Kaleo fires back at Express Scripts, claiming it’s owed at least $5.3M

After Express Scripts last month filed a suit alleging Kaleo owes $14.5 million in unpaid rebates, Kaleo has filed a countersuit saying it overpaid the PBM giant by $5.3 million.

Kaleo’s suit claims it overpaid due to “opaque and convoluted invoices” from Express Scripts.

|

| Click to Learn More |

Further, Kaleo says, it paid administrative fees to the PBM giant only to see patient access to its overdose med Evzio restricted. Both actions amount to violations of contractual obligations, the drugmaker argues.

In its filing, Kaleo takes a page out of the industry playbook to accuse PBMs of causing high prices by demanding rebates that pad their bottom lines. In the suit, Kaleo argues Express Scripts “extracts excessive fees and ‘rebates’ from pharmaceutical manufacturers like Kaleo to drive up its own profits while providing little, if anything, of value to the pharmaceutical supply chain.”

For its part, Express Scripts argued in its lawsuit that Kaléo owes $14.5 million in unpaid rebates because the company stopped paying its bills in full back in April 2016. From June 2016, the company hasn’t paid any rebates, and Express Scripts removed Evzio from its national preferred formulary effective July 1, 2016, according to the Express Scripts lawsuit.

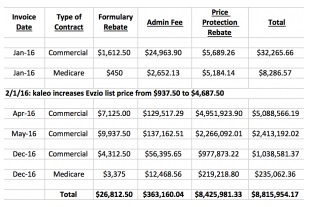

Kaleo’s coverage contract with Express Scripts features two types of rebates, according to Express Scripts’ suit, a “formulary rebate” designed to secure coverage and a “price protection rebate” to limit exposure to dramatic price hikes. Kaleo’s eventual price hikes on Evzio drove up the latter significantly.

On Friday, an Express Scripts spokesperson said the PBM wants “Kaleo to honor its written contracts and not shirk its obligation to pay the rebates and fees it owes.”

“Kaleo’s business strategies—its baseless exponential price increases on its drugs and its failure to satisfy its contractual obligations to Express Scripts under the terms of its rebate agreements—are geared towards increasing its own profits and undermining the efforts by pharmacy benefit managers and other payers to reduce the cost of prescription drugs,” according to the Express Scripts spokesperson.

Kaleo CEO Spencer Williamson sees things differently, arguing that the lawsuit from Express Scripts is “baseless.”

Earlier this year, more than 30 senators wrote to Kaleo seeking information about drastic price hikes on the lifesaving overdose med. In its countersuit, Kaleo admits that it priced a two-pack of Evzio injectors at $575 in 2014 and $3,750 in 2016.

The senators wrote to Kaleo CEO Spencer Williamson that they were “deeply concerned” about the price hikes that came amid an opioid-abuse epidemic. The move “threatens to price-out families and communities that depend on naloxone to save lives,” the letter stated (PDF).