Pharmacy benefit managers (PBMs) play a critical role in managing prescription drug costs for employers, yet many benefit decision-makers struggle with how to compare PBM proposals. The lack of clarity often results in higher costs, misaligned incentives, and poor contract terms. If you’re a PBM consultant, director of benefits, or benefit broker, understanding the differences between traditional, pass-through, transparent, and fiduciary PBMs is essential to making informed recommendations. Here’s how each model operates and why the distinctions matter.

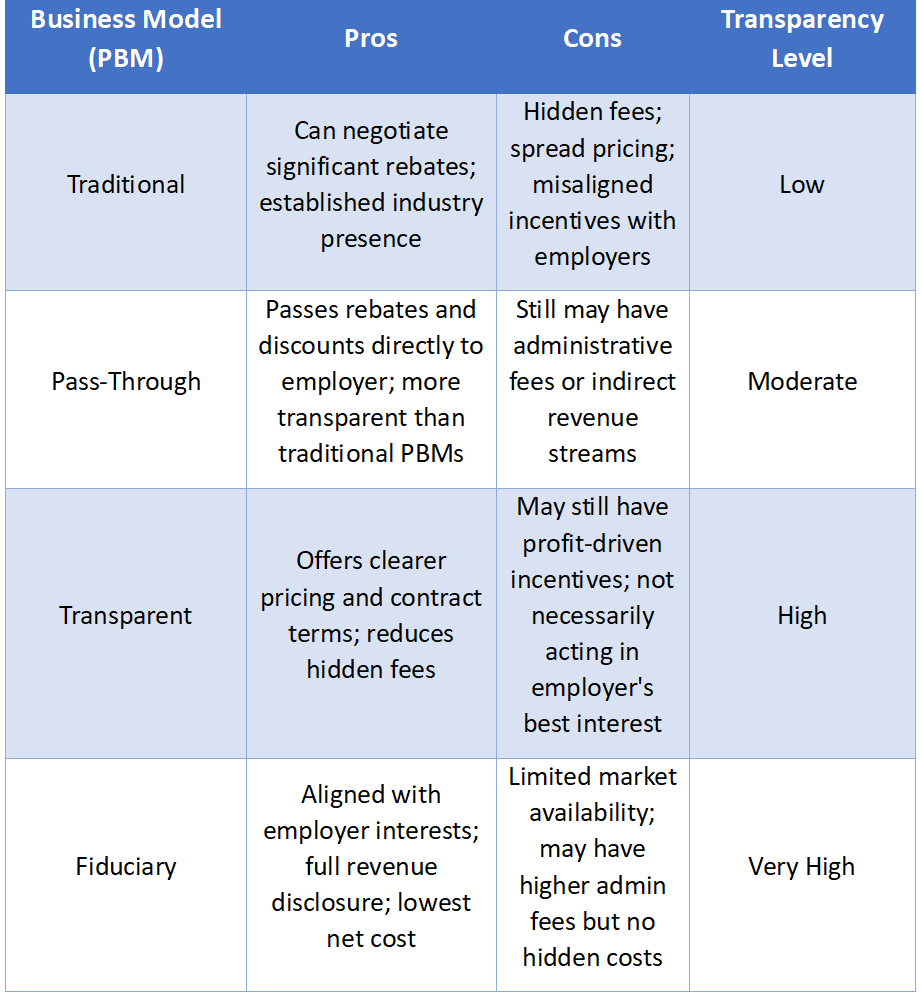

Traditional PBMs: Profits Over Transparency

Traditional PBMs operate under a spread pricing model, where they charge plan sponsors more for drugs than they reimburse pharmacies. They also retain a portion of manufacturer rebates instead of passing the full amount back to the employer. While they claim to reduce pharmacy costs, the reality is that their financial incentives are misaligned with the employer’s goal of cost containment. The lack of visibility into contract terms allows traditional PBMs to generate excessive margins at the expense of plan sponsors.

Pass-Through PBMs: A Step Forward, But Not Enough

Pass-through PBMs promote transparency by committing to pass all rebates, discounts, and pharmacy reimbursements directly to the employer. However, this model does not necessarily eliminate hidden fees. Some pass-through PBMs still engage in practices such as administrative fees or spread pricing under different labels, making it crucial to scrutinize contract language carefully.

Transparent PBMs: More Clarity, But Still Not Fully Aligned

Transparent PBMs provide greater visibility into pricing and contractual terms, offering more straightforward fee structures. However, transparency alone does not guarantee fiduciary alignment. Some transparent PBMs still derive profits from administrative fees or other undisclosed revenue streams. While they disclose costs more openly than traditional or pass-through models, employers must still verify that the PBM’s financial incentives align with their best interests.

Fiduciary PBMs: The Gold Standard

A fiduciary PBM is contractually obligated to act in the best interests of the plan sponsor and its members. Unlike traditional, pass-through, or transparent PBMs, fiduciary PBMs fully disclose all revenue sources, eliminate spread pricing, and pass 100% of rebates back to the employer. They charge a flat administrative fee for their services, ensuring their profit does not depend on inflated drug costs or hidden fees. This model creates true alignment between the PBM and the employer, leading to lower overall costs and better outcomes.

Why Employers Struggle to Differentiate PBM Proposals

- Misleading Terminology: PBMs often use terms like “pass-through” and “transparent” to appear cost-effective, but their contracts may still include hidden fees.

- Complex Contracts: PBM agreements are notoriously difficult to decipher, filled with clauses that allow for profit retention through indirect means.

- Focus on Rebates Instead of Net Costs: Many decision-makers fixate on rebate amounts rather than overall drug spending, failing to see how lower ingredient costs can save more money than high rebates.

- Inconsistent Pricing Structures: Without standard pricing models, comparing PBM proposals side-by-side is challenging.

How to Cut Through the Confusion

- Demand a Fiduciary Standard: If a PBM refuses to sign a fiduciary contract, it’s a red flag.

- Focus on Net Cost, Not Rebates: A high rebate percentage or dollar amount does not mean lower drug costs.

- Request Full Revenue Disclosure: Ask the PBM to disclose all sources of income and ensure there are no hidden fees.

- Continuous Monitoring: Provides real-time oversight, allowing plan sponsors to detect and address pricing discrepancies, contract non-compliance, and waste before they escalate into major financial losses.

Final Thoughts

The contract is the foundation of any PBM relationship, dictating pricing, transparency, and accountability. Without a carefully negotiated agreement, employers may unknowingly agree to terms that allow hidden fees and misaligned incentives to persist. To achieve radical transparency and cost control, every PBM contract should be reviewed by an expert who understands the complexities of pricing structures, revenue streams, and contract loopholes. A thorough review ensures that the PBM is fully aligned with the employer’s best interests, eliminating hidden costs, and creating a pathway for sustainable savings. Investing in expert oversight of PBM contracts is not just a best practice—it’s a necessity for securing the financial health of your pharmacy benefits plan.

Agree, full fiduciary PBM insurance busibess model is only way to go. Big 3 have shown time and time again work arounds to piecemeal 100 % pass thru

See my new 8 page outline of full PBM insurance business model on my website