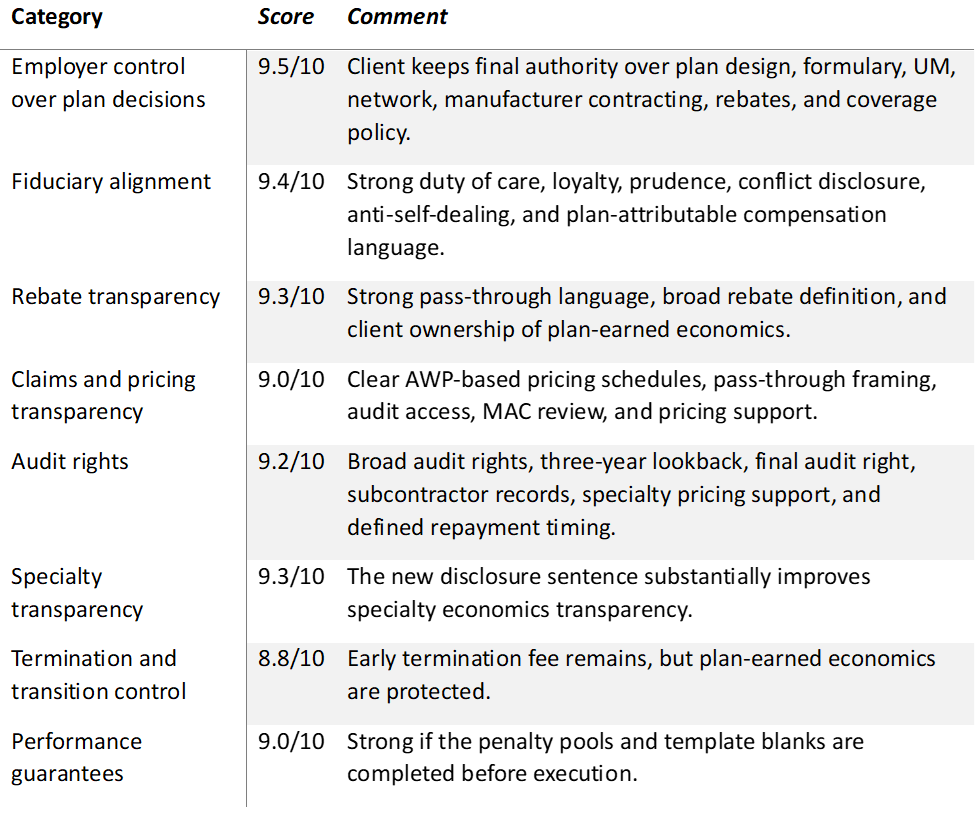

A No-Nonsense Pharmacy Benefit Model. What Does It Mean?

I read a LinkedIn post a few days where a broker said he was cold called by a PBM offering a 10% commission payable to the consultant. Around the same time, I was still seeing RFPs asking for lump monthly compensation to be paid from the PBM to the consultant.

Both examples point to the same problem. The industry has placed new expectations on PBM disclosure and transparency, but old compensation practices are still showing up in new proposals. If transparency is going to mean anything, it has to apply across the entire pharmacy benefit ecosystem, including how brokers, consultants, TPAs, and PBMs are paid.

A no-nonsense pharmacy benefit model is not complicated. It starts with a simple idea. The plan sponsor should know where the money goes, who gets paid, why they get paid, and whether those payments align with the best interests of the plan and its members.

The point should sound obvious. In pharmacy benefits, too often it does not reflect how the business works. Too many PBM arrangements still depend on money moving through side doors, including rebates, spread pricing, network differentials, data fees, consultant payments, broker payments, “clinical” programs tied to drug spend, and contract terms only a lawyer could enjoy.

A no-nonsense model strips all of it down. It puts the plan sponsor back in control, makes the economics visible, and forces every stakeholder to answer a basic question. Does this arrangement serve the plan, the members, and the fiduciary standard of care?

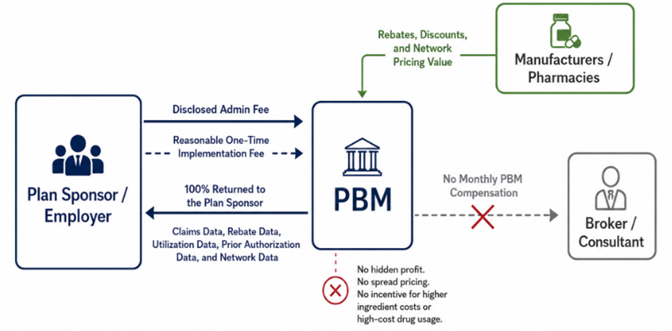

Clean PBM Economics

The PBM should not profit from the plan unless the profit is fully disclosed. Preferably, the PBM should earn its revenue through a clearly stated administrative fee. The client sees the fee, understands the fee, and can compare the fee against the work being performed.

A clean fee structure creates better alignment. When a PBM earns revenue in other ways, the incentives get messy fast. If money is tied to rebates, the PBM may benefit when high-cost drugs are used. If money is tied to ingredient cost spreads, the PBM may benefit when the plan pays more than it should. If money comes from sources the client cannot see, the client cannot determine whether the PBM is managing the benefit or monetizing it.

A fiduciary pharmacy benefits administrator should not need hidden economics to be successful. It should be paid for administration, clinical management, service, reporting, implementation, and accountability. The economics should be visible, documented, and easy for the client to verify.

No Unnecessary Cash Outflows

A no-nonsense model also means no unnecessary outflow of plan sponsor cash. Reasonable implementation fees can make sense when real work is involved. A PBM transition requires eligibility setup, benefit configuration, formulary review, clinical program buildout, accumulator coordination, member communications, testing, and go-live support.

Ongoing monthly payments to brokers or consultants from the PBM should not be part of the model. Those payments create questions the client should not have to ask. Who is the consultant working for? Is the recommendation based on the client’s best interest or on a revenue arrangement behind the scenes?

If a broker or consultant provides value, the client should pay them directly. Doing so keeps the relationship clean. It also protects the consultant’s credibility because the advice is no longer connected to an undisclosed or indirect payment stream from the vendor being recommended.

The industry needs to be honest with itself. PBMs are being asked to disclose more, pass through more, and operate with cleaner economics. Fair enough. Brokers, consultants, TPAs, and advisors also have to adjust. If transparency is the standard, compensation arrangements tied to PBM selection should not be buried in RFP terms, side agreements, or monthly payment schedules routed through the vendor.

The same standard applies to pharmacy management services and other add-on arrangements. If a service is needed, define it, price it, disclose it, and measure it. Do not bury it in the PBM’s economics and pretend it is free. Nothing in pharmacy benefits is free. Someone pays, and most of the time, it is the employer.

Client-Owned Data

A no-nonsense model also means the client owns its data. Not summaries. Not dashboards controlled by the vendor. Not reports filtered through someone else’s business interests. The client should own its claims data, rebate data, utilization data, eligibility data, prior authorization data, and pharmacy network data.

Data ownership matters because pharmacy benefit decisions cannot be managed on trust alone. Employers need the ability to verify pricing, monitor trends, evaluate clinical programs, review member disruption, test performance guarantees, and confirm whether contract terms are being followed.

If the client cannot access its own data, the client is not really in control of the plan. A vendor may say all the right things in sales meetings, but without data access, the plan sponsor has no practical way to confirm what is happening behind the scenes.

Full Audit Rights

Full audit rights are part of the same standard. A plan sponsor should have the right to audit claims, pricing, rebates, fees, guarantees, and any other financial arrangement tied to the pharmacy benefit. The audit should not be limited by narrow contract language, unnecessary delays, or vendor-controlled definitions of what can be reviewed.

A fiduciary standard of care requires more than a promise. It requires evidence. Audit rights give the plan sponsor a way to test whether the PBM’s conduct matches the contract and whether the contract matches the employer’s expectations.

In a no-nonsense model, audit rights are not treated as a threat. They are part of good governance. If the PBM is doing what it says it is doing, audit rights should not be a problem.

The Standard Employers Should Expect

In my view, a no-nonsense pharmacy benefit model comes down to a few basic principles.

- The PBM gets paid in a clear and disclosed way.

- The plan sponsor receives all rebates, discounts, and pricing value intended for the plan.

- The PBM does not earn more when drug costs go up.

- The broker or consultant is not quietly paid by the PBM.

- The client owns the data.

- The client has full audit rights.

- The contract supports the fiduciary standard of care instead of working around it.

Employers are not asking for anything radical. They are asking for pharmacy benefits to work the way vendor relationships should have worked all along. They need clean economics, clear contracts, useful data, and a PBM willing to be measured by the same standard it claims to represent.

A no-nonsense pharmacy benefit model means fewer games, fewer excuses, and fewer hidden incentives. More importantly, it means every stakeholder has to live under the same standard they are asking others to meet.