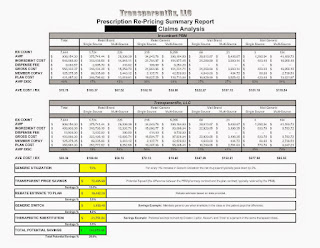

Claims Analysis: Negotiated Pricing Between Preferred and Non-Preferred Retail Pharmacies

|

| CMS Analysis: preferred vs. non-preferred pharmacy networks |

CVS Health announced Tuesday that it expects to lose 40 million retail prescriptions next year because of new retail pharmacy networks that don’t include CVS, such as those created by Walgreens’ partnerships.

This year, Deerfield-based Walgreens formed partnerships with a number of pharmacy benefit managers, which are companies that manage prescription drug benefits for insurers and employers. Those partnerships make Walgreens a preferred pharmacy for people with certain health insurance plans, meaning medications for those customers are significantly cheaper at Walgreens and other in-network pharmacies than at drugstores that aren’t part of those networks.

Tyrone’s comment: A CMS analysis has proved this theory (cheaper medications in preferred networks) to be inconsistent at best. While medications may cost patients less at the point-of-sale, it turns out they could actually be more expensive to payers in a preferred network.

In September, Express Scripts, the pharmacy benefit manager for the U.S. military’s health insurance program, announced that on Dec. 1 it would add Walgreens to the military health insurance program’s network and drop CVS. That means those with military health insurance, known as Tricare, will have to get their prescriptions at Walgreens or other in-network pharmacies starting Dec. 1 or pay significantly higher rates for them elsewhere.

In August, Walgreens announced a partnership with pharmacy benefit manager Prime Therapeutics, which is owned by 14 Blue Cross and Blue Shield plans and has 22 million members. Walgreens also partnered in March with benefit manager OptumRx, which is part of UnitedHealth Group and has 66 million members.

Walgreens has been particularly aggressive in pursuing such deals, said Vishnu Lekraj, a senior equity analyst at Morningstar in Chicago. The benefit managers restrict which drugstores can be part of their networks to get better discounts on drugs from pharmacies such as Walgreens, he said.

CVS has its own pharmacy benefit manager business, and CVS President and CEO Larry Merlo said in a news release Tuesday the he expects a “healthy increase” in operating profit growth next year in that area. He said, however, that he expects a decrease in retail operating profit growth.

Tyrone’s comment: I hope self-funded employers are paying attention to this comment because it is significant. An increase in operating profit occurs one of two ways; increase in revenues and/or cost-cutting measures. In other words, Caremark will look to grow its account base but also increase incremental revenue from existing clients.

Read more: http://www.chicagotribune.com/business/ct-walgreens-cvs-prescriptions-1109-biz-20161108-story.html