Employers’ New Decision Point: Whether to Cover Expensive Weight Loss Drugs [Weekly Roundup]

Employers’ New Decision Point: Whether to Cover Expensive Weight Loss Drugs and other notes from around the interweb:

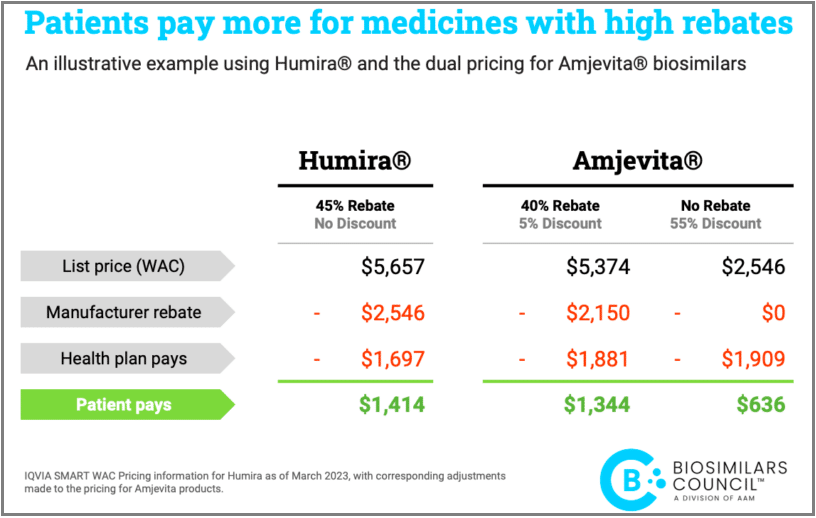

- When is a Smaller AWP Discount Better? Buyers need to be able to select a cheaper product if one is available on the market to save money. It’s common sense. The pharmaceutical business, however, is not your typical market. Many people are prevented from using cheaper biosimilars and forced to pay exorbitant prices for brand name medications because of perverse incentives. Health plans and PBMs now benefit from brand manufacturer price reductions, such as rebates, in return for securing preferred positioning on formularies and excluding cheaper biosimilars from those formularies. The modest uptake of less expensive biosimilar insulin serves as a stark illustration of these processes. As evidenced by statistics from IQVIA, several health plans have continued to favor and promote the use of an expensive brand insulin.

- The Consolidated Appropriations Act and PBM Transparency. Pharmacy Benefit Managers (PBMs) have been extending vertical integration in new and unique ways, leading to significant issues for plan sponsors and plans (referred to as “Plans” collectively). In a new and innovative approach, several large PBMs have created an additional layer between themselves and manufacturers to effectively delegate the collection of manufacturer rebates to “rebate aggregators.” Sometimes referred to as rebate GPOs, these mysterious entities include Ascent Health Services, a Switzerland-based GPO that Express Scripts launched in 2019; Zinc, a contracting entity launched by CVS Health in 2020, and Emisar Pharma Services, an Ireland-based entity recently rolled out by OptumRx. Even some of the major PBMs (i.e., the “Big Three” PBMs) sometimes contract with other PBMs’ rebate aggregators for the collection of manufacturer rebates as seen in the case of OptumRx contracting with Express Scripts for rebate aggregation for public employee plans. Worse yet, several of these entities have claimed exemption from the federal GPO Safe Harbor, resulting in a lack of transparency, and few limitations of their profitability.

- Employers’ New Decision Point: Whether to Cover Expensive Weight Loss Drugs. Thanks to buzzy results and popularity among celebrities, there’s a big spike in demand for GLP-1 drugs, such as Ozempic and Wegovy, as a tool to help people shed pounds. The injectable medications, originally prescribed for diabetes management, have also shown promising results for weight loss. That demand is creating a major decision point for employers: whether their health insurance plans should cover the pricy drugs for weight loss. “It’s a really big issue for employers,” said Dr. Jeff Levin-Scherz, M.D., population health leader at consulting firm WTW. “We’re seeing a pretty dramatic increase in the rate of the prescription of [drugs such as] Ozempic, which is only approved for diabetes but is now showing to be very effective for weight loss.” As a result, employers are thinking about how to handle coverage of the drugs, industry experts say, a decision made more difficult by competing priorities of trying to hold down rising health care costs for themselves while also retaining and wooing talent in an employee-driven job market. Covering desirable drugs for weight loss could help them with the latter.

- Report: “Specialty” Drugs are by Far the Most Expensive, but Classification Seems Arbitrary. The prescriptions with the most astonishing price tags — like cancer meds that can cost more than $20,000 a month — are usually classified as “specialty” drugs. You’d think that since they’re so costly, there would be clear criteria for putting drugs in the specialty category. But, according to a new report, you’d be wrong. The issue might seem arcane, but it’s hugely important. Specialty drugs account for only about 2% of the volume of drugs dispensed in the United States, according to industry estimates, but they also account for more than 50% of overall drug spending. The report, by data analysis firm 46Brooklyn Research, found that the three largest drug middlemen in the United States often don’t classify the same medicines as specialty. It also said that a substantial portion of the ones they do put into that category are generics — drugs that are usually no longer under patent and thus are supposed to be cheaper because multiple drugmakers can supply them.