Self-funded employers often face a difficult tradeoff in pharmacy benefit management. They can reduce unnecessary pharmacy spend or limit member disruption. On the surface, avoiding disruption feels like the safer path. HR teams do not want employees frustrated at the pharmacy counter, calling about medication changes, or asking why a drug that worked yesterday now requires a different process today.

That concern is real. But it can also become expensive. In many pharmacy plans, meaningful savings are available through better formulary management, stronger utilization management, and a more disciplined approach to generic and therapeutic alternatives. The challenge is that those savings often require some level of change for a small portion of members.

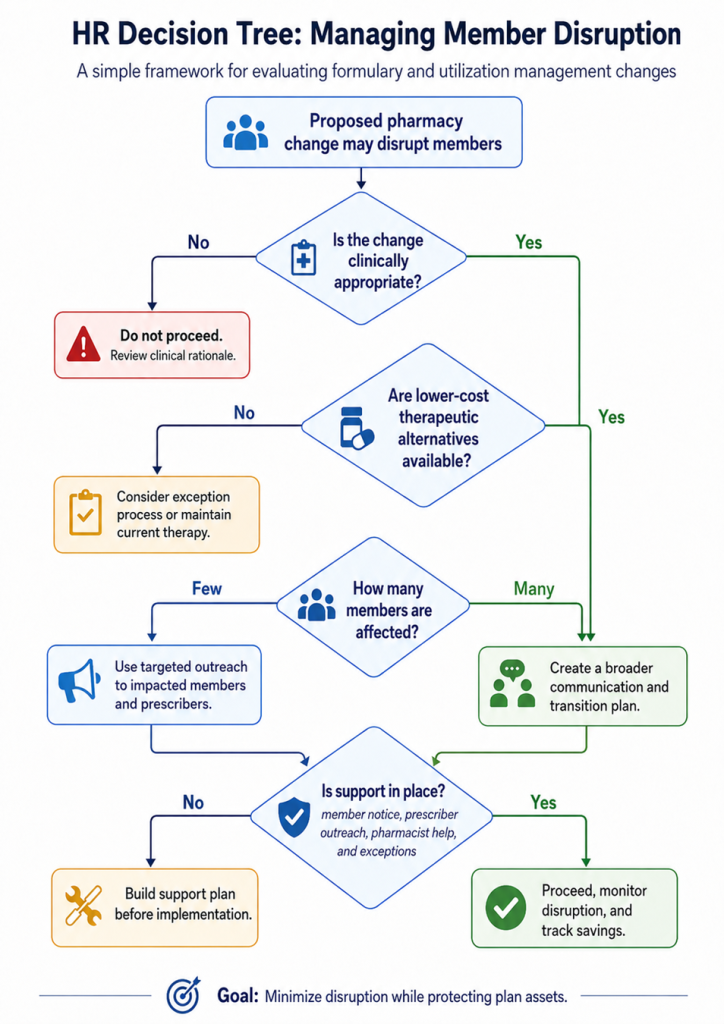

The Concern: Member Disruption

When a plan moves from a loose formulary to a more carefully managed one, some members may be affected. A member may need to switch from a brand drug to a generic equivalent. Another may need to move to a lower cost therapeutic alternative. Others may go through prior authorization, step therapy, or an exception review.

That creates anxiety for HR, and understandably so. HR teams often hear the complaints, even when the clinical and financial rationale is sound. No one wants a benefit change to feel like a takeaway, especially when employees are dealing with medications they rely on. But the question should not be, “Will there be any disruption?” A better question is, “Is the disruption clinically appropriate, financially justified, and properly supported?”

Reckless vs. Responsible Disruption

There is a big difference between reckless disruption and responsible disruption. Reckless disruption happens when members are forced through confusing changes without support, communication, or clinical review. That creates frustration and can harm trust. Responsible disruption looks different. It includes:

- Advance member notice before changes take effect

- Prescriber outreach when therapy changes may be needed

- Clear therapeutic alternatives when clinically appropriate

- Exception protocols for members with legitimate clinical needs

- Pharmacist support for members who need help navigating the change

That is not disruption for the sake of savings. That is fiduciary plan management.

The Fiduciary Issue

Self-funded employers have a duty to manage plan assets carefully. Every unnecessary dollar spent on an avoidable high-cost medication is a dollar that cannot be used for wages, benefits, reserves, or other priorities. When lower-cost alternatives are clinically appropriate, ignoring them is not member advocacy. It is poor stewardship.

Take a simple generic dispensing rate example. Assume a self-funded plan spends $10 million annually on pharmacy claims and has an 80% generic dispensing rate. If stronger formulary management, utilization management, and member support can move that plan to a 90% generic dispensing rate, the plan gains ten percentage points of improvement.

If each one point increase in generic dispensing rate produces an estimated 4% gross savings, the math is hard to ignore. A ten point improvement would represent an estimated 40% gross savings opportunity. On a $10 million annual pharmacy spend, that equals approximately $4 million in potential gross savings.

That does not mean every plan will capture the full amount. Savings depend on the drug mix, brand utilization, specialty exposure, rebates, member behavior, prescriber cooperation, and how well the transition is managed. But the example makes the fiduciary point clear. Even modest improvements in generic dispensing can create major financial consequences for a self-funded employer.

A low generic dispensing rate, high non-formulary spend, or excessive use of non-preferred brands can signal that the plan is paying more than necessary. These patterns do not always mean care is better. Often, they mean the formulary is not being managed tightly enough, the incumbent PBM has not applied sufficient controls, or the plan sponsor has not been given a clear picture of the tradeoffs.

The Cost of Doing Nothing

HR teams often feel caught between two pressures: controlling pharmacy costs and avoiding employee complaints. That tension is real. But avoiding every difficult conversation is not a strategy. It usually means the plan is allowing historical prescribing patterns, manufacturer influence, or PBM economics to drive decisions.

Before implementing any major formulary or utilization management change, the affected member population should be reviewed carefully. Some members may have direct generic equivalents available. Others may have lower-cost therapeutic alternatives. Some cases may require clinical review. A smaller group may need more hands-on support to avoid confusion or gaps in therapy.

This is where many employers make the wrong comparison. They compare the discomfort of change against the comfort of doing nothing. But doing nothing has a cost, and in pharmacy benefits, that cost can be substantial.

The Better Standard

The purpose of a well-managed pharmacy benefit is not to keep everything exactly as it is. It is to protect members while protecting the plan. Sometimes that means change. Sometimes it means telling a member, “There is a clinically appropriate alternative, and the plan will support you through the transition.”

That message is not anti-member. It is honest. Most employees do not know whether their medication is preferred, non-preferred, non-formulary, or clinically replaceable. They only know what their doctor prescribed and what they pay at the pharmacy counter. It is the plan’s responsibility, with the right pharmacy benefit administrator, to create a structure that helps members get appropriate care without wasting plan dollars.

Disruption should be minimized, not worshipped. The better goal is not zero disruption. The better goal is the right disruption, for the right reasons, with the right support. For self-funded employers, that distinction can be worth millions.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.