Mark Cuban recently posed a simple but important question: if pharmacy benefit managers can no longer generate revenue as a percentage of drug list prices, where will the money come from?

The answer is straightforward. It will come from somewhere else. Revenue in the PBM industry rarely disappears. It shifts. As regulatory pressure increases on spread pricing and rebate-driven compensation, vertically integrated PBMs are repositioning how they generate margin. The industry is transitioning away from price-linked income and toward fee-based services and control of dispensing channels.

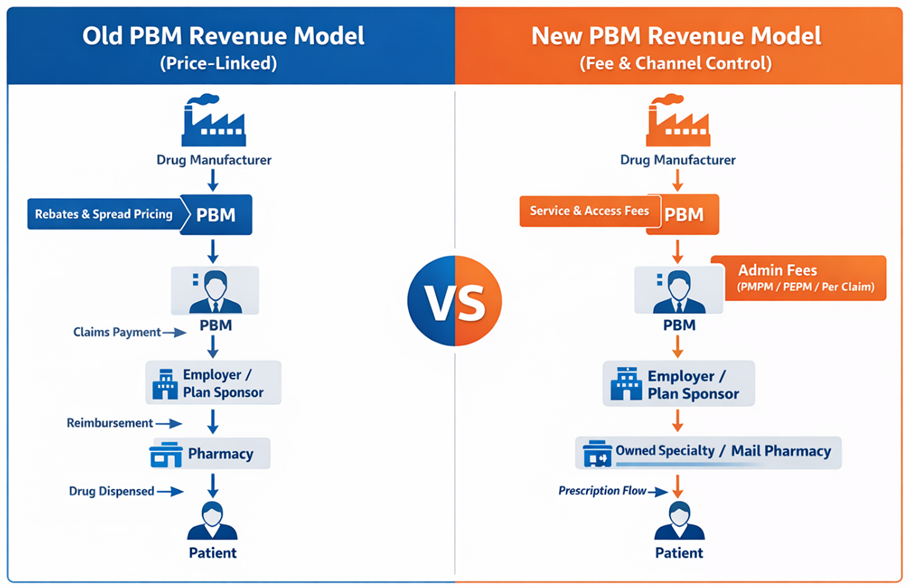

The Shift from Drug Price Revenue to Service Fees

For years, PBM profits were closely tied to the price of drugs. Rebates and spreads provided a steady stream of revenue that was largely invisible to employers. That model is now under scrutiny from regulators and plan sponsors. In response, PBMs are replacing percentage-based compensation with administrative service fees that are billed directly to employers.

Charging administrative fees is not inherently problematic. Employers should expect to pay PBMs for legitimate services such as claims processing, clinical oversight, network management, and reporting. The concern lies in how these fees are structured and whether they accurately reflect the value being delivered.

PBMs typically bill administrative services in one of three ways: per paid claim, per employee per month (PEPM), or per member per month (PMPM). While each structure can produce similar economics if priced properly, the incentive structure behind the fee matters greatly. Employers should carefully examine how these fees align with the PBM’s financial interests.

One structure employers should avoid entirely is percentage-of-savings compensation. This arrangement often appears in carve-out programs, particularly those targeting specialty drugs or cost-containment initiatives. The PBM promises to reduce costs and retain a percentage of the “savings.” However, the PBM often controls how savings are defined and measured. If the starting price is inflated, the reported savings can appear significant even when the employer is still paying more than necessary.

Percentage-of-savings models create a troubling incentive. High claim volumes and inflated baseline prices can increase the PBM’s share of the savings calculation. Employers end up rewarding the very behavior they are trying to control.

Where Vertically Integrated PBMs Will Find New Margin

At the same time, many PBMs are introducing layered PMPM service fees. Clinical programs, utilization management initiatives, data analytics platforms, and reporting systems are increasingly being packaged as separate cost-management services. Functions that were once embedded in the PBM contract are now itemized and billed individually. Some of these programs provide real value. Others represent services PBMs were already expected to perform as part of basic plan administration.

Meanwhile, vertically integrated PBMs are shifting margin downstream into businesses they own. Specialty pharmacies, mail-order facilities, and affiliated dispensing channels have become central to their economic strategy. When the PBM controls the formulary, the pharmacy network, and the prescription routing process, it can direct prescriptions into pharmacies it owns or controls. The margin generated by dispensing then appears within the pharmacy operation rather than in the PBM contract itself.

This strategy allows vertically integrated organizations to preserve profitability even as traditional rebate structures face scrutiny. The economics shift from price control to channel control. Another emerging revenue source involves manufacturer “service fees.” These payments are often described as compensation for market access, data analytics, or clinical program support. While the terminology has changed, the underlying financial relationship between manufacturers and PBMs frequently remains intact.

All of this illustrates an important point: transparency alone is not enough. What is happening now goes beyond transparency. Plan sponsors are beginning to examine PBM economics much more closely. In other words, pocket-watching has begun. Employers are no longer satisfied with rebate guarantees or assurances of pass-through pricing. They want to understand the entire financial structure supporting their pharmacy benefit program. Administrative fees, channel margins, manufacturer payments, and program charges must all be evaluated together.

The CPBS Way: Running an RFP That Actually Works

The most effective way to achieve that visibility is through a well-run request for proposal and continuous monitoring. A disciplined RFP process forces PBMs to disclose how they generate revenue and what services they are charging for. It allows plan sponsors to compare competing models and determine which PBM offers the best overall value. In the CPBS framework, an effective PBM RFP follows a structured process designed to eliminate ambiguity and marketing theater. The “CPBS Way” relies on six steps to produce meaningful comparisons and enforce accountability.

- Require consulting firms and plan sponsors to have skilled staff with extensive PBM knowledge. Without subject-matter expertise, critical contract provisions and pricing mechanisms often go unchallenged.

- Draft an entirely new PBM contract that eliminates common loopholes. Allowing PBMs to submit proposals using their own contract templates invites hidden revenue opportunities.

- Develop a questionnaire that seeks only verifiable information. Marketing claims and projections should be excluded in favor of responses that can be validated through contract language or audit rights.

- Conduct extensive legal negotiations with remaining PBM candidates early in the process. Key contractual issues should be resolved before finalists are selected.

- Select semi-finalists based on binding contract terms and firm pricing commitments rather than marketing narratives.

- Conduct finalist presentations that function as validation sessions, not marketing contests. At this stage, the focus should be operational capability and clarification of remaining issues.

Administrative pricing can also serve as an important signal. When a PBM proposes an all-in administrative fee below ten dollars PMPM, employers should approach the offer with caution. Operating a compliant PBM platform with meaningful clinical programs, reporting infrastructure, and member support requires real investment.

If the administrative fee appears artificially low, the PBM will almost certainly recover margin somewhere else. That recovery often occurs through pharmacy channel ownership, specialty dispensing margins, or additional program fees.

There is no such thing as a free PBM. For employers, the focus should shift from individual pricing components to the total economic picture. Administrative fees, dispensing margins, specialty pharmacy economics, and program charges must all be considered together.

The real question is not whether PBMs will replace rebate income with service fees. That transition is already underway. The real question is whether employers fully understand the total fee stack they are paying and whether those fees produce measurable results for their plan and their members.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.