The old PBM sales pitch is no longer enough. In today’s environment, cost management must be measurable, defensible, and open to inspection. With drug spend still climbing and scrutiny intensifying, plan sponsors cannot afford vague promises or half-measures. A PBM that claims to act in the client’s best interest should be able to prove it in plain view. Here are seven ways to tell whether your PBM is truly operating at maximum cost-effectiveness.

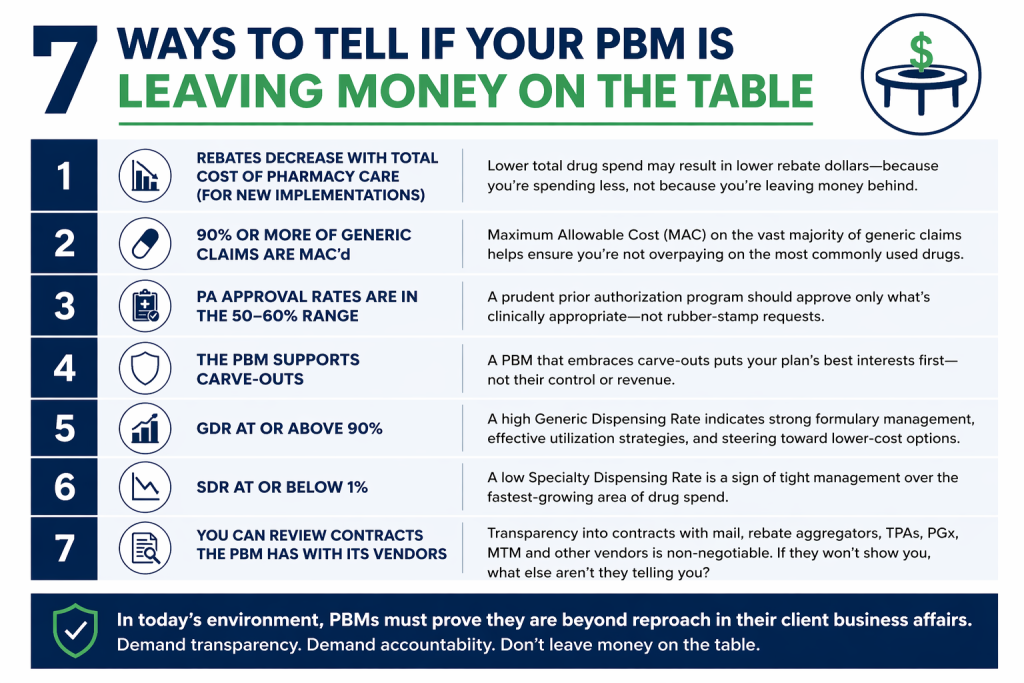

Rebates decrease when total cost of pharmacy care (TCoPC) decreases for new implementations. If a new PBM implementation lowers net drug spend, rebate yields may also decline because fewer high-cost brand claims are being dispensed. That is not a red flag. It is often evidence that the PBM is steering the plan toward lower cost alternatives. Brokers and Benefits Directors should focus on total cost of care, not rebate totals in isolation. A bigger rebate check means little if overall spend remains inflated.

At least 90% of generic claims are MAC’d. A PBM serious about controlling cost should place the overwhelming majority of generic claims under a Maximum Allowable Cost methodology. When too many generic claims fall outside MAC, the plan is exposed to unnecessary spread and inflated reimbursement. This metric gives consultants and fiduciaries a quick way to test whether the PBM is applying disciplined pricing controls where they matter most.

Prior authorization approval rates fall in the 50% to 60% range. A PA program that approves nearly everything is not managing utilization. It is rubber-stamping it. A rate in the 50% to 60% range suggests the PBM is conducting real clinical review and stopping inappropriate or avoidable spend. For Benefits Directors, that means the utilization management program is doing its job instead of serving as window dressing.

The PBM supports carve-outs. When a PBM resists carve-outs, the objections usually sound familiar: safety concerns, compliance risk, operational complexity, or disruption. Plan sponsors have heard it all. In many cases, that resistance is about preserving control and protecting revenue streams. A cost-effective PBM should be willing to support carve-outs when they create better economics or oversight for the client.

Generic dispensing rate is 90% or higher. A high GDR remains one of the clearest signs that the plan is being steered toward lower-cost therapies when clinically appropriate. It does not tell the whole story, but it is still a strong indicator of formulary discipline, prescriber engagement, and member channel management. For brokers, it is a simple metric that signals whether savings strategies are translating into actual behavior.

Specialty dispensing rate is 1% or lower. Specialty utilization drives an outsized share of pharmacy spend. A lower SDR can indicate tighter management, better site-of-care strategies, stronger prior authorization controls, and more effective biosimilar adoption. Benefits leaders should watch this closely because even small changes in specialty mix can materially affect total plan cost.

You can review the PBM’s vendor contracts. If the PBM will not let you review contracts with mail pharmacies, rebate aggregators, TPAs, PGx vendors, MTM vendors, and others, you are being asked to trust what should be verified. Transparency at this level is no longer optional. Given the current climate, PBMs must be beyond reproach in their client business affairs. Anything less should concern every fiduciary.

A PBM that truly maximizes cost-effectiveness does not hide behind talking points. It shows its work.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.

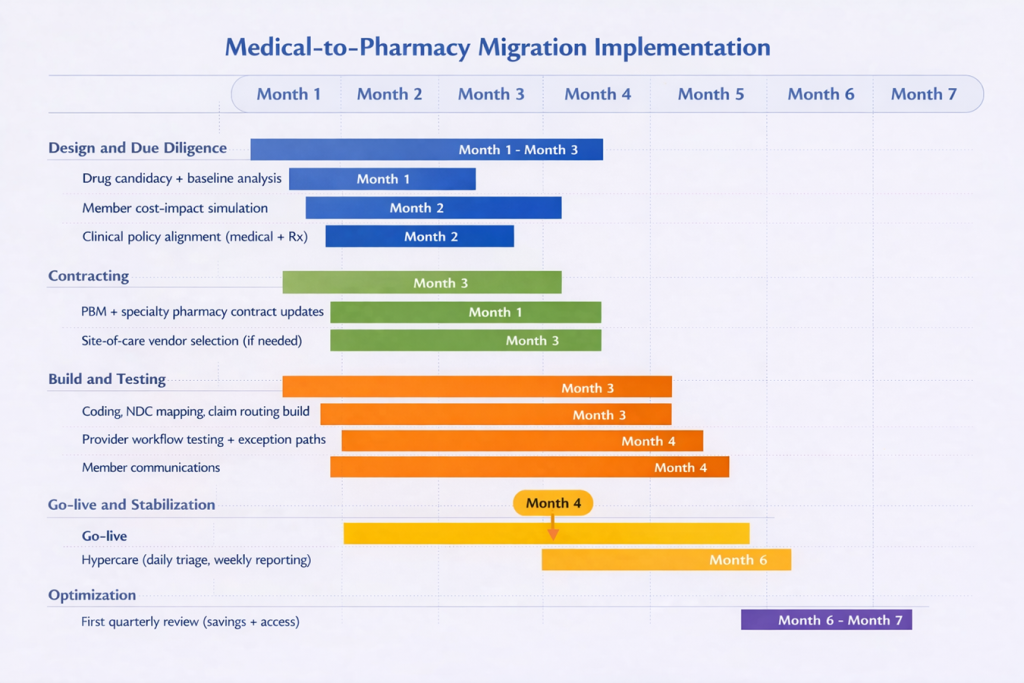

When a plan sponsor decides to move medical benefit drugs to the pharmacy benefit as part of its total cost of care strategy, it shifts the focus from idea to execution. This is where benefit brokers and benefit directors can either create a smooth transition or inherit avoidable disruption. The move is not just a benefit design change. It is an implementation project involving vendors, providers, internal teams, and members. Done well, it can improve control, visibility, and savings. Done poorly, it can create confusion, provider pushback, and member dissatisfaction.

A good decision still needs a good rollout.

The first step is to define exactly which drugs are moving. Not every medical benefit drug belongs on the pharmacy benefit. The best candidates are usually high-cost therapies with repeat use, clear product identification, and a real savings opportunity tied to unit cost, site of care, or utilization management. This is also the point to establish a baseline: current spend, site of care, billing patterns, denial rates, and member out-of-pocket exposure. Without that baseline, vendor savings claims are hard to verify. Payers already require detailed drug identification and accurate unit reporting on many claims, which shows how precise this work needs to be.

The second step is vendor alignment. This is where many implementations begin to fail. The PBM may think it owns the clinical policy, the medical administrator may think prior authorization still sits on the medical side, and providers may not know who is supplying the drug. Those issues need to be resolved before any build work begins. Brokers and benefit directors need clear answers on who handles prior authorization, dispensing, drug billing, administration billing, and exceptions. That matters because medical and pharmacy coverage policies do not always align for the same drug, which can create delays, denials, and provider friction.

The third step is to build and test the workflow before go-live. Claims routing, code mapping, prior authorization rules, specialty pharmacy logistics, exception handling, and reporting all need to be built and tested from start to finish. That means validating the full sequence: physician order, prior authorization, dispensing, provider receipt, drug administration, and claim payment. You cannot treat this as a desk exercise because provider acceptance is a real issue. Some providers and health systems will not accept white-bagged product, or they will accept it only under narrow conditions. That is why clinical groups continue to raise concerns about safety, coordination, and disruption when organizations execute these models poorly.

The fourth step is to protect the member before the transition goes live. This is one of the most overlooked parts of implementation. Moving a drug from the medical benefit to the pharmacy benefit can change how cost share is applied. A drug once covered under medical coinsurance may now fall under a specialty tier, a different deductible, or a separate accumulator. That means the employer may save money while the member pays more, which is not a fiduciary win. One oncology study found that bagging was linked to lower insurer payments but higher patient out-of-pocket costs. Before launch, employers should model member impact, identify likely points of disruption, and prepare clear communications and escalation paths for delays, denials, or provider refusals.

The fifth step is to treat go-live as the start of the proof period, not the finish line. For at least the first 90 days, brokers and benefit directors should monitor denial rates, prior authorization turnaround times, shipment failures, missed administrations, provider complaints, member complaints, and site-of-care shifts. That last point matters because outpatient hospital settings are often materially more expensive than physician offices for comparable services. Savings also need to be measured on a net basis. If spend simply moved from provider markup to PBM markup, the employer did not solve the problem. That is why transparent reporting and tight contract discipline matter just as much after implementation as before it. FTC scrutiny of specialty pharmacy economics is a reminder that more control does not automatically mean better value.

The strategy is set. Now comes the work.

A practical seven month roadmap for shifting eligible therapies from the medical benefit to the pharmacy benefit.

The bottom line is simple. Once the plan sponsor makes the decision, success depends less on the strategy itself and more on how well it manages the transition. Benefit brokers and benefit directors play a central role in keeping the process disciplined, practical, and member-conscious. Employers that approach this move with a clear plan, defined accountability, and strong post-launch oversight are far more likely to achieve the savings they expect without creating unnecessary friction along the way.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.

Most employers do not lose sleep over concert ticket fees. They should still pay attention to Ticketmaster. The reason is simple. Ticketmaster is being criticized for operating in a way that many buyers see as unfair, confusing, and self-protective. According to The Guardian, senators accused the company of raising other charges after rules targeted hidden fees, calling it a bait-and-switch approach rather than real reform. At the same time, the Department of Justice alleges that Live Nation-Ticketmaster’s conduct harms fans, artists, smaller promoters, and venues by weakening competition and preserving its control over the market.

Commercial employers should see the parallel immediately.

The traditional PBM model often works the same way. A large intermediary controls key parts of the transaction, tells the buyer it is delivering savings, and then makes it difficult to determine where money is being earned, retained, or shifted. The product is different, but the outcome can look familiar: the buyer pays more than expected, the contract is hard to interpret, and the middleman keeps defending its role as essential.

That is why the Ticketmaster story matters. It is not really about concerts. It is about what happens when opacity becomes part of the business model. The DOJ says Live Nation-Ticketmaster used exclusionary conduct, long-term exclusive arrangements, and other tactics that limited competition and kept venues from using rival providers. That matters because concentrated control often weakens pricing pressure, blunts innovation, and leaves buyers with fewer practical options than they appear to have on paper.

Employers dealing with PBMs should recognize the pattern.

Here are the similarities.

Who is harmed. In Ticketmaster’s case, the DOJ says the harm falls on fans, artists, smaller promoters, and venue operators. In the PBM market, the comparable groups are employers, plan members, independent pharmacies, and sometimes even consultants or advisers who cannot get complete, reliable claims and pricing data. In both settings, the end buyer and surrounding market participants lose leverage when one intermediary controls too much of the flow.

How they are harmed. The Guardian reports that after hidden-fee rules took effect, Ticketmaster found other ways to preserve revenue. Employers often face the same kind of economic shell game in pharmacy benefits. A PBM may promote rebate improvements or stronger discounts in one area while recovering margin somewhere else through spread pricing, retained rebates, specialty pharmacy markups, inflated dispensing economics, administrative fees, or favorable steering into affiliated channels. The issue is not just high cost. It is cost that moves around faster than the buyer can track it.

Why buyers miss it. Most employers do not review PBM economics line by line. They rely on RFPs, consultant scorecards, guarantee sheets, and headline discount terms. That is where the problem starts. A PBM can look competitive on AWP discounts or rebate guarantees while still retaining value through contract definitions, exclusions, data blind spots, specialty carve-in rules, or opaque reconciliation methods. Ticketmaster’s fee criticism is a useful reminder that disclosure alone does not solve much if the structure still lets the intermediary protect margin elsewhere.

How competition gets weakened. The DOJ alleges that Live Nation-Ticketmaster used its market position and exclusive deals to lock out rivals and reduce real competition. Employers often see a softer but similar version in PBM contracting. Incumbents bundle services, tie data to proprietary systems, make implementation difficult, and use affiliate arrangements to keep clients inside their ecosystem. That does not always violate antitrust law, but it does make the market less open and less accountable.

Why trust breaks down. Buyers can tolerate complexity for a while. What they do not tolerate is the feeling that complexity was designed to keep them from seeing the truth. Once employers begin to suspect that savings in one bucket are being offset by profit-taking in another, the conversation changes. It stops being about vendor performance and starts being about whether the buyer has been managed or misled. That is where reputational damage begins. This is an inference from the reported Ticketmaster fee response and the DOJ’s broader allegations about market conduct.

Employers should also be clear about the likely PBM equivalents of Ticketmaster’s fee reshuffling.

If one revenue stream gets squeezed, margin often reappears somewhere else. It can show up in spread pricing on generic drugs. It can show up in lower rebate pass-through percentages than the client assumed. It can show up in specialty drug dispensing margins through affiliated pharmacies. It can show up in administrative fees, data access restrictions, formulary management payments, or contract language that makes audits technically possible but practically useless. That is why a single “savings” metric is rarely enough. A PBM that loses easy profit in one place may simply hunt for it in another.

Ballooning is when a PBM loses one source of hidden profit, then shifts that profit-taking to another part of the pharmacy benefit.

This is where employers need to stop thinking like purchasers of administrative services and start thinking like fiduciaries. A fiduciary standard of care means asking whether the pharmacy benefit is being managed for the exclusive benefit of the plan and its participants, or whether the structure rewards the intermediary first. That is not a philosophical question. It is a financial one. If the PBM’s compensation rises when the plan spends more, uses more expensive channels, or accepts lower transparency, the employer has a governance problem whether it wants to admit it or not.

Here are practical steps employers can take.

Evaluate total net cost, not isolated discounts. Rebate totals and AWP discounts can be manipulated as standalone talking points. Review ingredient cost, rebates, dispensing fees, administrative fees, specialty pharmacy economics, and every retained revenue stream together.

Force plain-English contract terms. If your team cannot explain how the PBM makes money in two minutes, the arrangement is too opaque. Definitions around spread pricing, rebate pass-through, specialty pharmacy, audit rights, and manufacturer revenue should be explicit and easy to understand.

Test whether savings are real or relocated. After any contract change or “enhancement,” ask one question: did total plan cost go down, or did margin simply move to another line item?

Benchmark specialty separately. This is where many employers lose control. Specialty claims are often the easiest place for a PBM to preserve margin while still reporting attractive overall contract terms.

Strengthen audit rights and use them. Audit language that cannot produce actionable data is window dressing. Employers should insist on timely access to claims detail, rebate detail, channel economics, and affiliate compensation.

Reduce dependence on one black-box vendor. The more functions the PBM and its affiliates control, the harder it becomes to challenge pricing and performance. Carve-outs, pass-through arrangements, and direct contracting deserve serious evaluation.

Hold advisers to the same standard. Employers should expect consultants and brokers to explain not just what a PBM promises, but how the economics work underneath the promises.

Ticketmaster is now dealing with the kind of scrutiny that shows up after buyers decide the system may be working against them. PBMs are on similar ground. Once employers realize that “savings” can be manufactured on paper while money leaks elsewhere, patience runs out. Regulators may act. Litigators may act. Markets may shift. But none of that helps an employer that waited too long to look closely.

The better move is to get ahead of it.

The core lesson is not that PBMs are identical to Ticketmaster. They are not. The lesson is that any middleman that depends on complexity, limited visibility, and shifting revenue streams should expect more skepticism over time. Employers do not need to wait for a subpoena, a lawsuit, or a Senate hearing to respond. They already have enough reason to demand clarity now. That is what a fiduciary buyer does. It does not accept savings claims at face value. It follows the money.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.

In the commercial sector, employers are still being told that pharmacy benefits are too complex to fully understand, too specialized to directly manage, and too entrenched to meaningfully change. That story falls apart the moment you look at Caterpillar.

More than 20 years ago, Caterpillar decided the prescription drug supply chain was bloated, conflicted, and wasting money. Instead of accepting the usual PBM talking points, the company did what too few employers have done since. It followed the money, challenged the middlemen, and redesigned the purchasing model around transparency, direct accountability, and measurable value.

That is what makes the Caterpillar story so relevant today. It is not a tale about a clever contract tweak. It is proof that large employers have had a workable blueprint for fixing pharmacy benefits all along. Most just chose not to use it.

According to Todd Bisping’s 2010 account, Caterpillar’s prescription drug spend had been rising about 14% per year from 1996 through 2004. Brand drug prices had doubled since 2004. After the company began actively managing generic utilization, formulary strategy, and the supply chain, it reported that by 2009 total drug costs were 6.8% lower than in 2004 and per-member-per-year costs were 13.8% lower, even while employee and retiree copayment tiers generally remained unchanged from 2002 levels.

Read that again. Lower costs. Stable member cost sharing. No magical innovation. No AI dashboard. No new law required. Just an employer refusing to tolerate waste. Caterpillar’s leadership started with a simple but powerful observation.

Their internal analysis suggested that 10% to 25% of the prescription drug supply chain contained waste, some of it driven by conflicts of interest. They specifically pointed to the fact that some consultants advising plan sponsors on PBM selection were also receiving broker fees from the PBMs being evaluated. That is not alignment. That is a rigged purchasing process dressed up as expert guidance.

So Caterpillar attacked the problem at its root.

The company pushed for transparency standards through the HR Policy Association coalition, then treated transparency not as the goal, but as the starting point. That distinction matters. Transparency by itself does not save a dime. It only gives an employer the ability to see where the waste lives and who is benefiting from it. Caterpillar then used that visibility to do what the market said could not be done: directly negotiate with major pharmacies outside the standard PBM pricing structure.

Its goals were straightforward. Find major pharmacy partners willing to contract directly. Preserve non-exclusive arrangements. Replace average wholesale price with a more rational pricing method. Ensure true price transparency. Caterpillar struck deals with Walmart and Walgreens that were built around those principles.

The most important part of the model was the pricing methodology. Caterpillar rejected AWP and moved to a cost-plus framework based on actual invoice cost, overhead, and margin. In plain English, the company wanted to know what the drug really cost, what it reasonably took to dispense it, and what profit the pharmacy would earn. That is how serious buyers purchase almost everything else. Employers should ask themselves a blunt question: why has pharmacy been allowed to operate under looser rules than office furniture, freight, or industrial supplies?

Caterpillar showed employers what happens when you stop handing the keys to a PBM. Take control of the pharmacy benefit, and waste gives way to transparency, accountability, and real savings.

Caterpillar also insisted on audit rights. That may be the most underappreciated part of the story. Any vendor can promise transparency. A serious buyer builds in the right to verify it. Caterpillar understood that a pricing method without audit rights is just another act of faith.

Then came the network strategy. With two-year contracts effective January 1, 2010, Caterpillar said Walgreens and Walmart provided geographic access to more than 90% of participants. The company built a preferred network around those pharmacies, kept copays unchanged there, and imposed higher cost sharing outside the preferred network. Over the term of those contracts, Caterpillar expected savings “well into 8 figures.”

This is where many employers still get lost. They assume disruption means taking something away from members. Caterpillar showed the opposite. If you remove waste from the supply chain, you can improve the economics without immediately shifting more burden to employees. That is what disciplined purchasing looks like.

So why did Caterpillar solve this problem years ago while so many employers remain stuck in the status quo?

Part of the answer is convenience. The traditional PBM model asks employers to outsource difficult thinking. It packages complexity into glossy reports, benchmark language, rebate guarantees, and contract terms that sound protective but often preserve the same structural conflicts. Employers are told they are buying expertise when in many cases they are buying opacity.

Another part is fear. Many plan sponsors have been conditioned to believe that direct contracting, transparent pricing, or fiduciary oversight is too disruptive, too niche, or only feasible for unusually large employers. Caterpillar disproved that assumption. The company did not eliminate every intermediary. It redefined their role. It kept partners that added value and challenged those that extracted value without earning it.

That distinction matters even more now because the broader market has started catching up to what Caterpillar recognized years ago. The FTC’s July 2024 interim report found that the six largest PBMs managed nearly 95% of prescriptions filled in the United States and said increasing vertical integration and concentration enabled PBMs to profit while inflating drug costs and squeezing independent pharmacies. The FTC’s January 2025 second interim report said the big three PBMs marked up many specialty generic drugs significantly.

In other words, the concerns Caterpillar acted on in 2004 are no longer dismissed as fringe complaints. They are now being validated by federal investigators.

That should be a wake-up call for every employer in the commercial market.

The future of pharmacy benefits will not belong to employers who negotiate the best rebate story. It will belong to employers who build plans around transparent net cost, aligned incentives, and independent oversight. The market is moving, although not fast enough. Employers that wait for perfect regulation or unanimous consultant support will remain trapped in a model designed to reward middlemen more than plan sponsors and members.

Here is what employers should be doing now.

They should stop judging PBM performance primarily by discounts, rebates, and guarantees that can be manipulated within an opaque system. Those metrics often distract from the real question: what is the total net cost after all revenue streams, spread, fees, and channel steering are accounted for?

They should demand contract language that identifies every source of PBM compensation and every affiliated entity touching the claim. If money changes hands anywhere in the arrangement, the employer should know who received it, why, and whether it reduced plan cost.

They should require pass-through economics, independent audit rights, and a pricing model tied to verifiable acquisition cost wherever possible. A vendor that resists transparency is telling you more than enough.

They should revisit pharmacy network strategy. The commercial sector has more leverage than it acts like it has. Employers can steer volume, reward efficient channels, and contract with organizations willing to compete on price and service instead of relying on black-box arrangements.

They should also rethink advisor alignment. A consultant cannot credibly represent the employer’s interest while receiving compensation tied to the vendor being evaluated. That is not a technical flaw. That is the flaw.

Most of all, employers need to adopt a fiduciary mindset. That means treating pharmacy benefits as a managed asset, not a mysterious carveout. It means asking harder questions, accepting less marketing theater, and refusing to tolerate compensation models that depend on concealment.

Caterpillar did not fix every problem in pharmacy benefits. But it proved something that still unsettles the status quo: employers have far more power than they are led to believe. The lesson for the commercial sector is not that Caterpillar was unusually bold. It is that too many others have been unusually passive.

The next era of pharmacy benefits will be defined by inherent transparency, fewer conflicts of interest, and tighter employer oversight. The employers that prepare now will be in position to lower costs without gutting benefits. The ones that do not will keep paying for opacity and calling it strategy.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.

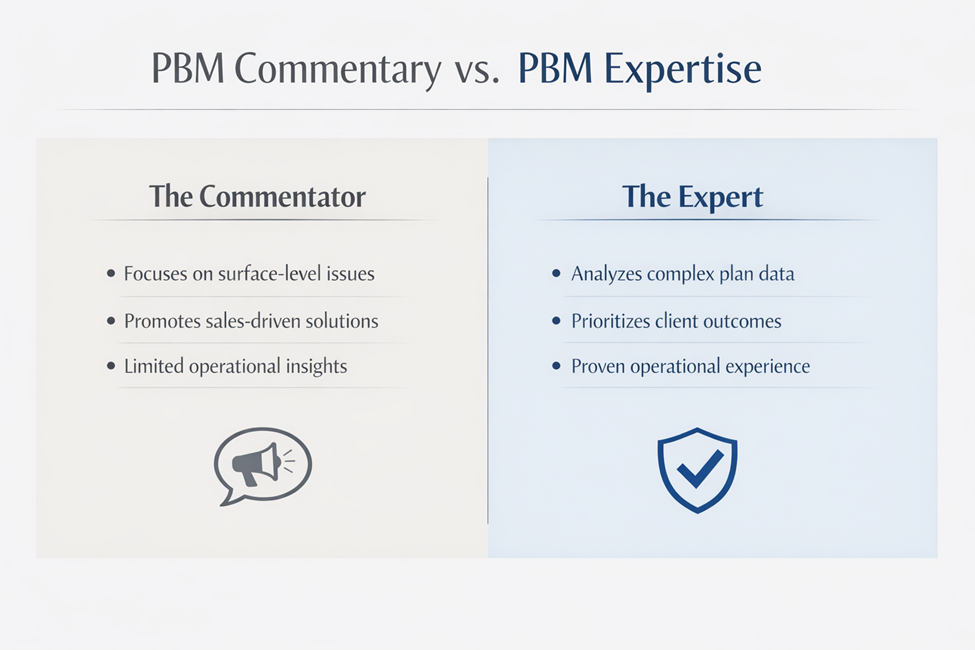

Anyone can claim to be a PBM expert. Proving it is another matter. In pharmacy benefit management, expertise should be measured by more than a title, years in the business, or a polished sales presentation. Employers, consultants, and other plan fiduciaries need stronger evidence, especially when the financial and clinical stakes are so high. In my view, the hallmarks of a true PBM expert is demonstrated through a combination of:

Education and formal training

Applied experience

Teaching

Measurable results

A solid foundation of formal learning is one part of that equation. Certifications and structured training can help confirm that a person understands the core components of pharmacy benefit management, including formulary strategy, rebate structures, utilization management, contract terms, and compliance obligations. That matters. But education by itself does not make someone an expert. It simply establishes that the person has done the work to understand the fundamentals.

The next layer is the ability to communicate that knowledge clearly. Professionals who consistently publish articles, white papers, or practical commentary on PBM issues tend to separate themselves from those who rely on general claims. Writing well about complex topics requires more than familiarity. It requires command of the subject. The same is true for teaching. People who lead workshops, train advisors, or educate plan sponsors on how PBM contracts work often demonstrate a deeper level of mastery because they can translate technical material into practical guidance.

Operational experience is equally important. There is a meaningful difference between knowing how the system should work and understanding how it actually works in practice. Experience managing pharmacy programs, evaluating contracts, auditing claims, or overseeing benefit strategy gives professionals a more grounded view of where value is created and where cost leakage occurs. That kind of experience sharpens judgment in ways that theory alone cannot.

Most PBM “experts” comment on the system. Few can fix it.

Still, the most persuasive evidence of PBM expertise is results. Can the individual point to examples where pharmacy spend was reduced without compromising care? Can they show how a plan sponsor improved contract performance, gained pricing clarity, or corrected misaligned incentives? Can they demonstrate that their recommendations produced measurable savings or better oversight? Those are the kinds of outcomes that move a person from knowledgeable to credible.

Recognition from outside the organization can add to that credibility. Media interviews, conference presentations, advisory roles, and industry invitations all help reinforce a professional reputation. But those signals should support the case, not define it.

For employers and consultants evaluating PBM expertise, the standard should be straightforward. Look for someone with formal training, a track record of educating others, practical operating experience, and documented outcomes. Most important, look for someone who understands the fiduciary implications of PBM decision-making and can connect strategy to accountability.

That is the real test. A PBM expert should not only understand the system. They should be able to explain it clearly, identify where it works against the plan sponsor, and recommend changes that improve financial performance and protect the employer’s interests. Anything less may be experience, but it is not expertise.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

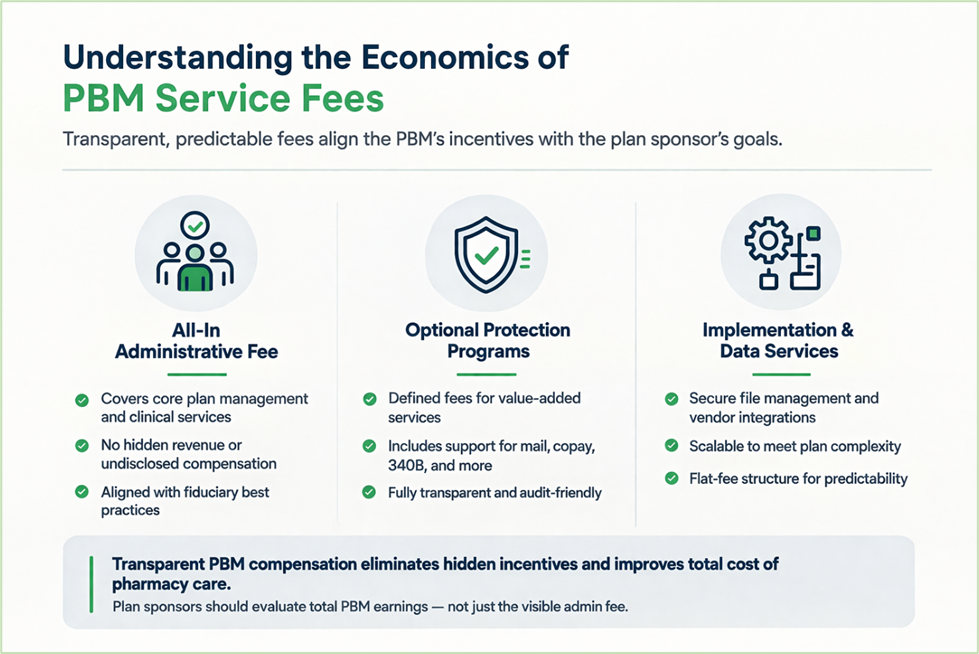

When employers think about how to assess PBM service fees, most still look at the wrong number. They focus on the administrative fee instead of total compensation. That approach has allowed PBMs to quote a low visible fee while collecting far more through hidden revenue streams. A better way to evaluate PBM compensation is Earnings After Cash Disbursements, or EACD. As I explained in my earlier post on PBM math, EACD reflects what the PBM keeps after paying pharmacies and disbursing other required cash flows.

In plain English, it shows what the PBM actually earns to manage your drug benefit. That matters because PBMs have historically hidden compensation in places most employers never thought to examine. A contract might show a modest admin fee, while the PBM quietly earned more through spread pricing, specialty markups, retained rebates, network differentials, data fees, and affiliate arrangements.

That is why an artificially low admin fee should raise concern, not confidence. In many cases, the low fee was never a sign of efficiency. It was a signal that the PBM expected to make up the difference somewhere else. Said differently, the admin fee was the decoy. The real money was buried in the mechanics of the program. That model gave PBMs a blank check.

Now the market is changing. Greater scrutiny and new disclosure requirements are making it harder for PBMs to hide how they get paid. That is good news for plan sponsors, but it also means employers need to reset their expectations. If a PBM built its business on self-dealing and off-contract revenue, a truly transparent arrangement will not come with a bargain-basement fee. Plan sponsors should expect all-in administrative fees in the range of $30 to $50 PMPM from PBMs that historically profited from hidden compensation. That number may sound high to buyers accustomed to teaser pricing, but it is often more honest and easier to evaluate.

The real question is not whether the fee looks low. The real question is whether the fee reflects the PBM’s full compensation.

That is where understanding how to assess PBM service fees becomes practical, not theoretical. A transparent pricing model should show plan sponsors exactly what they are paying for. A cleaner structure might include a base administrative fee, a defined fee for optional protection services, and a separate charge for additional file integrations or other clearly scoped work.

Understanding PBM service fees starts with one principle: what you see should be what you pay

Consider two PBM proposals for the same self-funded employer. One PBM offers a $4 PMPM administrative fee. Another offers a much higher all-in $16 PMPM service fee with clearly defined services and no hidden revenue rights. Many employers would instinctively lean toward the $4 offer. That would be a mistake. If the low-fee PBM owns pharmacies, controls specialty distribution, retains undisclosed income, or profits from dispensing spreads, the plan sponsor will likely pay more in the end. Fully transparent PBM service fees often look higher than legacy teaser rates because disclosed compensation is replacing revenue that was once hidden in the contract.

So what should plan sponsors do?

Start by demanding full compensation disclosure in writing. Do not settle for a narrow definition of admin fees. Require the PBM to disclose every direct and indirect source of revenue tied to your plan, including spread income, retained rebates, manufacturer payments, pharmacy fees, specialty margins, data income, and affiliate profits.

Move away from shared savings arrangements. They often reward the PBM, or other vendors, for gaming the baseline, then charging you a percentage of the problem it helped create. A fiduciary-minded buyer should prefer fixed, transparent compensation.

Build an internal PBM oversight team. Do not leave pharmacy benefits buried inside a general health plan workflow. Assign clear roles across benefits, finance, procurement, legal, and clinical support so someone is accountable for contracts, data review, utilization management, and vendor oversight. You do not need a new department, but you do need a focused team that treats pharmacy like a major financial asset rather than an HR side task.

Scrutinize pharmacy reimbursement terms, especially dispensing fees. Benchmark them against NADAC-plus models where appropriate and make sure the contract clearly defines what the “plus” includes. Ambiguity is where abuse starts.

Get educated before you go to market. If your team does not understand EACD, spread pricing, specialty pharmacy economics, or vertical integration risk, you are negotiating from a position of weakness.

Stay away from PBMs that own pharmacies whenever possible. Ownership creates conflicts that are difficult to police and even harder to unwind after the contract is signed. Most of all, stop buying PBM contracts based on what looks cheap. Buy based on what is clear, auditable, and aligned with your interests. Low fees do not save employers money. Clean economics do.

When Transparent Fees Lose to Teaser Pricing

I have sat in more RFP meetings than I can count where the reaction was immediate. I would walk through a fully transparent model, explain exactly how we get paid, and then show the management fee. You could see it on their faces. Some leaned back. Others stopped taking notes. A few exchanged looks. The number felt too high compared to the other bids on the table.

Then the conversation would shift to the competitor quoting a fraction of the fee. On paper, it looked like an easy decision. Lower admin cost, similar guarantees, same language. What was not visible in that moment was how that low fee would be recovered elsewhere through spread, pharmacy economics, or other undisclosed revenue. In many of those cases, the lower bid won.

That pattern tells you everything you need to know. PBM services are not inexpensive when structured honestly. You either see the cost upfront, or you find it later buried in the claims. The objective is transparency and value, so buyers can evaluate total compensation and make a decision they can defend long after the contract is signed.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

A recent court ruling involving JPMorgan Chase should concern every self-insured employer. A federal judge allowed employees to move forward with part of a lawsuit alleging the company mismanaged its health and prescription drug benefits program, resulting in higher drug costs and premiums. On its face, the case is about one employer. In practice, it reflects a much larger shift in how courts, regulators, and plan members are viewing pharmacy benefit oversight.

For years, employers have asked a reasonable question: How can we be held responsible for fiduciary liability when PBMs refuse to share the data needed to perform that duty? It is a fair point. In many cases, the employer is expected to act as a prudent fiduciary while the PBM controls claims data, rebate terms, spread pricing, pharmacy reimbursements, network arrangements, and formulary strategy. Employers are often asked to oversee a system they cannot fully see.

But the legal environment is changing. Judges may understand the frustration, yet still expect plan fiduciaries to monitor vendors, question compensation, and avoid unreasonable arrangements. In plain terms, lack of transparency may explain the problem, but it may not excuse inaction.

Education matters more now than ever for HR leaders.

That is what makes the JPMorgan case important. It suggests that if employees can plausibly claim a plan paid too much, a PBM benefited from the arrangement, and the employer failed to exercise proper oversight, the case may survive long enough to reach discovery. That alone changes the risk profile for self-insured employers. Once a case gets past an early dismissal attempt, internal documents, contracts, fee structures, and oversight practices can all come under a microscope.

This did not happen in a vacuum. The PBM industry is under pressure from multiple directions. Federal regulators have raised concerns about market concentration, vertical integration, opaque compensation, and inflated drug prices. State lawmakers continue to push new PBM reform measures. The Department of Labor is also moving toward greater fee disclosure in ERISA-covered plans. Taken together, these developments send the same message: pharmacy benefits are no longer a black box that employers can afford to ignore.

The implications reach far beyond PBMs.

Employers will face greater pressure to prove they are actively overseeing pharmacy benefit arrangements, not merely accepting consultant recommendations or carrier reporting.

Brokers, consultants, and other advisors will be expected to deliver more than benchmarking reports and renewal talking points. Clients need contract analysis, claims-level insight, and real oversight.

TPAs and carriers will face increasing demands for better integration, cleaner reporting, and clearer lines of accountability across the full health plan.

PBMs will face more pressure to explain how they are paid, what revenue exists outside the stated administrative fee, and whether plan sponsors are truly receiving the value they were promised.

Employees and plan members may become more willing to challenge benefit practices when they believe plan costs were inflated or fiduciary duties were ignored.

Drug manufacturers may also face more attention as policymakers and employers look more closely at list prices, rebate structures, and other distortions that affect net cost.

Self-insured employers should not read this case as a reason to panic. They should read it as a reason to stop delaying action.

Regulation will help, but it will not solve the employer’s problem by itself. Rules can create disclosure requirements. They cannot create judgment. They cannot teach a finance leader, HR executive, or benefits committee how to spot a bad PBM contract, a weak guarantee, or a rebate arrangement that looks attractive on paper but drives up total cost. More disclosure is useful only if the employer knows what to look for and what to challenge.

That is why education matters now more than ever. But employers need to be careful about where they get it. Everyone is a thought leader now, especially with AI making it easier to sound informed. Sounding informed is not the same as knowing how PBM contracts work in the real world. It is not the same as understanding where margin hides, how specialty costs are manipulated, why guarantees often miss the point, or how to restructure a pharmacy program without shifting risk back onto members.

Self-insured employers do not need more polished commentary. They need practical guidance from people who have actually done the work. They need thought doers, not thought leaders. They need advisors who have negotiated PBM contracts, audited claims, challenged rebate narratives, rebuilt formularies, and dealt with the operational fallout when the numbers did not match the sales pitch.

This is no longer a passive compliance issue. It is a fiduciary standard of care issue.

Employers should be asking direct questions right now. Who owns the data? Can we access claims-level detail? How is the PBM paid, both directly and indirectly? What compensation exists outside the stated admin fee? Are rebates reducing net plan cost, or are they masking bad unit prices? Do we have meaningful audit rights? Can we exit the arrangement without disruption or leverage being used against us?

If those questions make a vendor uncomfortable, that is revealing. The old defense has been that employers cannot fulfill their fiduciary duty without the data. There is truth in that. But the better response now is not resignation. It is action. Demand transparency. Tighten contract language. Document oversight. Reassess the role of every intermediary involved in the pharmacy benefit. Most important, get educated by people who understand both the theory and the execution.

The JPMorgan case does not prove every employer has failed. It does show that the standard is changing. When pharmacy benefit decisions are challenged in court, the issue will not be whether the system is opaque. Everyone already knows that. The issue will be whether the employer acted like a fiduciary anyway. For self-insured employers, the message is clear: you are now on the clock.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.

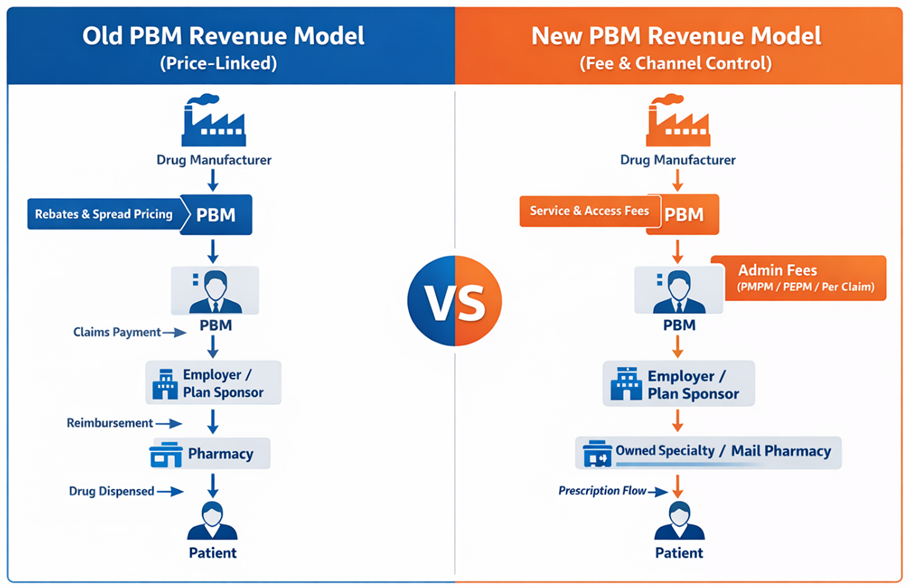

Mark Cuban recently posed a simple but important question: if pharmacy benefit managers can no longer generate revenue as a percentage of drug list prices, where will the money come from?

The answer is straightforward. It will come from somewhere else. Revenue in the PBM industry rarely disappears. It shifts. As regulatory pressure increases on spread pricing and rebate-driven compensation, vertically integrated PBMs are repositioning how they generate margin. The industry is transitioning away from price-linked income and toward fee-based services and control of dispensing channels.

The Shift from Drug Price Revenue to Service Fees

For years, PBM profits were closely tied to the price of drugs. Rebates and spreads provided a steady stream of revenue that was largely invisible to employers. That model is now under scrutiny from regulators and plan sponsors. In response, PBMs are replacing percentage-based compensation with administrative service fees that are billed directly to employers.

Charging administrative fees is not inherently problematic. Employers should expect to pay PBMs for legitimate services such as claims processing, clinical oversight, network management, and reporting. The concern lies in how these fees are structured and whether they accurately reflect the value being delivered.

PBMs typically bill administrative services in one of three ways: per paid claim, per employee per month (PEPM), or per member per month (PMPM). While each structure can produce similar economics if priced properly, the incentive structure behind the fee matters greatly. Employers should carefully examine how these fees align with the PBM’s financial interests.

One structure employers should avoid entirely is percentage-of-savings compensation. This arrangement often appears in carve-out programs, particularly those targeting specialty drugs or cost-containment initiatives. The PBM promises to reduce costs and retain a percentage of the “savings.” However, the PBM often controls how savings are defined and measured. If the starting price is inflated, the reported savings can appear significant even when the employer is still paying more than necessary.

Percentage-of-savings models create a troubling incentive. High claim volumes and inflated baseline prices can increase the PBM’s share of the savings calculation. Employers end up rewarding the very behavior they are trying to control.

Where Vertically Integrated PBMs Will Find New Margin

At the same time, many PBMs are introducing layered PMPM service fees. Clinical programs, utilization management initiatives, data analytics platforms, and reporting systems are increasingly being packaged as separate cost-management services. Functions that were once embedded in the PBM contract are now itemized and billed individually. Some of these programs provide real value. Others represent services PBMs were already expected to perform as part of basic plan administration.

Side-by-Side Flow: Old Revenue Model vs. New Revenue Model

Meanwhile, vertically integrated PBMs are shifting margin downstream into businesses they own. Specialty pharmacies, mail-order facilities, and affiliated dispensing channels have become central to their economic strategy. When the PBM controls the formulary, the pharmacy network, and the prescription routing process, it can direct prescriptions into pharmacies it owns or controls. The margin generated by dispensing then appears within the pharmacy operation rather than in the PBM contract itself.

This strategy allows vertically integrated organizations to preserve profitability even as traditional rebate structures face scrutiny. The economics shift from price control to channel control. Another emerging revenue source involves manufacturer “service fees.” These payments are often described as compensation for market access, data analytics, or clinical program support. While the terminology has changed, the underlying financial relationship between manufacturers and PBMs frequently remains intact.

All of this illustrates an important point: transparency alone is not enough. What is happening now goes beyond transparency. Plan sponsors are beginning to examine PBM economics much more closely. In other words, pocket-watching has begun. Employers are no longer satisfied with rebate guarantees or assurances of pass-through pricing. They want to understand the entire financial structure supporting their pharmacy benefit program. Administrative fees, channel margins, manufacturer payments, and program charges must all be evaluated together.

The CPBS Way: Running an RFP That Actually Works

The most effective way to achieve that visibility is through a well-run request for proposal and continuous monitoring. A disciplined RFP process forces PBMs to disclose how they generate revenue and what services they are charging for. It allows plan sponsors to compare competing models and determine which PBM offers the best overall value. In the CPBS framework, an effective PBM RFP follows a structured process designed to eliminate ambiguity and marketing theater. The “CPBS Way” relies on six steps to produce meaningful comparisons and enforce accountability.

Require consulting firms and plan sponsors to have skilled staff with extensive PBM knowledge. Without subject-matter expertise, critical contract provisions and pricing mechanisms often go unchallenged.

Draft an entirely new PBM contract that eliminates common loopholes. Allowing PBMs to submit proposals using their own contract templates invites hidden revenue opportunities.

Develop a questionnaire that seeks only verifiable information. Marketing claims and projections should be excluded in favor of responses that can be validated through contract language or audit rights.

Conduct extensive legal negotiations with remaining PBM candidates early in the process. Key contractual issues should be resolved before finalists are selected.

Select semi-finalists based on binding contract terms and firm pricing commitments rather than marketing narratives.

Conduct finalist presentations that function as validation sessions, not marketing contests. At this stage, the focus should be operational capability and clarification of remaining issues.

Administrative pricing can also serve as an important signal. When a PBM proposes an all-in administrative fee below ten dollars PMPM, employers should approach the offer with caution. Operating a compliant PBM platform with meaningful clinical programs, reporting infrastructure, and member support requires real investment.

If the administrative fee appears artificially low, the PBM will almost certainly recover margin somewhere else. That recovery often occurs through pharmacy channel ownership, specialty dispensing margins, or additional program fees.

There is no such thing as a free PBM. For employers, the focus should shift from individual pricing components to the total economic picture. Administrative fees, dispensing margins, specialty pharmacy economics, and program charges must all be considered together.

The real question is not whether PBMs will replace rebate income with service fees. That transition is already underway. The real question is whether employers fully understand the total fee stack they are paying and whether those fees produce measurable results for their plan and their members.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.

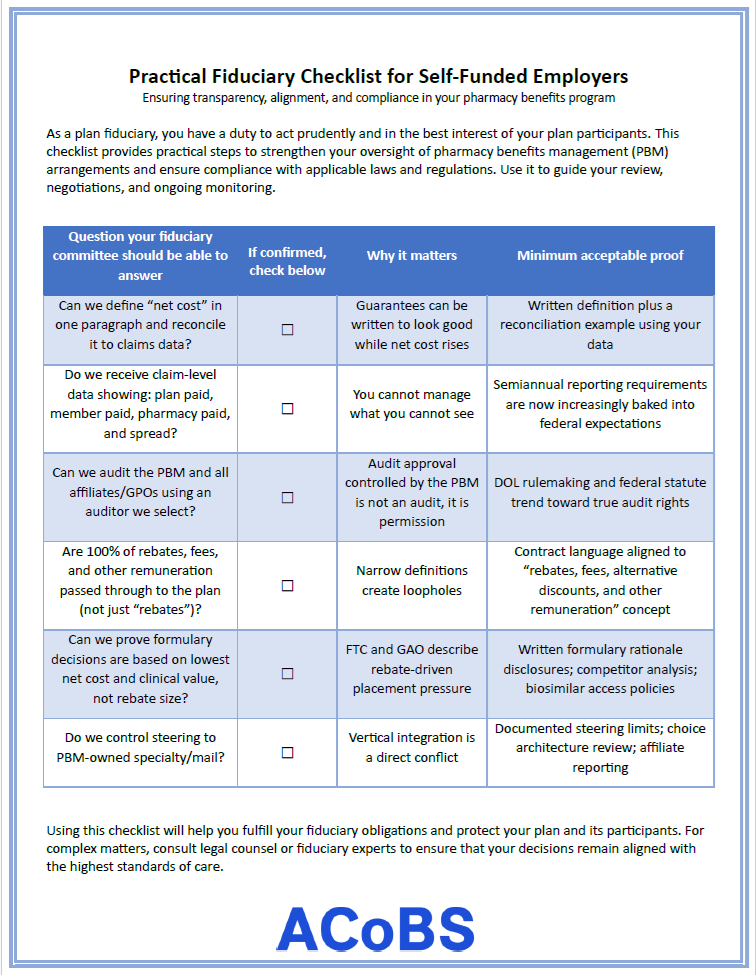

Self-funded employers operate under a prudent expert standard. The Consolidated Appropriations Act raised the bar. A good faith effort is not enough. Plan fiduciaries must understand what they are buying, what they are paying, and whether the arrangement serves participants, not intermediaries. A practical fiduciary checklist is not theoretical. It is operational.

Confirm true independence. Require written disclosure of all direct and indirect compensation paid to your PBM and your consultant. Indirect revenue, side agreements, rebate aggregators, and affiliated entities matter. If your advisor receives compensation from a PBM, you do not have a buyer’s agent. You have a seller’s agent. Replace conflicted vendors if necessary.

Define value before you define rebates. Rebates are not value. Net cost by drug class, appropriateness, waste reduction, and total cost of care are value. Demand reporting that shows ingredient cost, dispensing fee, member cost share, and all manufacturer revenue tied to your utilization. If you cannot see the full economics at the claim level, you cannot meet a fiduciary standard.

Control the formulary. Your PBM’s P&T committee is not automatically aligned with you. Vertical integration and rebate-driven placement can bias decisions toward high-list-price drugs. Require a value-based formulary that prefers generics and biosimilars when clinically appropriate. Prohibit favoring a higher list price drug solely because it generates a larger rebate. Demand quarterly formulary updates and written justification for material changes.

Download the Checklist

Tighten utilization management. Prior authorization approval rates north of 90 percent signal process failure. Protocols should be clinically grounded, documented, and consistently applied. Prohibit off-label expansion designed to increase rebate flow. Insist on reporting that shows approval rates, step therapy compliance, and exception patterns by drug class. Own the data. You must have full access to claims files, historical data, and rebate invoices. Require clear identifiers for 340B claims, specialty drugs, MAC pricing, coupon usage, and exclusions from guarantees. If you cannot independently reprice claims, conduct market checks, and audit rebate agreements, you are relying on representations, not evidence.

Eliminate guarantee games. Forbid offsets where overperformance in one guarantee masks underperformance in another. Define rebates broadly to include all manufacturer payments, not just what the PBM chooses to label as a rebate. Close loopholes tied to definitions of generic, specialty, or excluded drugs.

Audit aggressively. Retain an independent auditor with unrestricted access to contracts, pharmacy records, and rebate agreements. No blackout periods. No PBM veto over auditor selection. Annual audits should assess pricing, rebate pass-through, formulary compliance, and contract adherence.

Separate 340B economics. Require separate identification and pricing treatment of 340B claims. Do not allow inflated list pricing to persist without rebate offset. If 340B savings are not passed through, you are subsidizing intermediaries.

Fiduciary governance in pharmacy benefits is not about squeezing another basis point from a discount off AWP. It is about knowledge. Knowledge of definitions. Knowledge of financial flows. Knowledge of clinical appropriateness.

If you do not understand the mechanics, you cannot discharge the duty. If you do understand them, you can realign the system to serve the only constituency that matters: your plan participants.

How to Know If You Are Falling Short

This checklist is a governance test. Missing one item may signal a process gap. Missing two or three signals exposure. If the gaps are administrative, such as delayed reporting or incomplete benchmarking, you likely have an operational weakness that can be corrected.

If the gaps involve financial transparency, audit rights, data ownership, conflicted compensation, or formulary control, the risk is structural. These are not minor deficiencies. They directly affect whether plan assets are being managed solely in the interest of participants, as required under a prudent expert standard.

You should assume you are out of alignment if:

You cannot document every source of PBM and consultant compensation tied to your plan.

You do not have full audit rights, including access to rebate agreements and subcontractors.

You cannot independently reprice claims or validate net cost by drug class.

You permit guarantee offsets that mask underperformance.

You rely on your PBM’s formulary decisions without independent review.

Two or three misses in these areas are not cosmetic. They mean you cannot verify alignment. And if you cannot verify alignment, you cannot demonstrate prudent oversight. The practical rule is simple: If a gap limits transparency or independence, treat it as a fiduciary risk until corrected. Gaps become failures only when they are ignored.

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.

If you are a self-funded employer, your health plan is the payer of last resort. Every hidden spread, every rebate-driven formulary choice, every “mandatory” specialty pharmacy shift, every opaque fee that is not clearly defined in writing comes out of plan assets. That is money you could have used to lower contributions, avoid benefit cuts, or invest in people.

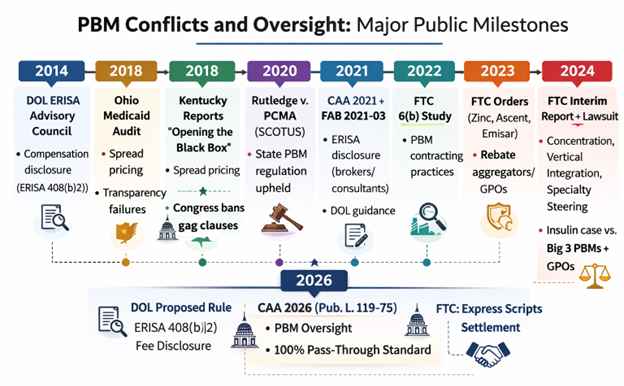

The conflict problem is not theoretical. Federal and state findings describe a market that is both highly concentrated and heavily vertically integrated. The Federal Trade Commission’s interim staff report found the top three PBMs processed nearly 80 percent of U.S. prescriptions in 2023 and the top six processed more than 90 percent, with the largest PBMs integrated into insurers and pharmacies (1). The same FTC report found PBM-affiliated pharmacies account for nearly 70 percent of specialty drug revenue and documented two specialty-generic case studies where PBM-affiliated pharmacies were often paid 20 to 40 times the National Average Drug Acquisition Cost (NADAC), with nearly $1.6 billion in dispensing revenue above NADAC for those two drugs (2020 through part of 2022).

Regulators are now putting “fiduciary standard of care” into the PBM conversation in a way that self-funded employers have wanted for years. In early 2026, DOL proposed a PBM fee disclosure rule under ERISA section 408(b)(2) designed to force disclosure of direct and indirect compensation and to give plan fiduciaries audit rights (2). In February 2026, Congress enacted the Consolidated Appropriations Act, 2026 (Public Law 119-75), adding major PBM oversight and transparency provisions for group health plans and, critically, wiring 100 percent pass-through of “rebates, fees, alternative discounts, and other remuneration” into ERISA plan contracting standards on a defined timeline (3).

Why self-funded employers become the “payer of last resort”

Self-funded plans do not “buy insurance” for the pharmacy benefit in the way fully insured groups do. They fund claims. That makes PBM incentives a governance issue, not just a procurement issue.

ERISA already expects plan fiduciaries to understand what service providers are paid and to ensure compensation is reasonable. In 2014, the ERISA Advisory Council examined whether PBMs should be required to disclose fees and compensation so plan sponsors could meet ERISA’s “reasonable compensation” expectations under section 408(b)(2) (4). Twelve years later, DOL’s 2026 proposed rule is basically the government acknowledging the obvious: PBM compensation is complex, can come from multiple directions, and is difficult for fiduciaries to evaluate without standardized disclosure and audit rights (5).

A second layer that self-funded employers often underestimate is the broker/consultant channel. A STAT investigation reported that some consulting firms may be paid by PBMs on a per-prescription basis, with sources describing at least $1 per prescription and up to $5 per prescription in extreme cases, plus other forms of compensation. Whether every allegation in the market pans out is almost beside the point: if your advisor is compensated by the entity they are supposed to challenge, it weakens your fiduciary posture and your negotiating leverage. “Vendor selection” becomes “vendor placement.”

If your PBM, your broker, or your consultant cannot give you a clean compensation story in writing, they are not operating at a fiduciary standard of care. They are operating at a sales standard.

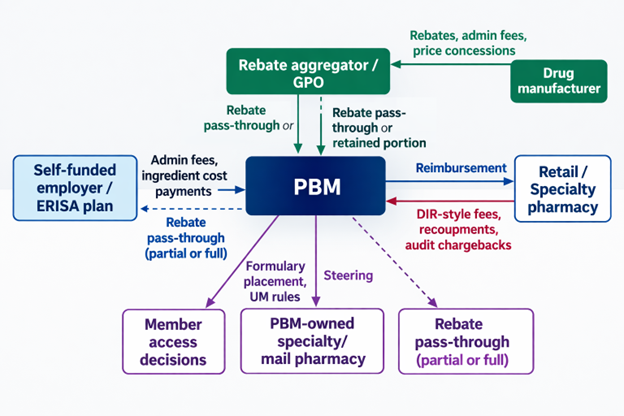

The conflict map: how PBMs make money and how each conflict hits employers

PBMs offer real services: network contracting, claims adjudication, formularies, utilization management, and rebate negotiation. The problem starts when the PBM’s profit depends on decisions that make the plan spend more, not less.

To keep this practical, here are the main conflict types you asked for, framed as “what it is,” “how the PBM wins,” and “how the self-funded employer loses.”

Rebate steering and rebate-driven formularies: manufacturers pay rebates and fees tied to formulary placement and market share. Those arrangements can reward high list prices and large rebates rather than low net cost. The FTC has warned that rebate and fee agreements used to secure exclusion of lower-cost products may incentivize steering to higher-cost drugs and block competition from cheaper generics and biosimilars (6). A self-funded employer loses twice: higher gross ingredient cost today, and a plan design reality where members’ deductibles/coinsurance are often based on gross prices, not net prices after rebates.

Formulary control as a profit center: formulary placement is not just “clinical.” It is a pricing lever. Economic research on rebate contracting and formulary design shows how formulary position can be traded for rebate value, which means the PBM’s “preferred drug” is not automatically the plan’s lowest net option (7). Employers get marketing language about “rebate guarantees” and “discounts,” but the real harm shows up in which drugs get preferred tier status and which lower-cost competitors get boxed out.

Spread pricing: spread is the margin between what the plan (or its carrier/TPA) pays the PBM and what the PBM reimburses the pharmacy. State audits show how large this can be in public programs. Ohio’s Auditor found total spread of $224.8 million in a 12-month period (Apr 2017–Mar 2018), with generic spread representing 31.4 percent of amounts paid for generics in that dataset (8). Kentucky’s “Opening the Black Box” report found PBMs were paid $957.7 million through MCOs for spread-pricing contracts in CY2018, with $123.5 million (12.9 percent) not paid to pharmacies and kept by PBMs as spread (9). Self-funded employers should treat these as warnings because the same mechanics exist in commercial contracts, just with fewer public audit rights.

PBM ownership of specialty pharmacies and specialty steering: vertical integration turns “benefit management” into self-preferencing. The FTC found PBM-affiliated pharmacies now account for nearly 70 percent of specialty drug revenue, and documented steering mechanisms and pricing outcomes that favor affiliated channels (1). When the PBM owns the specialty pharmacy, the plan is effectively negotiating with a party that can move volume to itself and capture dispensing margin. As one industry benefits leader put it, the Big 3 control both the “rebate pipeline” and the “utilization pipeline,” creating a closed loop.

Gag clauses and “clawbacks” at the pharmacy counter: historically, some contracts limited pharmacists from telling patients when a cheaper cash price existed. Congress passed two laws in 2018 aimed at banning gag clauses in private plans and Medicare, reflecting the view that these restrictions caused overpayment at the point of sale (10). Even after gag clause bans, disputes continue around cost-sharing that can exceed the pharmacy’s negotiated price. In Negron v. Cigna/OptumRx litigation, plaintiffs alleged schemes where insureds were charged more than the negotiated amounts and excess money was remitted back, described as “clawbacks.” (11) For self-funded employers, this is not just member pain. It can increase overall plan costs and trigger fiduciary litigation risk when participants claim the plan allowed unjustified pricing.

Opaque “pass-through” promises and hidden remuneration: “pass-through” is often marketed as “we pass rebates.” In reality, compensation can show up as many categories: manufacturer admin fees, data fees, pharmacy DIR-like fees/recoupments, spread on specific channels, price protection terms, rebate aggregation retained amounts, and affiliate payments. DOL’s Jan 2026 fact sheet explicitly calls out categories like spread compensation, pharmacy clawbacks, and price protection arrangements as reportable compensation categories, and proposes audit rights so fiduciaries can verify accuracy (12). The DOL proposal also notes concerns about rebate aggregators/GPOs formed outside the U.S. and the need to capture compensation flowing to “agents” that do not fit neat affiliate/subcontractor definitions (5).

A simple visual of where conflicts show up in a typical commercial flow is below. It matches the structure described in state Medicaid reporting and federal discussions, even though the exact contract terms vary widely.

Diagram 1: Where conflicts show up in a typical commercial flow

What the public record shows: quantified impacts, lawsuits, enforcement

The data problem for employers is that the strongest transparency is often found in government audits and enforcement, not in commercial PBM sales decks. Still, the public record has enough signal to justify hard questions in every RFP and renewal.