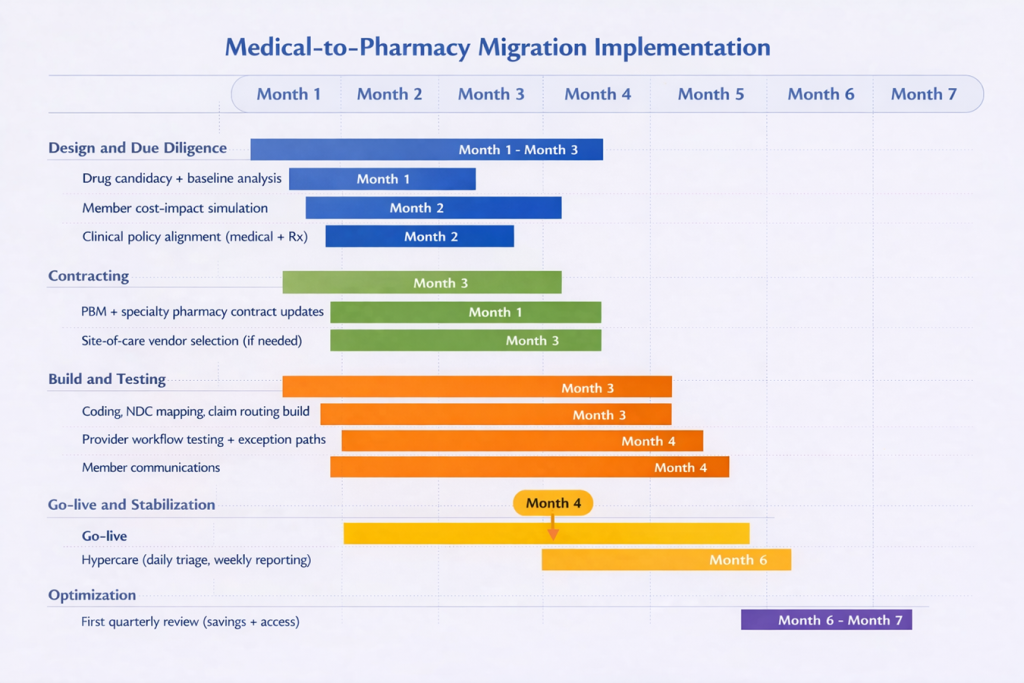

- The first step is to define exactly which drugs are moving. Not every medical benefit drug belongs on the pharmacy benefit. The best candidates are usually high-cost therapies with repeat use, clear product identification, and a real savings opportunity tied to unit cost, site of care, or utilization management. This is also the point to establish a baseline: current spend, site of care, billing patterns, denial rates, and member out-of-pocket exposure. Without that baseline, vendor savings claims are hard to verify. Payers already require detailed drug identification and accurate unit reporting on many claims, which shows how precise this work needs to be.

- The second step is vendor alignment. This is where many implementations begin to fail. The PBM may think it owns the clinical policy, the medical administrator may think prior authorization still sits on the medical side, and providers may not know who is supplying the drug. Those issues need to be resolved before any build work begins. Brokers and benefit directors need clear answers on who handles prior authorization, dispensing, drug billing, administration billing, and exceptions. That matters because medical and pharmacy coverage policies do not always align for the same drug, which can create delays, denials, and provider friction.

- The third step is to build and test the workflow before go-live. Claims routing, code mapping, prior authorization rules, specialty pharmacy logistics, exception handling, and reporting all need to be built and tested from start to finish. That means validating the full sequence: physician order, prior authorization, dispensing, provider receipt, drug administration, and claim payment. You cannot treat this as a desk exercise because provider acceptance is a real issue. Some providers and health systems will not accept white-bagged product, or they will accept it only under narrow conditions. That is why clinical groups continue to raise concerns about safety, coordination, and disruption when organizations execute these models poorly.

- The fourth step is to protect the member before the transition goes live. This is one of the most overlooked parts of implementation. Moving a drug from the medical benefit to the pharmacy benefit can change how cost share is applied. A drug once covered under medical coinsurance may now fall under a specialty tier, a different deductible, or a separate accumulator. That means the employer may save money while the member pays more, which is not a fiduciary win. One oncology study found that bagging was linked to lower insurer payments but higher patient out-of-pocket costs. Before launch, employers should model member impact, identify likely points of disruption, and prepare clear communications and escalation paths for delays, denials, or provider refusals.

- The fifth step is to treat go-live as the start of the proof period, not the finish line. For at least the first 90 days, brokers and benefit directors should monitor denial rates, prior authorization turnaround times, shipment failures, missed administrations, provider complaints, member complaints, and site-of-care shifts. That last point matters because outpatient hospital settings are often materially more expensive than physician offices for comparable services. Savings also need to be measured on a net basis. If spend simply moved from provider markup to PBM markup, the employer did not solve the problem. That is why transparent reporting and tight contract discipline matter just as much after implementation as before it. FTC scrutiny of specialty pharmacy economics is a reminder that more control does not automatically mean better value.

The strategy is set. Now comes the work.

The bottom line is simple. Once the plan sponsor makes the decision, success depends less on the strategy itself and more on how well it manages the transition. Benefit brokers and benefit directors play a central role in keeping the process disciplined, practical, and member-conscious. Employers that approach this move with a clear plan, defined accountability, and strong post-launch oversight are far more likely to achieve the savings they expect without creating unnecessary friction along the way.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.

Very informative and easy to understand.