|

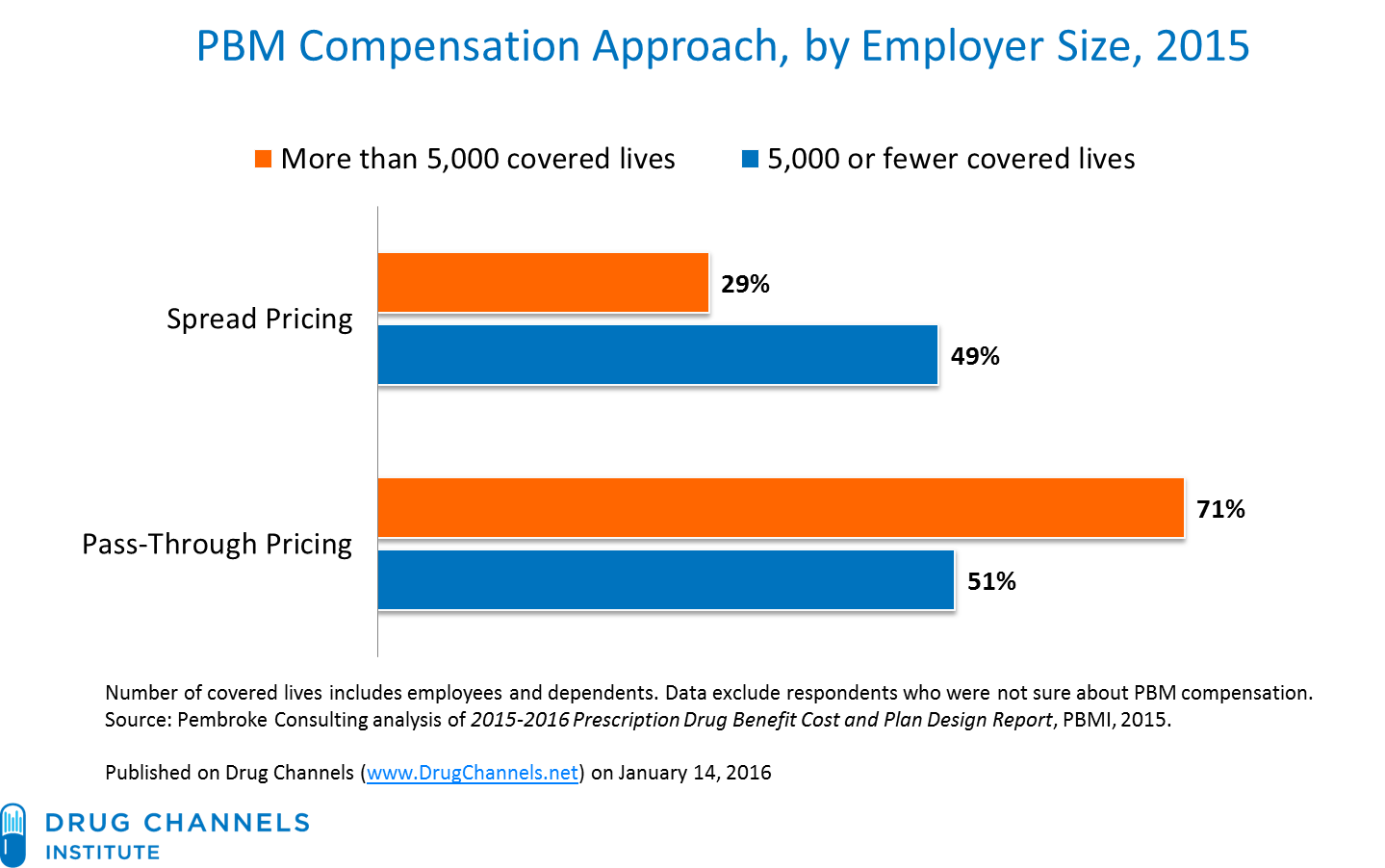

| [Click to Enlarge] |

Can payers save money on increasingly expensive prescriptions by setting prices based not on drugmakers’ wishes, but on how well the medicines control, contain or cure disease?

The notion of tying drug payments to results, called “pay-for-performance pricing” or “value-based pricing,” already is being tested by some health insurance companies, some pharmaceutical companies and Medicare. And just last week, the Oregon Health & Science University announced it will undertake a large-scale research project to examine how states could apply the concept to Medicaid.

Tyrone’s comment: If all the savings are passed-back then great! But, value-based pricing is rife with hidden cash flow opportunities for non-fiduciary pharmacy benefit managers. Traditional or non-fiduciary PBMs are aware of the attention being paid to existing pricing arrangements or overpayments (see ESI, Anthem dispute) so this new pricing arrangement could serve a dual purpose; to show an effort to control costs AND protect their margins. Put another way, pay-for-performance arrangements provide an opportunity for non-fiduciary PBMs to protect margins while giving the “appearance” of reducing drug costs. How will a payer know when a drug has failed and just as important what happens to the revenue when a manufacturer credits it, for example? Remember this, better doesn’t necessarily mean good. The concept is both brilliant and misleading so close the loopholes!

If payers are able to adopt a workable performance- or value-based pricing system on drugs, they may be able to hold down spiraling Medicaid spending, said Matt Salo, executive director of the National Association of Medicaid Directors.

Medicaid, the federal-state health insurance plan for the poor, is staggering under escalating prescription drug prices just as patients and private insurers are, and the costs are straining state budgets. On average, roughly a quarter of a state’s budget goes to Medicaid spending.

Medicaid spending on prescription drugs for Medicaid recipients rose 24.3 percent between 2013 and 2014, in part owing to an increase in enrollment under the Affordable Care Act. That was nearly double the increase in total U.S. prescription drug spending in that same period, according to federal data.

And there’s every reason to think the increase in spending will continue as drugmakers prepare to introduce dozens more “specialty drugs,” high-priced, complex medications developed from living cells to treat chronic conditions such as hepatitis C, HIV, cancer, rheumatoid arthritis and multiple sclerosis.

Although they barely existed a decade ago, last year specialty drugs accounted for nearly a third of Medicaid spending, or about $16.9 billion. Specialty drugs make up just 1.5 percent of claims, but they could play a big role in the rise of Medicaid spending on drugs.

Something has to give, said Jeff Myers, CEO of Medicaid Health Plans of America, the trade association representing Medicaid managed care plans. “A system in which the manufacturers are pricing to get the most money out of taxpayers isn’t workable,” he said.

Pay-for-Performance

Currently, Medicaid and federal health plans such as Medicare and the U.S. Department of Veterans Affairs are constrained in bargaining with manufacturers over drug prices.

Pharmaceutical companies enter into agreements with the federal Centers for Medicare and Medicaid Services on what drugs all state Medicaid programs will make available to patients. In return, the pharmaceutical companies agree to give the states fixed discounts off their average price.

But those prices are set by the manufacturers, and the manufacturers are not governed by any price ceilings, nor are the prices based on the drugs’ success, such as whether they control or cure a patient’s disease.

Pay-for-performance or value-based pricing would change that. It would tie payments for prescription drugs to their effectiveness, whether they did what they were designed to do.

How well do medications for high blood pressure or cholesterol, for example, keep patients in healthy ranges for each? How well do medications control symptoms of autoimmune diseases? How much do cancer drugs extend life? And how much do the drugs save the health care system by enabling patients to avoid medical treatments they no longer need?

How to Price

Evaluating the effectiveness of a drug will be essential to pricing under the concept. One tool health plans could use for evaluating cancer drugs to establish a price has been developed by the Center for Health Policy and Outcomes at Memorial Sloan Kettering Cancer Center, in New York.

Called the “DrugAbacus,” the tool creates a price for cancer drugs based on how many years of additional life they provide, the severity of their side effects, the rarity of the disease and the novelty of their chemistry.

<< Read More >>