The old PBM sales pitch is no longer enough. In today’s environment, cost management must be measurable, defensible, and open to inspection. With drug spend still climbing and scrutiny intensifying, plan sponsors cannot afford vague promises or half-measures. A PBM that claims to act in the client’s best interest should be able to prove it in plain view. Here are seven ways to tell whether your PBM is truly operating at maximum cost-effectiveness.

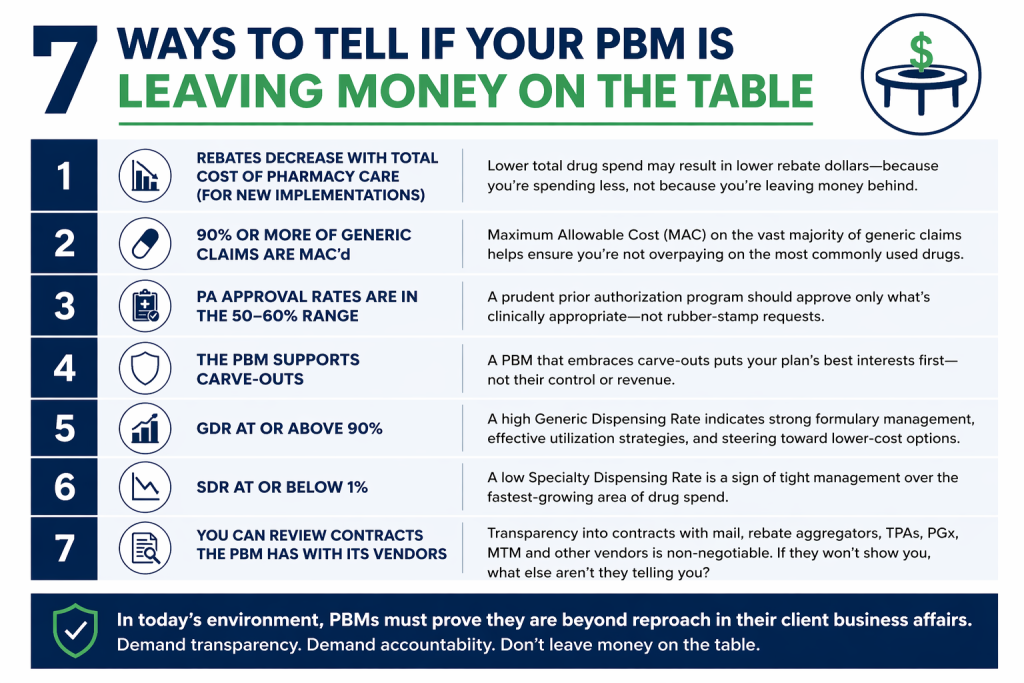

- Rebates decrease when total cost of pharmacy care (TCoPC) decreases for new implementations.

If a new PBM implementation lowers net drug spend, rebate yields may also decline because fewer high-cost brand claims are being dispensed. That is not a red flag. It is often evidence that the PBM is steering the plan toward lower cost alternatives. Brokers and Benefits Directors should focus on total cost of care, not rebate totals in isolation. A bigger rebate check means little if overall spend remains inflated. - At least 90% of generic claims are MAC’d.

A PBM serious about controlling cost should place the overwhelming majority of generic claims under a Maximum Allowable Cost methodology. When too many generic claims fall outside MAC, the plan is exposed to unnecessary spread and inflated reimbursement. This metric gives consultants and fiduciaries a quick way to test whether the PBM is applying disciplined pricing controls where they matter most. - Prior authorization approval rates fall in the 50% to 60% range.

A PA program that approves nearly everything is not managing utilization. It is rubber-stamping it. A rate in the 50% to 60% range suggests the PBM is conducting real clinical review and stopping inappropriate or avoidable spend. For Benefits Directors, that means the utilization management program is doing its job instead of serving as window dressing. - The PBM supports carve-outs.

When a PBM resists carve-outs, the objections usually sound familiar: safety concerns, compliance risk, operational complexity, or disruption. Plan sponsors have heard it all. In many cases, that resistance is about preserving control and protecting revenue streams. A cost-effective PBM should be willing to support carve-outs when they create better economics or oversight for the client. - Generic dispensing rate is 90% or higher.

A high GDR remains one of the clearest signs that the plan is being steered toward lower-cost therapies when clinically appropriate. It does not tell the whole story, but it is still a strong indicator of formulary discipline, prescriber engagement, and member channel management. For brokers, it is a simple metric that signals whether savings strategies are translating into actual behavior. - Specialty dispensing rate is 1% or lower.

Specialty utilization drives an outsized share of pharmacy spend. A lower SDR can indicate tighter management, better site-of-care strategies, stronger prior authorization controls, and more effective biosimilar adoption. Benefits leaders should watch this closely because even small changes in specialty mix can materially affect total plan cost. - You can review the PBM’s vendor contracts.

If the PBM will not let you review contracts with mail pharmacies, rebate aggregators, TPAs, PGx vendors, MTM vendors, and others, you are being asked to trust what should be verified. Transparency at this level is no longer optional. Given the current climate, PBMs must be beyond reproach in their client business affairs. Anything less should concern every fiduciary.

A PBM that truly maximizes cost-effectiveness does not hide behind talking points. It shows its work.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.