When employers think about how to assess PBM service fees, most still look at the wrong number. They focus on the administrative fee instead of total compensation. That approach has allowed PBMs to quote a low visible fee while collecting far more through hidden revenue streams. A better way to evaluate PBM compensation is Earnings After Cash Disbursements, or EACD. As I explained in my earlier post on PBM math, EACD reflects what the PBM keeps after paying pharmacies and disbursing other required cash flows.

In plain English, it shows what the PBM actually earns to manage your drug benefit. That matters because PBMs have historically hidden compensation in places most employers never thought to examine. A contract might show a modest admin fee, while the PBM quietly earned more through spread pricing, specialty markups, retained rebates, network differentials, data fees, and affiliate arrangements.

That is why an artificially low admin fee should raise concern, not confidence. In many cases, the low fee was never a sign of efficiency. It was a signal that the PBM expected to make up the difference somewhere else. Said differently, the admin fee was the decoy. The real money was buried in the mechanics of the program. That model gave PBMs a blank check.

Now the market is changing. Greater scrutiny and new disclosure requirements are making it harder for PBMs to hide how they get paid. That is good news for plan sponsors, but it also means employers need to reset their expectations. If a PBM built its business on self-dealing and off-contract revenue, a truly transparent arrangement will not come with a bargain-basement fee. Plan sponsors should expect all-in administrative fees in the range of $30 to $50 PMPM from PBMs that historically profited from hidden compensation. That number may sound high to buyers accustomed to teaser pricing, but it is often more honest and easier to evaluate.

The real question is not whether the fee looks low. The real question is whether the fee reflects the PBM’s full compensation.

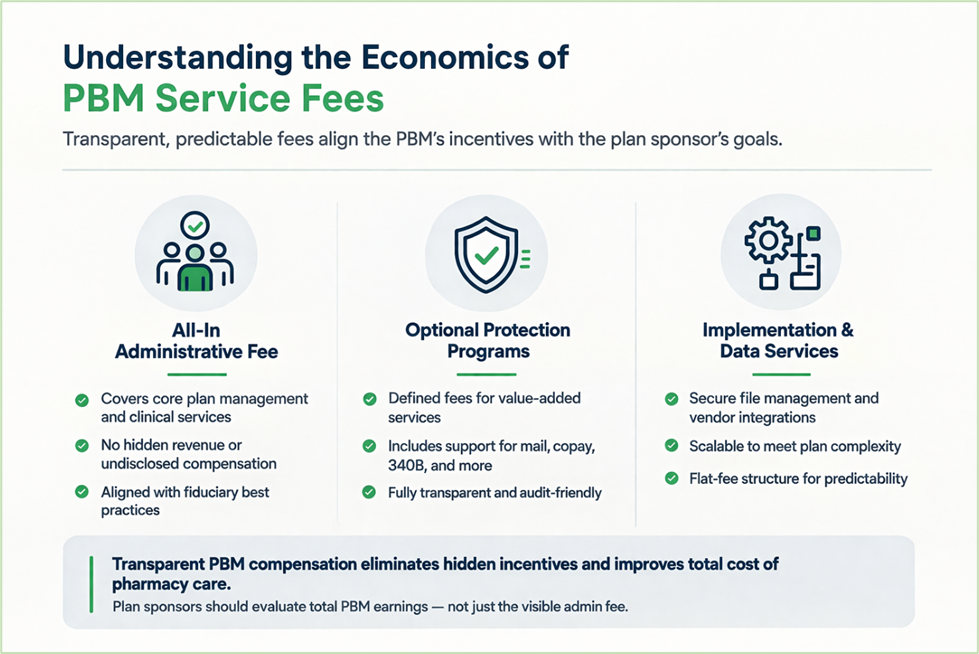

That is where understanding how to assess PBM service fees becomes practical, not theoretical. A transparent pricing model should show plan sponsors exactly what they are paying for. A cleaner structure might include a base administrative fee, a defined fee for optional protection services, and a separate charge for additional file integrations or other clearly scoped work.

Consider two PBM proposals for the same self-funded employer. One PBM offers a $4 PMPM administrative fee. Another offers a much higher all-in $16 PMPM service fee with clearly defined services and no hidden revenue rights. Many employers would instinctively lean toward the $4 offer. That would be a mistake. If the low-fee PBM owns pharmacies, controls specialty distribution, retains undisclosed income, or profits from dispensing spreads, the plan sponsor will likely pay more in the end. Fully transparent PBM service fees often look higher than legacy teaser rates because disclosed compensation is replacing revenue that was once hidden in the contract.

So what should plan sponsors do?

Start by demanding full compensation disclosure in writing. Do not settle for a narrow definition of admin fees. Require the PBM to disclose every direct and indirect source of revenue tied to your plan, including spread income, retained rebates, manufacturer payments, pharmacy fees, specialty margins, data income, and affiliate profits.

- Move away from shared savings arrangements. They often reward the PBM, or other vendors, for gaming the baseline, then charging you a percentage of the problem it helped create. A fiduciary-minded buyer should prefer fixed, transparent compensation.

- Build an internal PBM oversight team. Do not leave pharmacy benefits buried inside a general health plan workflow. Assign clear roles across benefits, finance, procurement, legal, and clinical support so someone is accountable for contracts, data review, utilization management, and vendor oversight. You do not need a new department, but you do need a focused team that treats pharmacy like a major financial asset rather than an HR side task.

- Scrutinize pharmacy reimbursement terms, especially dispensing fees. Benchmark them against NADAC-plus models where appropriate and make sure the contract clearly defines what the “plus” includes. Ambiguity is where abuse starts.

- Get educated before you go to market. If your team does not understand EACD, spread pricing, specialty pharmacy economics, or vertical integration risk, you are negotiating from a position of weakness.

Stay away from PBMs that own pharmacies whenever possible. Ownership creates conflicts that are difficult to police and even harder to unwind after the contract is signed. Most of all, stop buying PBM contracts based on what looks cheap. Buy based on what is clear, auditable, and aligned with your interests. Low fees do not save employers money. Clean economics do.

When Transparent Fees Lose to Teaser Pricing

I have sat in more RFP meetings than I can count where the reaction was immediate. I would walk through a fully transparent model, explain exactly how we get paid, and then show the management fee. You could see it on their faces. Some leaned back. Others stopped taking notes. A few exchanged looks. The number felt too high compared to the other bids on the table.

Then the conversation would shift to the competitor quoting a fraction of the fee. On paper, it looked like an easy decision. Lower admin cost, similar guarantees, same language. What was not visible in that moment was how that low fee would be recovered elsewhere through spread, pharmacy economics, or other undisclosed revenue. In many of those cases, the lower bid won.

That pattern tells you everything you need to know. PBM services are not inexpensive when structured honestly. You either see the cost upfront, or you find it later buried in the claims. The objective is transparency and value, so buyers can evaluate total compensation and make a decision they can defend long after the contract is signed.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.