Channel management is one of the most overlooked levers in pharmacy benefit design. Too many plans fixate on unit cost or rebates while ignoring where drugs are dispensed and who controls the economics. Channels are not neutral. Each one carries its own incentives, risks, and transparency gaps. When employers fail to manage channels deliberately, PBMs manage them instead.

Retail Pharmacy. Retail pharmacies remain the front door for most members. They offer convenience and access, but they also hide significant pricing variation. Employers should manage retail through narrow or preferred networks tied to transparent reimbursement benchmarks, not inflated AWP formulas. PBMs should pay pharmacies using fully disclosed ingredient costs and fixed dispensing fees. Employers must eliminate spread pricing and require claim-level audit rights. Retail becomes cost-effective only when the plan sponsor controls network design and pricing rules.

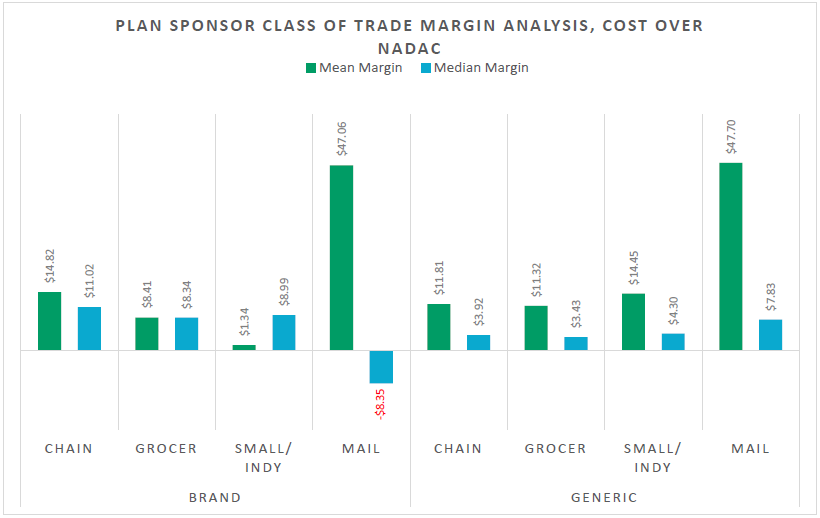

Mail Order. PBMs often position mail order as a savings tool, but they frequently use it as a profit center. The channel itself is not the issue. Oversight is. Employers should treat mail order as an option, not a mandate, and apply the same transparent pricing logic used in retail. Plan sponsors should require disclosure of acquisition cost, prohibit auto-refill without member consent, and tie guarantees to adherence and waste reduction. Mail order works only when it serves members instead of maximizing PBM margin.

Specialty Pharmacy. Specialty drives the fastest growth in pharmacy spend and attracts the most aggressive channel manipulation. PBMs steer volume to affiliated specialty pharmacies, restrict distribution, and rebrand identical drugs to protect margins. Employers should manage specialty as a clinical channel first. They should demand open pricing, visibility into manufacturer assistance, and full disclosure of ownership relationships. Site-of-care optimization, dose management, and outcomes reporting matter more than rebate yields. True transparency means knowing the net cost per drug therapy.

340B. The 340B channel introduces complexity and frequent conflicts of interest. While it can reduce costs in certain scenarios, it often shifts margin to covered entities and contract pharmacies instead of employers. Plan sponsors should not assume savings. They should require claim-level identification, clear contracts, and defined savings allocation. When employers pay commercial prices while others retain the spread, the program creates leakage, not value.

International Sourcing. International sourcing now plays a legitimate role for select maintenance medications. When executed correctly, it delivers meaningful savings. Employers should govern this channel tightly, limit it to FDA-compliant pathways, and communicate clearly with members. International sourcing should complement domestic options, not replace them. Employers must understand which drugs qualify and where savings actually flow.

Other Channels Worth Attention. Direct-to-employer and cost-plus pharmacy models reduce intermediaries and improve price visibility, especially for generics. They do not solve every problem, but they belong in a fiduciary strategy. White bagging and brown bagging also demand attention. Employers should treat them as intentional channel decisions tied to site-of-care strategy, not operational afterthoughts.

The takeaway is simple. Channel management requires fiduciary discipline. Employers must align incentives, eliminate hidden margins, and maintain clear line-of-sight into every pharmacy dollar. Transparency is not a feature added later. It is the standard from day one.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

When a PBM change is on the table, the RFP process should surface more than just headline pricing. We participate in RFPs to provide full transparency into costs, guarantees, and alignment so plan sponsors can make informed, defensible decisions.

Choose your option to get clear, fiduciary guidance your team can rely on for pharmacy benefits decisions this week.

This is my first time pay a quick visit at here and i am really happy to read everthing at one place

Awesome! Its genuinely remarkable post, I have got much clear idea regarding from this post

I like the efforts you have put in this, regards for all the great content.