The Definition of Oversee: to watch over and direct (an undertaking, a group of workers, etc.) in order to ensure a satisfactory outcome or performance.

Pharmacy Benefit Managers (PBMs) often use clinical programs like Generic Dispensing Rate (GDR) and Specialty Dispensing Rate (SDR) to influence employer drug spend, but not always in your favor. In this episode of Unlocking the Secrets of PBMs: Strategies to Navigate Their Profit Tactics, I break down how these metrics can be quietly manipulated to boost PBM profit at the expense of plan sponsors.

[Watch} Unlocking the Secrets of PBMs: Strategies to Navigate Their Profit Tactics

You’ll learn:

What GDR and SDR actually measure

How PBMs use them to appear clinically focused while protecting revenue

Warning signs your PBM might be misusing these benchmarks

If you’re an HR leader, CFO, benefits consultant, or self-funded employer looking to cut pharmacy costs without sacrificing outcomes, this video is a must-watch.

As Rite Aid collapses, customers and other pharmacies bear the impact and other notes from around the interweb:

Get Certified Now!

As Rite Aid collapses, customers and other pharmacies bear the impact. Rite Aid has sold the pharmacy services of most of its stores across the United States to several rivals. The bankrupt company announced the fire sale Thursday, with CVS Pharmacy, Walgreens, Albertsons and Kroger scooping up Rite Aid’s pharmacy services at more than 1,000 locations. CVS Pharmacy was the biggest buyer, snapping up the prescription files of more than 600 Rite Aid stores spanning 15 states and agreeing to buy 64 Rite Aid locations in Idaho, Oregon, and Washington. The transactions still must be approved by the relevant bankruptcy court. As Rite Aid navigates the Chapter 11 bankruptcy process, the company said its stores remain open and customers can continue to use their pharmacy services “without interruption.”

Stuck in the Middle: Self-Funded Health Plans and Recent Challenges to State PBM Laws. In recent years, prescription drug prices have been top-of-mind for state legislators, who have responded by passing laws that seek to control that pricing in a variety of ways, including by regulating pharmacy benefit managers (PBMs). While states are permitted to regulate fully insured products offered in their state, including mandating the benefits that insurers must offer, the Employee Retirement Income Security Act of 1974, as amended (ERISA) preempts state laws that impermissibly relate to self-funded employer-sponsored health plans that are subject to ERISA.

The Uneven Landscape of Prescription Coverage and Restrictions Across U.S. Insurance. Medicaid, often viewed as a safety net, covers the broadest share of prescribed drugs but imposes more restrictions than any other insurance type. Medicare, by contrast, covers the least drugs while restricting access for nearly half of the drugs that are covered. Commercial insurance, typically employer-sponsored or purchased individually, falls in the middle in terms of drug coverage but has the fewest coverage limitations, like prior authorization, quantity limits, and step therapy.

Costs of Extending the Small Molecule Exemption Period in Medicare Drug Price Negotiation. The Inflation Reduction Act (IRA) of 2022 empowered Medicare to negotiate prices for certain prescription drugs with high levels of Medicare spending. However, prices for new drugs cannot be negotiated immediately after Food and Drug Administration approval due a statutory waiting period. For small molecule drugs (chemical compounds that are usually pills, e.g. empagliflozin [Jardiance]), prices are negotiated at year 7 and take effect 9 years after FDA approval. For biologics (derived from a living organism or its cells and that are usually injections, e.g. insulin), negotiation occurs starting after 11 years, and the negotiated prices take effect at year 13.

Why TransparentRx Is Your Trusted Partner for Smarter Pharmacy Benefits

At TransparentRx, we specialize in delivering fiduciary pharmacy benefit management services that prioritize transparency, cost containment, and optimal patient outcomes. Our unique approach helps self-funded employers, benefits consultants, and health plan sponsors navigate the complexities of pharmacy benefits while reducing costs and enhancing care.

If you’re ready to take control of your pharmacy benefit strategy and eliminate hidden fees, contact TransparentRx today for a consultation. Let us help you achieve smarter, more effective benefits management.

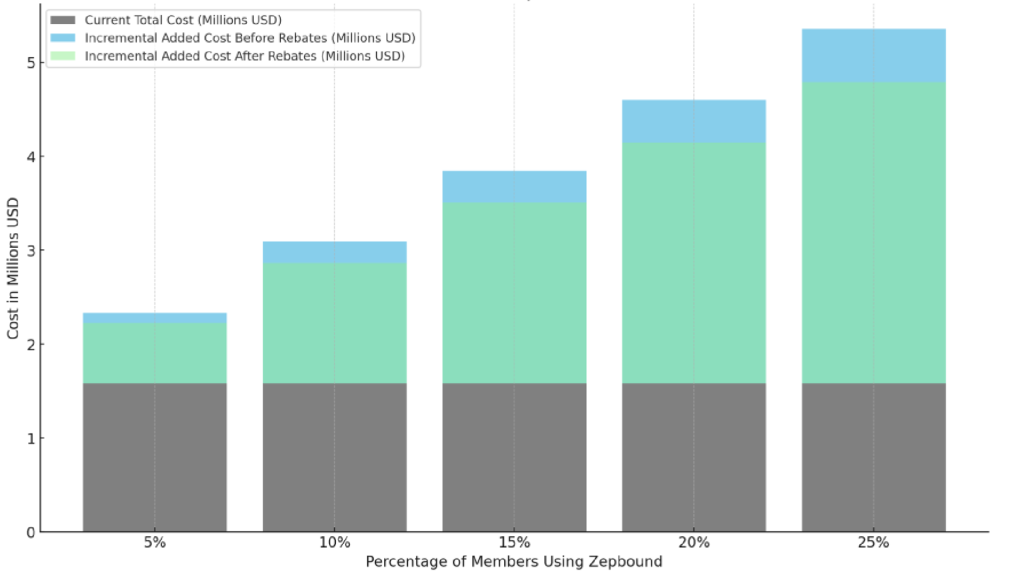

GLP-1 drugs like Wegovy and Zepbound have exploded in popularity for both weight loss and type 2 diabetes. They work, but they’re expensive, often exceeding $1,000 per member per month. Left unchecked, GLP-1 costs will crush your pharmacy spend and drive up health plan premiums, stop-loss rates, and employee contributions. Figure 1 models the budgetary impact of adding Zepbound to the formulary of a self-funded employer with 1224 members. Here’s how HR and Finance Leaders can take control of soaring GLP-1 drug costs.

1. Don’t Rely on PBMs to Manage the Problem

Many PBMs profit when your drug costs go up through spread pricing, rebate retention, and inflated dispensing fees. GLP-1s have become one of their biggest profit centers. If your PBM’s strategy to manage GLP-1s is vague or nonexistent, that is a problem.

Recommendation: Review your PBM contract. Make sure you have access to claims-level rebate data, no spreads, and full visibility into how GLP-1s are covered, reimbursed, and dispensed.

2. Establish Clear Clinical Criteria for Coverage

Approving GLP-1s for every employee who requests them is not financially sustainable. But denying coverage entirely can create backlash and retention issues.

Recommendation: Require prior authorization based on:

Confirmed diagnosis of type 2 diabetes or BMI ≥30 (or ≥27 with comorbidities)

Failure of first line therapy (i.e. Metformin) with diagnosis of type 2 diabetes

Documented history of lifestyle intervention

Quarterly clinical review to assess improvement (weight loss or A1C)

Discontinuation if there is no measurable improvement after 6 months

3. Move GLP-1s to the Pharmacy Benefit

Many GLP-1s administered in a clinical setting are billed under the medical benefit, where visibility and control are limited. Rebate capture is also more difficult.

Recommendation: Shift GLP-1 claims from the medical to the pharmacy benefit when possible. This improves formulary control, rebate access, and member-level tracking.

Figure 1: Total Cost vs. Added Cost (Pre- and Post-Rebate for Zepbound)

4. Use Tiered Coverage and a Narrow Formulary

Covering every GLP-1 is a waste of dollars. Employers need to focus coverage on the most effective and cost-efficient options.

Recommendation: Work with a fiduciary PBM to build a narrow GLP-1 formulary. Cover one or two preferred options. Require step therapy or exclude others entirely.

5. Explore Alternative Procurement Channels

Some employers are saving thousands per script by sourcing GLP-1s from international mail-order providers.

Recommendation: Evaluate alternate sourcing strategies, especially for weight-loss-only use. Savings can range from 40 to 60 percent per fill.

6. Tie Coverage to Lifestyle Support Programs

Drugs alone won’t solve obesity. Employers should require members to participate in lifestyle or obesity coaching programs as part of their GLP-1 coverage.

Recommendation: Bundle GLP-1 coverage with a medication therapy management (MTM), digital or onsite wellness program. Require active participation for continued access.

Bottom Line

GLP-1s deliver clinical value, but they can quickly become a budget buster if left unmanaged. Self-funded employers cannot afford to be passive. With the right guardrails, procurement strategy, and clinical oversight, you can offer meaningful access while keeping spend in check. If you’re ready to tackle your GLP-1 costs head-on, let’s connect.

Elevate your expertise in pharmacy benefits management with the Certified Pharmacy Benefits Specialist® (CPBS) program, sponsored by the UNC-Chapel Hill Eshelman School of Pharmacy. Whether you’re an HR leader, finance executive, consultant, or pharmacist, this certification provides the in-depth knowledge and strategic insight needed to manage pharmacy benefits with confidence and cost efficiency. Gain up to twenty continuing education credits, enhance your career prospects, and help your organization take control of pharmacy spend. Register today to join a growing network of professionals shaping the future of pharmacy benefits management. Learn more at the Pharmacy Benefit Institute of America.

Plan Sponsors Can Choose Who They Trust with Their Pharmacy Benefits

“If you don’t know how your PBM gets paid, you’re probably overpaying.” That’s not scare tactics, it’s a fiduciary truth. For CFOs, CHROs, benefits consultants, and self-funded employers, understanding how a pharmacy benefit manager (PBM) earns revenue is the difference between managing costs and subsidizing someone else’s margin.

PBM Profits Often Come From Plan Overspending

Most PBMs profit through spread pricing and other opaque tactics. They earn revenue from the gap between what your plan pays and what the pharmacy receives, along with a mix of back-end cash flows like rebates, DIR fees, and clawbacks. These streams are often subsidized by inefficient benefit design and weak clinical oversight. The issue? These profits are usually hidden, buried in complex financial models and disguised as standard industry practice.

Here’s how you should be modeling PBM earnings:

Earnings After Cash Disbursement Formula

EACD = AF + DF + IC + MR – CD

Where:

MR = Manufacturer Revenue

IC = Ingredient Cost Reimbursement

DF = Dispensing Fees *(includes traditional dispensing fees and DIR fees)

AF = Administrative Fees

CD = Cash Disbursement to pharmacies and rebate payouts to plan sponsors

Note: In this formula, DF (Dispensing Fees) is a composite of:

Dispensing Fees paid or retained

DIR Fees (Direct and Indirect Remuneration) collected from pharmacies

DIR and DF Are Your Plan’s Money

When PBMs withhold or clawback fees from pharmacies (whether labeled as DIR, performance penalties, or admin charges) they’re using your plan’s volume and activity to generate income. If these funds aren’t transparently passed back or accounted for, they become undisclosed profit. In fiduciary terms, that’s plan leakage.

Why PBM Earnings Matter

If your PBM’s compensation is opaque, you’re at risk for:

Overpaying for drugs, even when rates look competitive

Losing plan assets to undisclosed spread, clawbacks, or retained fees

Incentive misalignment that drives up utilization or keeps higher-cost drugs on formulary

In contrast, when a PBM provides clear, formula-based earnings disclosures, you can:

Benchmark fees against fiduciary standards

Demand rebate and DIR transparency

Eliminate conflicts of interest

Fiduciary Oversight Starts with Financial Clarity

If your PBM resists disclosing their earnings using a formula like the one above, that’s a red flag. You can’t control what you can’t see, and in pharmacy benefits, visibility is leverage. Bottom line, you’re not just managing a benefit, you’re managing a financial asset. Know how your PBM earns their money, and you’ll protect more of yours.

Elevate your expertise in pharmacy benefits management with the Certified Pharmacy Benefits Specialist® (CPBS) program, sponsored by the UNC-Chapel Hill Eshelman School of Pharmacy. Whether you’re an HR leader, finance executive, consultant, or pharmacist, this certification provides the in-depth knowledge and strategic insight needed to manage pharmacy benefits with confidence and cost efficiency. Gain up to twenty continuing education credits, enhance your career prospects, and help your organization take control of pharmacy spend. Register today to join a growing network of professionals shaping the future of pharmacy benefits management. Learn more at the Pharmacy Benefit Institute of America.

Self-Funded Health Plans and Recent Challenges to State PBM Laws and other notes from around the interweb:

Get Certified Now!

Stuck in the Middle: Self-Funded Health Plans and Recent Challenges to State PBM Laws. In recent years, prescription drug prices have been top-of-mind for state legislators, who have responded by passing laws that seek to control that pricing in a variety of ways, including by regulating pharmacy benefit managers (PBMs). While states are permitted to regulate fully insured products offered in their state, including mandating the benefits that insurers must offer, the Employee Retirement Income Security Act of 1974, as amended (ERISA) preempts state laws that impermissibly relate to self-funded employer-sponsored health plans that are subject to ERISA.

The Uneven Landscape of Prescription Coverage and Restrictions Across U.S. Insurance. Medicaid, often viewed as a safety net, covers the broadest share of prescribed drugs but imposes more restrictions than any other insurance type. Medicare, by contrast, covers the least drugs while restricting access for nearly half of the drugs that are covered. Commercial insurance, typically employer-sponsored or purchased individually, falls in the middle in terms of drug coverage but has the fewest coverage limitations, like prior authorization, quantity limits, and step therapy.

Nonadherence Remains Common Concern in Dermatology. Concerns of low adherence for dermatological therapies persist, translating to poor patient outcomes, ineffective treatment, and decreased quality of life (QOL), according to a study published in Cureus.1 Researchers believe this low adherence can be owed to the sheer variety of treatment options available for a number of prominent dermatological conditions. According to the CDC, medication nonadherence is the act of a patient not taking their prescribed medicine or not following their providers’ instructions properly. While many factors can contribute to nonadherence, as well as barriers that impede patients’ ability to be adherent, it is known to result in uncontrolled blood pressure and greater rates of hospital admissions.

Payers split on GLP-1 strategy. Insurers are employing different strategies to manage the high cost of GLP-1 drugs. Most GLP-1 drugs are approved to treat type 2 diabetes. Wegovy and Zepbound are approved for weight loss. The drugs often cost more than $1,000 a month. Multiple insurers have cited the high price of GLP-1 drugs as a contributing factor to financial losses in 2024. Some insurers have chosen to drop coverage of the drugs for weight loss altogether.

Why TransparentRx Is Your Trusted Partner for Smarter Pharmacy Benefits

At TransparentRx, we specialize in delivering fiduciary pharmacy benefit management services that prioritize transparency, cost containment, and optimal patient outcomes. Our unique approach helps self-funded employers, benefits consultants, and health plan sponsors navigate the complexities of pharmacy benefits while reducing costs and enhancing care.

If you’re ready to take control of your pharmacy benefit strategy and eliminate hidden fees, contact TransparentRx today for a consultation. Let us help you achieve smarter, more effective benefits management.

Pharmacy Benefit Managers (PBMs) were originally designed to help employers manage rising drug costs. Today, many have built business models that put profits ahead of patient care, creating pricing games, blocking independent pharmacies, and driving up plan costs.

Arkansas is putting a stop to that. HB 1150, a new law set to take effect in 2026, will prohibit PBMs that own pharmacies from operating them in the state. The goal is simple: eliminate conflicts of interest and protect patient access to affordable care.

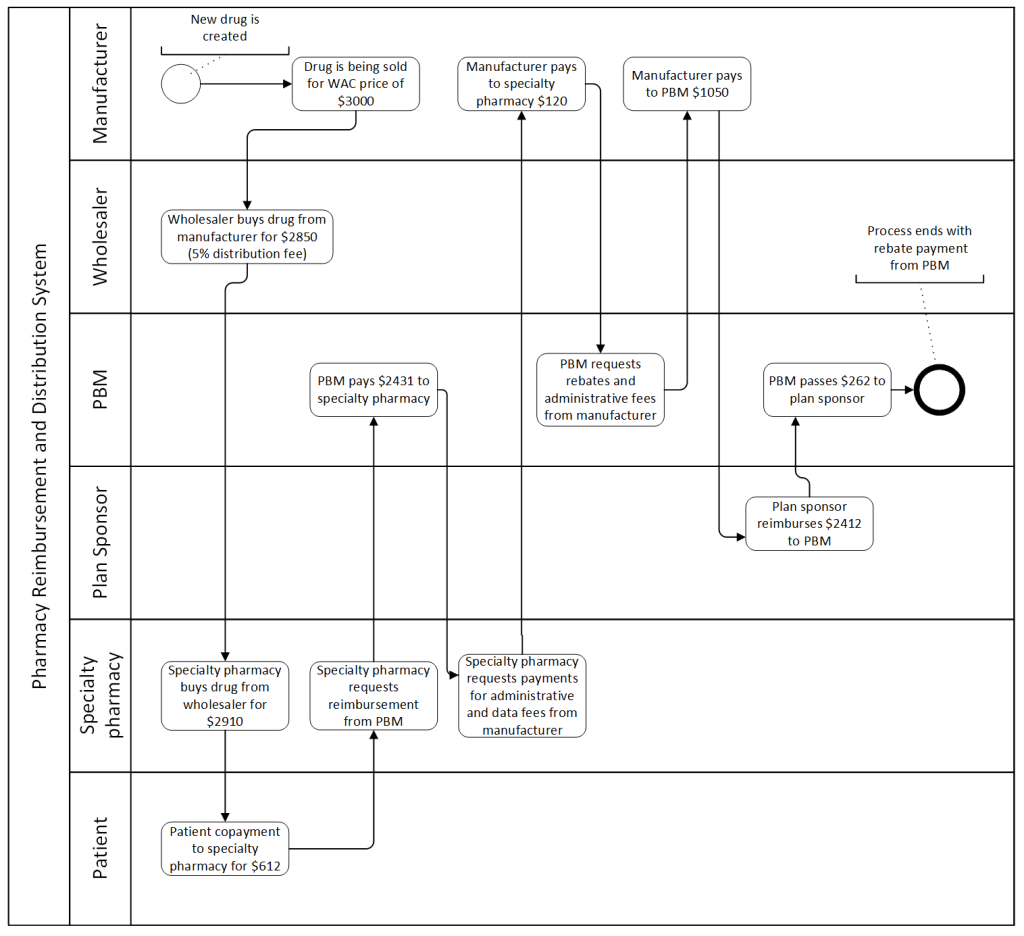

Where the Specialty Drug Dollar Really Goes

Employers, especially those with Arkansas-based members, should prepare by:

Choosing PBMs without ownership ties to licensed pharmacies in the state.

Working with current PBMs to ensure pharmacy networks include non-affiliated providers.

Planning for pharmacy closures, especially in areas where access may already be limited.

Because HB 1150 regulates pharmacy licensing, not benefit design, employers with self-funded ERISA plans likely won’t be exempt.

Other states and even Congress are watching Arkansas closely. Change is coming, and employers that demand a true fiduciary standard from their PBM partners will be better positioned to control costs and protect their members.

At TransparentRx, we help employers eliminate hidden conflicts and ensure pharmacy benefits are managed with complete transparency and care. If your PBM isn’t aligned with your best interests, let’s talk.

Executive Action Aims to Slash Drug Prices and Enhance PBM Clarity and other notes from around the interweb:

Get Certified Now!

Executive Action Aims to Slash Drug Prices and Enhance PBM Clarity. The Employer Retirement Income Security Act (ERISA) mandates strict standards for fiduciaries managing employee benefit plans, requiring careful selection, and monitoring of third-party providers like PBMs. Recently, the PBM industry faces increased scrutiny over drug costs, transparency issues, and lawsuits alleging mismanagement of prescription benefits. On April 15, 2025, President Donald Trump issued an executive order (EO) to reduce prescription drug prices in the U.S. This order instructs the Department of Labor (DOL) to enhance transparency in employer health plans regarding compensation from pharmacy benefit managers (PBM). While these changes will take time to implement, immediate cost reductions are not expected.

The Rise in Direct-to-Consumer Advertising of Prescription Drugs. From the marketing of drugs with low-added benefit to manufacturers’ inability to follow FDA guidelines, direct-to-consumer advertising for prescription drugs has increased in the US and is beginning to raise alarms. “Under FDA guidelines, pharmaceutical companies are supposed to provide a balanced view of drugs in advertising in terms of their risks and benefits,” said Jenny Markell, BA, PhD Candidate of Health and Public Policy at the Johns Hopkins Bloomberg School of Public Health. “They’re supposed to avoid any misleading information. It’s illegal, for example, to overstate a drug’s benefits, misrepresent data from studies, or make claims that are not supported by adequate evidence.” However, even after FDA attempts of holding manufacturers accountable, drug companies continue to skew the country’s perceptions of specific prescription drugs.

PBMs Score a Win in Federal Court Against State Regulation. A recent federal court decision has the potential to tip the balance in an ongoing series of skirmishes over state regulation of pharmacy benefit managers (PBMs). In McKee Foods Corp. v. BFP Inc. d/b/a/ Thrifty Med Plus Pharmacy, the US District Court for the Eastern District of Tennessee declared that an “any willing pharmacy” requirement in Tennessee was preempted by the federal Employee Retirement Income Security Act of 1974 (ERISA), as amended. On one side, self-funded group health plans argue that ERISA allows them to comply with a single set of rules nationwide, rather than having to navigate a patchwork of different, overlapping, and sometimes conflicting state laws.

Arkansas governor signs legislation banning PBMs from simultaneously owning pharmacies. Arkansas lawmakers in the Senate on Wednesday passed a bill that would stop pharmacy benefit managers (PBMs) from owning pharmacies and selling drugs retail in the state. The bill now heads to the governor’s desk for her signature. PBMs are the middlemen who negotiate with insurance companies, manufacturers, and pharmacies to set drug prices. Where the controversy comes in is when PBMs also own their own pharmacies, creating what many believe is a conflict of interest. CVS officials said a new law restricting Pharmacy Benefit Managers from owning pharmacies will result in the closure of more than 20 Arkansas pharmacies.

Why TransparentRx Is Your Trusted Partner for Smarter Pharmacy Benefits

At TransparentRx, we specialize in delivering fiduciary pharmacy benefit management services that prioritize transparency, cost containment, and optimal patient outcomes. Our unique approach helps self-funded employers, benefits consultants, and health plan sponsors navigate the complexities of pharmacy benefits while reducing costs and enhancing care.

If you’re ready to take control of your pharmacy benefit strategy and eliminate hidden fees, contact TransparentRx today for a consultation. Let us help you achieve smarter, more effective benefits management.

Non-fiduciary PBMs negotiate with drugmakers and pharmacies to benefit themselves. They use the purchasing power of plan sponsors who lack full insight into pharmacy economics. What used to be a cost-efficiency business is now, in many cases, about promoting the most profitable products, not the most clinically appropriate ones. If you’re a smart buyer of PBM services, you want more control over your pharmacy benefit plan, not less. Here are six pillars of a high-performing pharmacy benefit plan design to help you build a plan that works in your favor.

1. Internal Expertise

Internal expertise means a buyer or consultant has the knowledge to independently evaluate PBM contracts, pricing, and performance without relying on the PBM for direction. It includes deep knowledge of formularies, rebate structures, MAC pricing, and plan design strategies, for instance. Before partnering with a PBM or consultant, it’s worth asking a few key questions as a team:

Do we have the pharmacy benefits expertise we need in-house?

If not, would targeted education or outside support add value?

Are the consultants we’re relying on certified in pharmacy benefit management?

As a Benefits Director, you don’t need to be a pharmacist, but you do need a strong understanding of how pharmacy benefits impact your plan’s performance. Relying too heavily on a PBM or consultant without the right checks can expose your organization to unnecessary risk. That’s where Certified Pharmacy Benefits Specialists (CPBS) come in. Having credentialed support on your side gives you the clarity and leverage to keep your plan aligned with your goals, not someone else’s bottom line.

2. Access

The formulary is your plan’s rulebook for drug access. It informs which medications are covered, at what cost to members, and under what conditions, guiding both prescribers and patients toward clinically appropriate and cost-effective choices.

You should review formulary design regularly, especially for high-cost drug classes like GLP-1sused for weight loss. These drugs now exceed $1,000 per member per month. While effective, ICER has stated their prices are not justified by the long-term benefit in obesity treatment alone.

PBMs may promote these drugs heavily due to large rebates. That’s not fiduciary. Make decisions based on outcomes and cost-effectiveness, not marketing hype or rebate flow. When managed by a fiduciary PBM, the formulary is designed to serve the plan sponsor’s best interest, not the PBM’s bottom line.

3. Medication Adherence

Medication adherence refers to the extent to which a patient takes their medications as prescribed by their healthcare provider. This includes the correct dose, timing, frequency, and duration of use. Non-adherence drives over $290 billion in avoidable healthcare costs each year. Even the best-designed plan fails if members don’t take their medications.

Use Proportion of Days Covered (PDC) to track adherence. A PDC of 80 percent or higher signals a member is staying on therapy. Monitor this at the plan level and intervene where necessary. Otherwise, avoidable ER visits and hospitalizations will drive up your total spend.

4. Cost Containment

Cost containment in pharmacy benefits management refers to a range of strategies, policies, and practices used to manage and reduce the total spend on prescription drugs without compromising the quality of care or patient outcomes. It’s a foundational goal for any fiduciary PBM and a critical metric for evaluating pharmacy benefit performance. Common cost controls in pharmacy benefits management include:

Mandatory generics

Therapeutic substitution

Quantity limits and step therapy

Specialty pharmacy carve-outs

But controls without measurement are worthless. Use Total Cost of Care (TCOC) to see if lower pharmacy spend is driving higher medical costs. And track Per Member Per Month (PMPM) pharmacy trend to keep your budget on track. These are your two gold-standard benchmarks. If your PBM isn’t talking about them, ask why.

5. Member Cost Share

Cost-sharing strategies like copays and coinsurance are standard, but some tactics do more harm than good. Copay accumulator programs block manufacturer copay assistance from applying to members’ deductibles. That means patients pay more out of pocket, often unexpectedly.

PBMs pocket the assistance and bill your plan anyway. Members struggle to afford meds, adherence drops, and total costs go up. These programs benefit PBMs, not your plan or your people.

6. Outcomes and Safety

Your plan should limit or exclude drugs that provide little to no health benefit. This includes:

Hair growth and weight loss products

ED drugs

Growth hormones

Over-the-counter meds

Opioids

The opioid crisis is a case study in misaligned incentives. From 2016 to 2017, Purdue Pharma paid $400 million in rebates and fees to the big three PBMs. Internal documents showed Purdue understood rebates were the key to staying on formulary. And it worked. Self-funded employers paid for it, both financially and in lost lives. Be explicit about what your plan won’t cover. Do not let your PBM make those decisions in a vacuum.

Final Word: Own Your Education

The best protection against misaligned incentives is knowledge. When you understand how pharmacy benefits really work, you’re in a stronger position to lead, question, and negotiate.

Too often, plan sponsors hand over control to PBMs or advisers without fully understanding the mechanics behind pricing, rebates, and utilization. That gap is where unnecessary costs and missed opportunities live.

Invest in your own education and that of your team. Learn the language. Get certified. Ask sharper questions. When you understand the system, you don’t just manage a benefit, you lead it. Transparency, accountability, and aligned incentives all start with being informed.

Governor signs legislation banning PBMs from simultaneously owning pharmacies and other notes from around the interweb:

Get Certified Now!

Arkansas governor signs legislation banning PBMs from simultaneously owning pharmacies. Arkansas lawmakers in the Senate on Wednesday passed a bill that would stop pharmacy benefit managers (PBMs) from owning pharmacies and selling drugs retail in the state. The bill now heads to the governor’s desk for her signature. PBMs are the middlemen who negotiate with insurance companies, manufacturers, and pharmacies to set drug prices. Where the controversy comes in is when PBMs also own their own pharmacies, creating what many believe is a conflict of interest. CVS officials said a new law restricting Pharmacy Benefit Managers from owning pharmacies will result in the closure of more than 20 Arkansas pharmacies.

Overcoming Biosimilar Utilization Barriers. “The opportunities with all of these biosimilars are that they have the ability to improve patient access, new starts, persistence and adherence,” said panelist Alex Mersch, PharmD, an assistant director of ambulatory specialty programs at University of Iowa Health Care, in Iowa City. “For many organizations, especially if we look at it from the inpatient side, there’s a lot of opportunity to decrease drug costs by [replacing the reference product with] the biosimilar.”

The Rise in Direct-to-Consumer Advertising of Prescription Drugs. From the marketing of drugs with low-added benefit to manufacturers’ inability to follow FDA guidelines, direct-to-consumer advertising for prescription drugs has increased in the US and is beginning to raise alarms. “Under FDA guidelines, pharmaceutical companies are supposed to provide a balanced view of drugs in advertising in terms of their risks and benefits,” said Jenny Markell, BA, PhD Candidate of Health and Public Policy at the Johns Hopkins Bloomberg School of Public Health. “They’re supposed to avoid any misleading information. It’s illegal, for example, to overstate a drug’s benefits, misrepresent data from studies, or make claims that are not supported by adequate evidence.” However, even after FDA attempts of holding manufacturers accountable, drug companies continue to skew the country’s perceptions of specific prescription drugs.

ERISA Preemption: Impact on State PBM Laws. Pharmacy benefit managers (PBMs) play a role in the US healthcare system by negotiating drug prices and formulary placements on behalf of insurers and employer sponsored health plans. Recently, there have been concerns about certain PBM business practices, including drug pricing transparency and reimbursement rates. This has prompted numerous states to enact laws regulating PBMs. A key legal challenge to these state laws is whether ERISA preempts these laws. ERISA is a federal law that sets national standards for employer-sponsored health plans. One of its most important provisions is preemption, meaning that ERISA overrides state laws that attempt to regulate employer health plans directly.

Why TransparentRx Is Your Trusted Partner for Smarter Pharmacy Benefits

At TransparentRx, we specialize in delivering fiduciary pharmacy benefit management services that prioritize transparency, cost containment, and optimal patient outcomes. Our unique approach helps self-funded employers, benefits consultants, and health plan sponsors navigate the complexities of pharmacy benefits while reducing costs and enhancing care.

If you’re ready to take control of your pharmacy benefit strategy and eliminate hidden fees, contact TransparentRx today for a consultation. Let us help you achieve smarter, more effective benefits management.

Not all red flags in PBM contract clauses are obvious. Some are buried in plain sight, phrased to sound harmless, even routine. But make no mistake, these clauses are often where profit hides, and where plan sponsors lose control. Here are five such clauses that deserve your full attention.

1. “Brand Effective Rate” Guarantees

On the surface, a Brand Effective Rate (BER) seems like a safeguard—a guarantee you’ll get a certain discount off AWP for brand drugs. But here’s the trap: PBMs typically define “brand” based on their internal classification, not by FDA or Medispan standards. That means drugs commonly accepted as generics may be counted as brands in your pricing guarantees. This manipulation boosts the PBM’s spread revenue and inflates your actual drug spend—all while appearing to honor the BER.

Example clause:“PBM guarantees a Brand Effective Rate discount of 18% off AWP for brand drugs as determined by PBM’s internal classification system.”

Fix:Demand clarity. The contract should reference a third-party source like Medispan for how “brand” and “generic” drugs are defined, not leave it up to the PBM.

2. “Custom Rebate” or “Non-Standard Rebate” Language

Some contracts give PBMs the ability to retain rebates that fall outside the traditional formulary or performance structures. These might be labeled as “custom,” “specialty,” or “administrative” rebates. These aren’t small dollars. They’re just hidden from view.

Example clause:“PBM will remit 100% of formulary rebates. PBM retains administrative, data, and market share incentives associated with manufacturer contracts.”

Fix: Require full transparency and 100% pass-through on all rebates—no matter what label they carry. Avoid vague classifications.

3. “Market Check” Clauses Without Enforcement

A contract might include a market check clause, promising to benchmark pricing mid-contract. But if there’s no mechanism to enforce it—or worse, the PBM controls the data source—it’s window dressing.

Example clause:“PBM agrees to conduct a market check upon client request in the second contract year. PBM will assess market competitiveness and make adjustments where appropriate.”

Fix: Ensure market checks are tied to independently verifiable data sources and come with actionable pricing adjustments. If it’s not enforceable, it’s useless.

4. “Sole Discretion” Language for Formulary or MAC Lists

Clauses that give the PBM “sole discretion” to update the formulary or MAC pricing are dangerous. It gives them unilateral control over which drugs are covered and at what price—without accountability.

Example clause:“PBM may, at its sole discretion and without prior approval, modify the formulary or MAC pricing schedule to reflect current market conditions.”

Fix: Retain audit rights and require notification and approval for key formulary or MAC list changes. At a minimum, add a right to exit if the PBM acts against your financial interests.

5. “Audits Must Be Conducted by a Qualified Third Party”

This one sounds reasonable—until you try to conduct an audit. PBMs often define “qualified” in a way that disqualifies anyone who might dig too deep or ask the right questions.

Example clause:“Client may audit PBM once per contract year using a nationally recognized auditor approved by PBM.”

Fix: Retain the right to use an auditor of your choice, as long as they meet reasonable privacy and security standards. Don’t give the fox a say in which watchdog gets hired.

PBMs are skilled at writing contracts that preserve their margin while appearing compliant. That’s why it’s not enough to just review your contract—you have to decode it.

AtTransparentRx, we operate under a fiduciary standard of care. That means no hidden clauses, no retained rebates, and no conflicts of interest. If you want a second set of eyes on your PBM agreement—or you’re tired of feeling like you’re being out-negotiated—let’s talk.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.