A recent court ruling involving JPMorgan Chase should concern every self-insured employer. A federal judge allowed employees to move forward with part of a lawsuit alleging the company mismanaged its health and prescription drug benefits program, resulting in higher drug costs and premiums. On its face, the case is about one employer. In practice, it reflects a much larger shift in how courts, regulators, and plan members are viewing pharmacy benefit oversight.

For years, employers have asked a reasonable question: How can we be held responsible for fiduciary liability when PBMs refuse to share the data needed to perform that duty? It is a fair point. In many cases, the employer is expected to act as a prudent fiduciary while the PBM controls claims data, rebate terms, spread pricing, pharmacy reimbursements, network arrangements, and formulary strategy. Employers are often asked to oversee a system they cannot fully see.

But the legal environment is changing. Judges may understand the frustration, yet still expect plan fiduciaries to monitor vendors, question compensation, and avoid unreasonable arrangements. In plain terms, lack of transparency may explain the problem, but it may not excuse inaction.

That is what makes the JPMorgan case important. It suggests that if employees can plausibly claim a plan paid too much, a PBM benefited from the arrangement, and the employer failed to exercise proper oversight, the case may survive long enough to reach discovery. That alone changes the risk profile for self-insured employers. Once a case gets past an early dismissal attempt, internal documents, contracts, fee structures, and oversight practices can all come under a microscope.

This did not happen in a vacuum. The PBM industry is under pressure from multiple directions. Federal regulators have raised concerns about market concentration, vertical integration, opaque compensation, and inflated drug prices. State lawmakers continue to push new PBM reform measures. The Department of Labor is also moving toward greater fee disclosure in ERISA-covered plans. Taken together, these developments send the same message: pharmacy benefits are no longer a black box that employers can afford to ignore.

The implications reach far beyond PBMs.

- Employers will face greater pressure to prove they are actively overseeing pharmacy benefit arrangements, not merely accepting consultant recommendations or carrier reporting.

- Brokers, consultants, and other advisors will be expected to deliver more than benchmarking reports and renewal talking points. Clients need contract analysis, claims-level insight, and real oversight.

- TPAs and carriers will face increasing demands for better integration, cleaner reporting, and clearer lines of accountability across the full health plan.

- PBMs will face more pressure to explain how they are paid, what revenue exists outside the stated administrative fee, and whether plan sponsors are truly receiving the value they were promised.

- Employees and plan members may become more willing to challenge benefit practices when they believe plan costs were inflated or fiduciary duties were ignored.

- Drug manufacturers may also face more attention as policymakers and employers look more closely at list prices, rebate structures, and other distortions that affect net cost.

Self-insured employers should not read this case as a reason to panic. They should read it as a reason to stop delaying action.

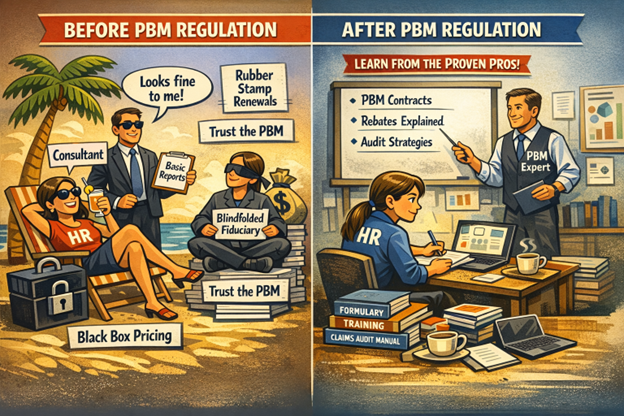

Regulation will help, but it will not solve the employer’s problem by itself. Rules can create disclosure requirements. They cannot create judgment. They cannot teach a finance leader, HR executive, or benefits committee how to spot a bad PBM contract, a weak guarantee, or a rebate arrangement that looks attractive on paper but drives up total cost. More disclosure is useful only if the employer knows what to look for and what to challenge.

That is why education matters now more than ever. But employers need to be careful about where they get it. Everyone is a thought leader now, especially with AI making it easier to sound informed. Sounding informed is not the same as knowing how PBM contracts work in the real world. It is not the same as understanding where margin hides, how specialty costs are manipulated, why guarantees often miss the point, or how to restructure a pharmacy program without shifting risk back onto members.

Self-insured employers do not need more polished commentary. They need practical guidance from people who have actually done the work. They need thought doers, not thought leaders. They need advisors who have negotiated PBM contracts, audited claims, challenged rebate narratives, rebuilt formularies, and dealt with the operational fallout when the numbers did not match the sales pitch.

This is no longer a passive compliance issue. It is a fiduciary standard of care issue.

Employers should be asking direct questions right now. Who owns the data? Can we access claims-level detail? How is the PBM paid, both directly and indirectly? What compensation exists outside the stated admin fee? Are rebates reducing net plan cost, or are they masking bad unit prices? Do we have meaningful audit rights? Can we exit the arrangement without disruption or leverage being used against us?

If those questions make a vendor uncomfortable, that is revealing. The old defense has been that employers cannot fulfill their fiduciary duty without the data. There is truth in that. But the better response now is not resignation. It is action. Demand transparency. Tighten contract language. Document oversight. Reassess the role of every intermediary involved in the pharmacy benefit. Most important, get educated by people who understand both the theory and the execution.

The JPMorgan case does not prove every employer has failed. It does show that the standard is changing. When pharmacy benefit decisions are challenged in court, the issue will not be whether the system is opaque. Everyone already knows that. The issue will be whether the employer acted like a fiduciary anyway. For self-insured employers, the message is clear: you are now on the clock.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.