Biologic or specialty drugs cost, on average, 10 times more than a small molecule or non-biologic prescription drug. At an average monthly cost of $3,000 and change, it’s only expected to get more expensive for plan sponsors. In fact, CVS Caremark estimates that specialty drugs could account for about half of the total pharmacy spend in 2018, which is up from one-third just two years earlier!

These recommendations are for plan sponsors who take their pharmacy benefits seriously; meaning they don’t rely too much on the advice of advisers or PBM account managers and are active participants in the management of the pharmacy benefit plan throughout the year.

Because these recommendations cut into your PBM’s bank account, you will get all sorts of push back why they don’t or can’t work. Cut through the noise and do your own due diligence by learning the business. You will see I’m writing this for your benefit not mine. Here are six techniques to blunt specialty drug costs and what has become the single largest driver of pharmacy cost trend.

A carved-out program may provide better cost control, transparency and technology as well as information and reporting. Health insurers may bundle the two programs and subsidize some of the pricing from one service with that of another (cost-shifting). For companies with a carved in program, there may be concerns about changing to a carved out program due to a perception that additional time and resources will be needed, but I have seen that on a day to day basis, there is little difference in having a separate specialty pharmacy program. The functions are the same and among the advantages are the following:

There are significant advantages to pursuing a carve-out strategy, both for the plan sponsor and plan participants.

That’s right I said it! Bring manufacturer contracting and rebate management in-house. The time has come and gone to only be talking about rebates or more specifically formulary rebates. On May 16, 2017 Express Scripts filed a complaint against drugmaker kaleo. The complaint revolves around the opioid overdose treatment, Evzio, which kaleo manufactures. Express Scripts’ attorneys redacted the complaint, but did not redact some information that Express Scripts has long regarded as proprietary thus not typically made available to the public.

According to Express Scripts, it entered into rebate agreements with kaleo for Evzio that required kaleo to pay Express Scripts not just for rebates but also administrative fees. The complaint reveals that in four of its invoices to kaleo, Express Scripts billed kaleo $26,812 in total for “formulary rebates” and $363,160 in total for “administrative fees.” That’s right, administrative fees amounted to almost 15 times more than the formulary rebates!

While plan sponsors believe they retain as much as 95% of rebate dollars (non-fiduciary PBM theoretically retains only the 5% difference), the truth is plan sponsors are retaining far less than 50% of rebates or earned manufacturer revenue. Don’t believe what so called transparent or pass-through PBMs tell you about how they make money – almost all of them are lying to you plain and simple.

How do you know if a PBM is offering radical transparency? The contract will tell you so that’s how. Of course, it requires a trained eye (someone entrenched in the business of pharmacy benefits management) to interpret it on your behalf. Not even an attorney from the top of his or her class can help in this regard if they don’t know the business of pharmacy benefits management.

The point is to address all manufacturer revenue paid to the PBM not just formulary rebates. If your PBM is unwilling to provide access to manufacturer contracts or explanation of payments, then as a plan sponsor you should be exploring a carve-out option or aligning with a fiduciary PBM. To do nothing and accept little or no transparency is a losing proposition.

3) Partial-Fill Program(1)

Some say that a partial fill is really a reduction-of-waste program, while others have pointed out the potential for impact on quality of care. A third group sees a partial fill as a medication-support and education tool. The reality is that depending on the services that surround the partial-fill plan design, it can be any or all 3. The best of the partial-fill programs have aspects that include:

- Clinical evaluation of potential side effects and efficacy prior to completing the secondary-portion fill of the medication.

- Ensuring that a patient still needs the medication. This may include issues such as admission to an inpatient facility in the interim or a change in circumstances, such as diagnostics, clinical goals, or death.

- Addressing medication adherence issues associated with the medication.

- Reviewing additional clinical information regarding a patient’s condition or the medication.

- A complete medication reconciliation to identify potential complications or issues associated with drug-drug interactions.

- Communicating with the prescribing physician if he or she is not the evaluating clinician.

- Helping to identify alternative treatments if there are clinical (side effect or efficacy) issues with the initial medication.

There is one area of concern associated with partial fill that has been identified and that is when there is little or no clinical interaction between the partial fill and the completion of the fill. The partial-fill model can reduce unnecessary fill completion and, therefore, reduce costs; however, this misses an opportunity to potentially improve clinical outcomes, and support patients regarding medical conditions that often need significant clinical support.

Source (1): http://www.ajpb.com/journals/ajpb/2016/ajpb_julyaugust2016/partialfill-programs–good-practice-or-barrier-to-care

4) Contracts

RFP burnout is something I attribute to what happens from the time a PBM request for proposal (RFP) begins and the countersigning of the resulting pharmacy services agreement concludes. RFPs can be quite lengthy and the selection process doubly so. By the time the selection committee or consultant evaluates the contract, they’re so exhausted and ready for the process to be over they don’t realize [or care] that much of what they were told or read doesn’t hold up in the contract language. It is at this point an expert in PBM contracts comes in handy and is worth their weight in gold. Forget what you’ve been told if the PBM doesn’t offer one of two business models; radical transparency or fiduciary standard it is hiding cash flows from you. These hidden cash flows lead to overpayments in your specialty drug cost. Period.

5) Outsource Prior Authorization

I’ve been fortunate enough to be a “fly on the wall” listening to the leadership teams of several national specialty pharmacies. And while they preach case management and patient care as the priority if you listen carefully what they really want first and foremost is volume or more prescriptions. I am asking self-funded employers a simple yet very important question. Does it make sense to have the same entity manage and approve specialty Rx claims when that entity stands to benefit when these claims are approved? If 90% or more of PAs are getting approved you might be a victim of rubber-stamping which leads to what? You guessed it – higher costs.

6) Restrict Access

A formulary is a list of medications for which a plan will provide reimbursement. When considering a formulary, access defines the basic aspects of a specialty pharmacy benefit design which includes but is not limited to:

- The products that will be covered

- The products that will not be covered

- The products that need prior approval

- Plan cap or maximum dollar amount a plan will pay for outpatient specialty drug benefits

- Mail service benefits, if any

- Specialty pharmacy network make up

Managing a formulary and improving its efficiency involves an ongoing assessment of the drugs on the formulary as well as any new potential drug therapy treatments. Again, do not leave this responsibility solely in the hands of the PBM unless it has agreed to accept fiduciary responsibility.

7) Medication Adherence

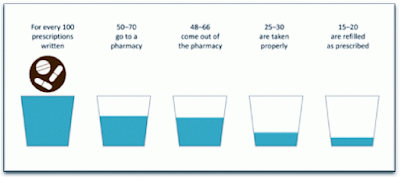

Medication adherence is a large and growing issue that has an impact not only on patients’ health, but also on employer finances. Non-adherence to medications has been linked to 30-50% of treatment failures and 125,000 deaths each year, according to

statistics gathered by the American College of Preventive Medicine.

|

Figure 1. Gap Between a Written Prescription and Actual Medication Use

[Source: National Association of Chain Drug Stores, Pharmacies: Improving Health, Reducing Costs, July 2010. Based on IMS Health data] |

In addition, non-adherence results in $290 billion in annual healthcare spending, $100 billion of which is due to hospitalization and rehospitalization that could have been avoided if medications were taken as prescribed. Simply put, even the most perfectly designed plan in the world can’t make up for poor adherence. Monitor adherence plan-wide and take corrective action for patients whose adherence is average or worse. A robust MTM program will address this issue and lower overall healthcare costs.

In summary, most plan sponsors don’t know what they don’t know. You should seek out only the best outside PBM expertise or better yet develop it in-house. Otherwise, you will leave tens of thousands of dollars on the table – this my friends is undeniable.