The Definition of Oversee: to watch over and direct (an undertaking, a group of workers, etc.) in order to ensure a satisfactory outcome or performance.

300 drugs now in generic ‘cartel’ probe and other notes from around the interweb:

300 drugs now in generic ‘cartel’ probe. What started as an antitrust lawsuit brought by states over just two drugs in 2016 have exploded into an investigation of alleged price-fixing involving at least sixteen companies and three hundred drugs, Joseph Nielsen, an assistant attorney general and antitrust investigator in Connecticut who has been a leading force in the probe, said. His comments represent the first public disclosure of the dramatically expanded scale of the investigation. The unfolding case is rattling an industry that is portrayed in Washington as the white knight of American health care. “This is most likely the largest cartel in the history of the United States,” Nielsen said. He cited the volume of drugs in the schemes, that they took place on American soil and the “total number of companies involved, and individuals.” The lawsuit and related cases picked up steam last month when a federal judge ruled that more than one million emails, cellphone texts and other documents cited as evidence could be shared among all plaintiffs.

PBMs pocketing savings from generic prescriptions, report says. The new report adds to a growing body of evidence showing that consumers overpay for generics, as “pharmacy benefit managers game opaque and arcane pricing practices to pad profits,” the white paper said. Generics make up more than 90% of prescriptions in the U.S. but just 18% of drug spending. By one estimate, the use of generic and biosimilar drugs in place of their branded equivalents saved the healthcare system $338 billion in 2020 alone. However, despite generics driving down prices relative to branded drugs, consumers are not benefiting from savings, the white paper said. “Generics are overlooked when we talk about drug pricing issues in this country,” said Erin Trish, co-director of the USC Schaeffer Center, in a statement. “But the same lack of transparency that is causing outrage over high and rising spending on branded drugs is also creating issues in the generic drug space.”

The drug rebate curtain. Lawyers for PBMs carefully define what a “rebate” means. For example, according to one template, “inflation payments” are not considered rebates. PBMs receive inflation payments from drug companies to cover year-over-year hikes to a drug’s list price. If employers don’t ask about inflation payments, PBMs keep them by default. The state of Delaware, however, modified its contract in 2015 to ensure those inflation payments are routed back to Delaware’s state employees, according to a copy of the contract that is publicly available.

Formulary Steering Prevents Members from Accessing Generics. A suit, first obtained by Stat, was filed by Alexandra Miller, who worked at CVS for nearly two decades before leaving the company three years ago. Miller says that when she reported the behavior to a superior, she was told that the company had decided the benefits of the alleged scheme outweighed the likelihood of being caught. Miller claims that CVS’ SilverScripts Part D subsidiary as well as its Caremark pharmacy benefit manager and retail pharmacies worked together to prevent access to generics, which allowed it to pocket higher rebates because members were pushed to buy branded medications rather than lower-cost options.

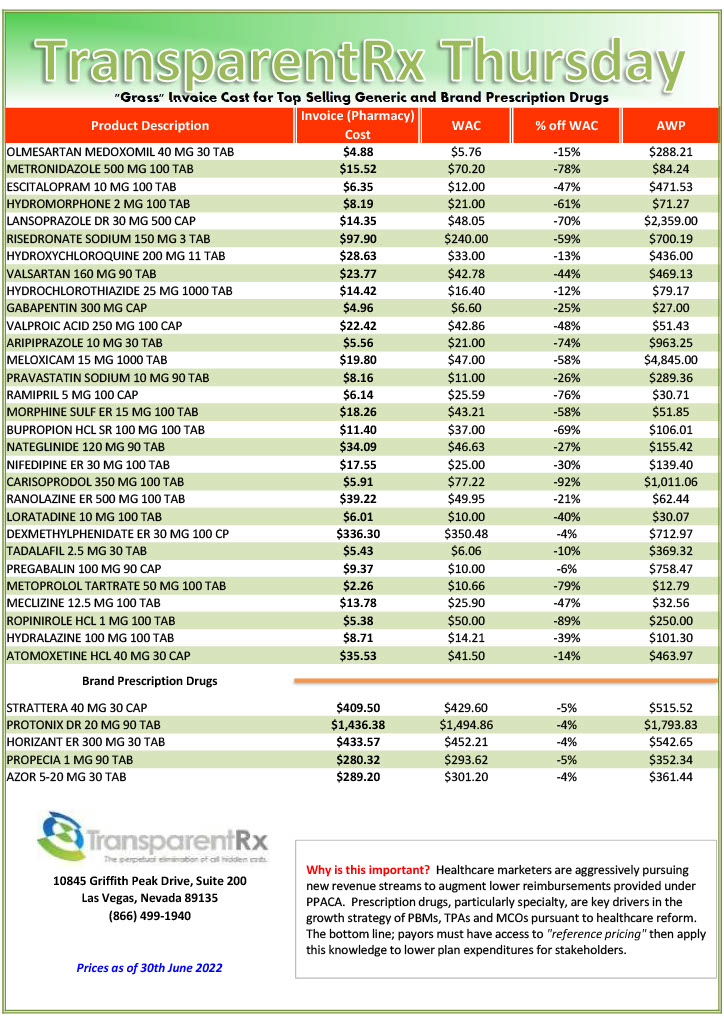

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

Large companies that spend billions of dollars a year on prescription drugs for their employees are hoping that the Federal Trade Commission’s inquiry into pharmaceutical benefit manager business practices will yield information that spurs major policy changes to reduce drug prices wrote Bloomberg Law. Prescription drug pricing isn’t the problem. Bloomberg Law has it wrong.

The FTC unanimously voted June 7 to conduct an inquiry into the PBM industry, sending compulsory orders to the six largest PBMs—CVS Caremark, Express Scripts Inc., OptumRx Inc., Humana Inc., Prime Therapeutics LLC, and MedImpact Healthcare Systems Inc.— to provide a wide range of information concerning the competitive impact of their contracting and business practices within 90 days. No date was set for issuing a special report from the information gathered.

Tyrone’s Commentary:

PBMs have always been tough negotiating with manufacturers and pharmacy networks for discounts. These negotiations have led to significant price concessions more than any other organization, government aside, could have negotiated for themselves. When those negotiations are completed, the pricing is set and accounts for inflation. We are hired to negotiate discounts. The problem isn’t the pricing it is the PBM’s management fee or Earnings After Cash Disbursements (EACD = AF + DF + IC + MR – CD).

The share of discounted pricing a PBM keeps for itself is its management fee or EACD. It would be like you calling up Amazon’s customer service on Prime Day and saying, “you know that 50% off deal for the Sony 75-inch television you are offering? Well, I don’t need that big of a discount, just make it 25%.” Because PBMs havesuperior information and knowledge, plan sponsors are giving discounts back to PBMs at the negotiating table. The focus should be on the PBMs’ management fee not pricing. This doesn’t mean that pricing isn’t important.

Until the industry standard becomes radical transparency, pricing is less important than the EACD. For example, a report by Nephron research says, “contracting entities are shifting discounts from the rebate profit pool 99% of which flows to clients to fee pools that may be retained by the PBM[i]. In other words, non-fiduciary PBMs have shifted their management fee to GMFs or group purchasing organization management fees. They’ve also shielded themselves from spread pricing revenue loss by powering discount cards.

Conclusion – Prescription Drug Pricing Isn’t The Problem. Bloomberg Law Has It Wrong

Bloomberg law writes, “among employers concerns a lack of transparency into whether PBMs are fully refunding rebates and discounts negotiated with drug manufacturers.” Non-fiduciary PBMs intentionally make it difficult to ascertain their management fee. It is easier to get away with an unfair management fee or overcharging when the purchaser has no clue what it amounts to. When a problem is misdiagnosed, the solution is inevitably wrong or inefficient.

[i] Fein, Adam PhD, Drug Channels News Roundup, June 2020: CVS’s New GPO, CMS on Copay Accumulators, GoodRx Fees, Supermarket Pharmacies, and Merck’s Ken Frazier, June 24, 2020, https://www.drugchannels.net/2020/06/drug-channels-news-roundup-june-2020.html

Formulary steering prevents members from accessing generics and other notes from around the interweb:

Formulary Steering Prevents Members from Accessing Generics. A suit, first obtained by Stat, was filed by Alexandra Miller, who worked at CVS for nearly two decades before leaving the company three years ago. Miller says that when she reported the behavior to a superior, she was told that the company had decided the benefits of the alleged scheme outweighed the likelihood of being caught. Miller claims that CVS’ SilverScripts Part D subsidiary as well as its Caremark pharmacy benefit manager and retail pharmacies worked together to prevent access to generics, which allowed it to pocket higher rebates because members were pushed to buy branded medications rather than lower-cost options.

PBMs pocketing savings from generic prescriptions, report says. The new report adds to a growing body of evidence showing that consumers overpay for generics, as “pharmacy benefit managers game opaque and arcane pricing practices to pad profits,” the white paper said. Generics make up more than 90% of prescriptions in the U.S. but just 18% of drug spending. By one estimate, the use of generic and biosimilar drugs in place of their branded equivalents saved the healthcare system $338 billion in 2020 alone. However, despite generics driving down prices relative to branded drugs, consumers are not benefiting from savings, the white paper said. “Generics are overlooked when we talk about drug pricing issues in this country,” said Erin Trish, co-director of the USC Schaeffer Center, in a statement. “But the same lack of transparency that is causing outrage over high and rising spending on branded drugs is also creating issues in the generic drug space.”

The drug rebate curtain. Lawyers for PBMs carefully define what a “rebate” means. For example, according to one template, “inflation payments” are not considered rebates. PBMs receive inflation payments from drug companies to cover year-over-year hikes to a drug’s list price. If employers don’t ask about inflation payments, PBMs keep them by default. The state of Delaware, however, modified its contract in 2015 to ensure those inflation payments are routed back to Delaware’s state employees, according to a copy of the contract that is publicly available.

Site-of-Care Management Oncology Infusion Moving From Hospital to Home. “If your institution, department or program does not have a home infusion setup for your oncology patients, you need to start working on it.” That was the message from Laure DuBois, PharmD, BCOP, pharmacy clinical coordinator at the University of Kansas Medical Center, in Kansas City, discussing the increasing trend toward site-of-care management at a session at the 2022 annual meeting of the Hematology/Oncology Pharmacy Association. “At our institution, we first observed this with Aetna wanting to transfer patients on PD-L1 [programmed death ligand-1] inhibitors to home infusion by self-injection or the physician’s office,” Dr. DuBois said. “These policies are increasingly in place for many supportive care medications, as well as some targeted therapies.”

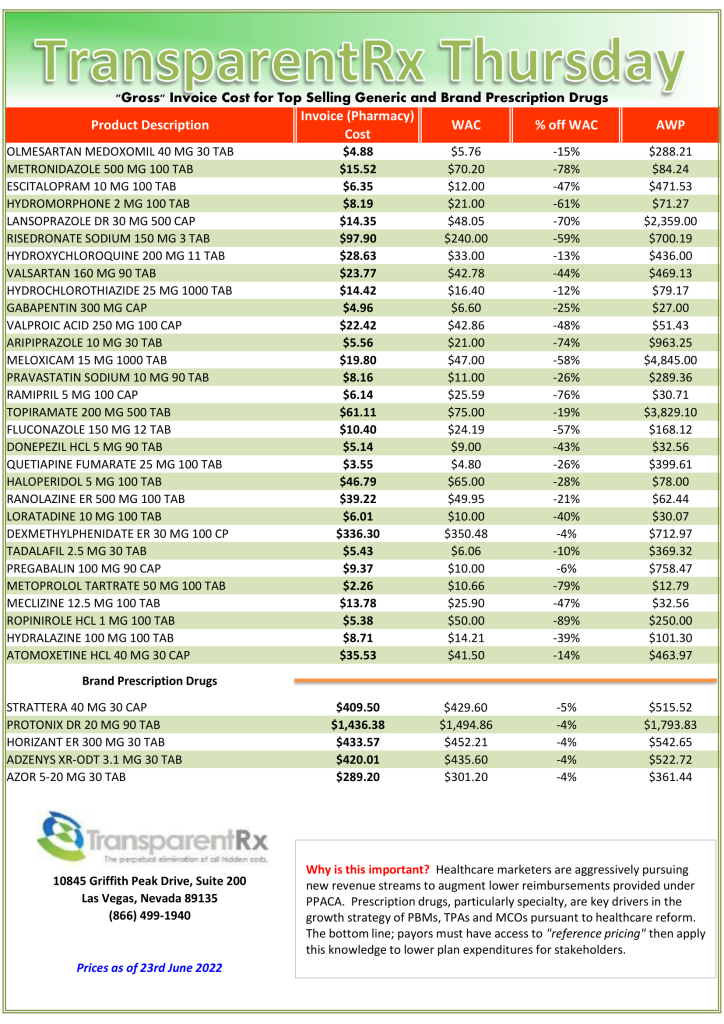

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

How pharmacy benefit managers (PBM) make money is an extremely complex web of deception. Non-fiduciary pharmacy benefit managers say, “We will contain your costs. We will lower drug prices.” They have not backed up their words with action. Instead, non-fiduciary pharmacy benefit managers have opted for personal financial gain at the expense of clients, plan participants and other stakeholders. Some pharmacy benefit managers have even gone as far as to admit publicly that it isn’t their responsibility to contain prescription drug costs. PBMs have three primary responsibilities: cost-containment, safety, and healthcare outcomes. The pharmacy benefits management industry, including consultants, has done a poor job in all three areas. Let’s look at five ways how non-fiduciary PBMs make money by skirting cost-containment responsibilities.

Formulary Steering. Occurs when patients are steered toward certain brand drugs on formulary when a lower cost usually generic equivalent or therapeutic alternative is available. A newly unsealed whistleblower suit claims that multiple CVS Health subsidiaries coordinated to prevent members from accessing generic drugs in a bid to boost the bottom line. The suit was filed by Alexandra Miller who worked at CVS for nearly two decades before leaving the company three years ago. Miller claims that CVS’ SilverScripts Part D subsidiary as well as its Caremark pharmacy benefit manager and retail pharmacies worked together to prevent access to generics, which allowed it to pocket higher rebates because members were pushed to buy branded medications rather than lower-cost options. Miller says that when she reported the behavior to a superior, she was told that the company had decided the benefits of the alleged scheme outweighed the likelihood of being caught[i].

Rubberstamping. Happens when a pharmacy benefit manager doesn’t employ utilization management protocols effectively. Drug utilization management includes but is not limited to prior authorization, step therapy, quantity limits, refill to soon, and drug utilization reviews. The New York City Transit Authority hired ESI to administer and manage the prescription drug benefits NYCTA offered to its employees, retirees, and dependents. In the year prior to contracting with ESI, NYCTA paid $6 million for compounded prescription claims. To the shock and awe of the NYCTA, in the first year of its contract with ESI, NYCTA paid over $38 million for compounds. In fact, in June 2016, only two months after the contract term began, an individual’s claim for an erectile dysfunction compound medication totaled $405,325.43 over three months. Critically, a sizable portion of the compound claims contributing to the substantial increase in spending originated from just three providers and were largely fraudulent. Disturbingly, ESI conducted its own investigations into two of the providers and neglected to share the results with NYCTA. ESI likely approved overpriced compounds because ESI may have earned “spread pricing” on such claims—this litigation will reveal the truth[ii].

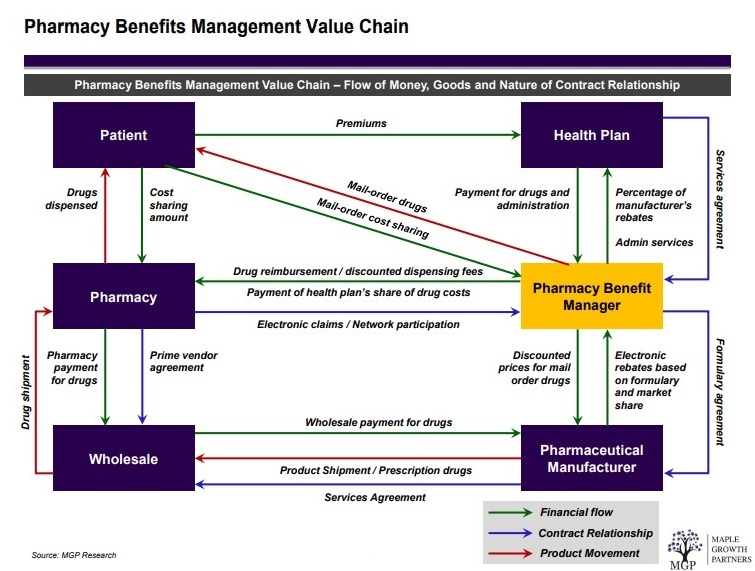

Figure 1. Pharmacy Benefits Management Distribution and Reimbursement System

Spread Pricing. Takes place when a pharmacy benefit manager reimburses a network or in-house pharmacy less than the amount billed and subsequently collected from a plan sponsor (see figure 1). The state of Ohio released data showing how private companies manage $2.5 billion in public money for pharmacy benefits for Ohioans on Medicaid. The middlemen, called pharmacy benefits managers, are under scrutiny for how transparent they are in how the public money gets spent. The report shows the companies retained (spread) $223.7 million of the money they billed Medicaid. The state of Ohio promptly terminated each contract.

Rebates. Have increased in lock step with list price since at least 2013. For example, internal company documents collected for the U.S. Senate Committee’s investigation show that, in 2013, average rebates for long-acting insulin products hovered around 2% and 4% for preferred formulary placement. However, approximately six years later, rebates for the same product were as high as 79.75%[iii]. It’s important to note that rebates vary by product, payer, and placement on a plan’s formulary. WAC data collected for the Committee’s investigation also suggest list prices for long-acting and short-acting insulins have increased rapidly during this same period.

Information Asymmetry. Is an imbalance between two negotiating parties in their knowledge of relevant factors and details. Typically, that imbalance means that the side with more information enjoys a competitive advantage over the other party. Non-fiduciary PBMs and some advisors have been leveraging information asymmetry or information failure to their financial benefit. Documents provided to Axios[iv] reveal a new layer of secrecy within the maze of American drug pricing — one in which firms that manage drug coverage for hundreds of employers, representing millions of workers, obscure the details of their work and make it difficult to figure out whether they’re providing a good deal. Each of the predominant health care consulting firms — Aon, Mercer, and Willis Towers Watson — has its own prescription drug coalition made up of employers. The conventional wisdom is firms use the combined scale to negotiate lower drug prices with large pharmacy benefit managers, but there’s no hard evidence the coalitions provide meaningful savings.

Conclusion: How pharmacy benefit managers (PBM) make money

John F. Kennedy said, “The greater our knowledge increases the more our ignorance unfolds.” Most self-insured employers, and their advisors, don’t know what they don’t know. Pharmacy Benefit Managers provide transparency and disclosure to a level demanded by the competitive market and generally rely on the demands of prospective clients for disclosure in negotiating their contracts. The best proponent of transparency is informed and sophisticated purchasers of PBM services. The purchaser needs to understand not only what they want to achieve in their relationship with their PBM but also the competitive market and their ability to drive disclosure of details on services important to them. Assessing transparency is done more effectively by a trained eye with personal knowledge of the purchaser’s benefit and disclosure goals. Consequently, the average self-insured employer is paying 67% more for PBM services than needed.

[i] Paige Minemyer, Senior Editor, Whistleblower suit: CVS prevented Part D members from accessing generics, June 16, 2022, Fierce Healthcare, https://www.fiercehealthcare.com/payers/whistleblower-suit-cvs-prevented-part-d-members-accessing-generics.

[ii] Jonathan E. Levitt, Esq., Dae Y. Lee, Pharm.D., Esq., CPBS, and Adam C. Farkas, Esq., PBMs could be driving up plan sponsors’ drug costs, June 15, 2022, BenefitsPro, https://www.benefitspro.com/2022/06/15/pbms-could-be-driving-up-plan-sponsors-drug-costs/.

[iii] Congress of the United States, 5/16/2022, FTC-2022-0015-0001 Solicitation for Public Comments on the Business Practices of Pharmacy Benefit Managers and their Impact on Independent Pharmacies and Consumers.

[iv] Bob Herman, 12/6/2021, Documents reveal the secrecy of America’s drug pricing matrix, 12/21/2021, <https://www.axios.com/2021/12/06/aon-express-scripts-contract-employers-drug-price-data>

The Future of Employer Sponsored Healthcare Plans Is Cost Management and other notes from around the interweb:

6 Payor Tactics to Control Drug Spending. Pressure is building to shift to the medical benefit. Plans didn’t historically manage drugs on the medical benefit as strictly as the pharmacy benefit, but now there is increasing economic pressure to do so, Dr. Grant said. Payor strategies here include aggressive site-of-care optimization strategies directing patients to the most cost-effective location to receive medications, and requiring billing through specialty pharmacies, known as bagging strategies, where health systems and physician practices must accept bagged medications from pharmacies to administer to patients. The best option is gold bagging, in which a specialty pharmacy dispenses prescriptions to its own clinics for administration, she said. Some states and professional groups, such as the American Hospital Association, have banned or oppose bagging for its potential disruptions in care.

The Future of Employer Sponsored Healthcare Plans Is Cost Management. Rising inflation and its effect on healthcare costs and spending has put price transparency in the spotlight. As of January 1, 2021, the Centers for Medicare and Medicaid Services (CMS) mandated that U.S. hospitals provide clear, accessible pricing information online about the items and services they provide. Greater transparency confirms that significant price variations exist across hospitals and providers for standard medical procedures. To mitigate this, many self-funded health plans have adopted a reference-based pricing (RBP) strategy.

Expert Discusses New Specialty Drugs That are in the Pipeline. In the non–small cell lung cancer space, therapies are really being targeted towards this specific gene expression. There are a lot of different gene mutations and just keeping an eye on the various agents in the pipeline as their mechanisms are tailored very specifically to those gene mutations and expressions. That was really what she highlighted as far as non–small cell lung cancer. As far as breast cancer treatments, Dr. Khullar really did a great job of discussing the oral SERDs, which are very specific to hormone positive breast cancer treatments. Those specific cancers are usually very resistant to the current agent. The agents in that class of SERDs for breast cancer treatment are really important to monitor for.

Site-of-Care Management Oncology Infusion Moving From Hospital to Home. “If your institution, department or program does not have a home infusion setup for your oncology patients, you need to start working on it.” That was the message from Laure DuBois, PharmD, BCOP, pharmacy clinical coordinator at the University of Kansas Medical Center, in Kansas City, discussing the increasing trend toward site-of-care management at a session at the 2022 annual meeting of the Hematology/Oncology Pharmacy Association. “At our institution, we first observed this with Aetna wanting to transfer patients on PD-L1 [programmed death ligand-1] inhibitors to home infusion by self-injection or the physician’s office,” Dr. DuBois said. “These policies are increasingly in place for many supportive care medications, as well as some targeted therapies.”

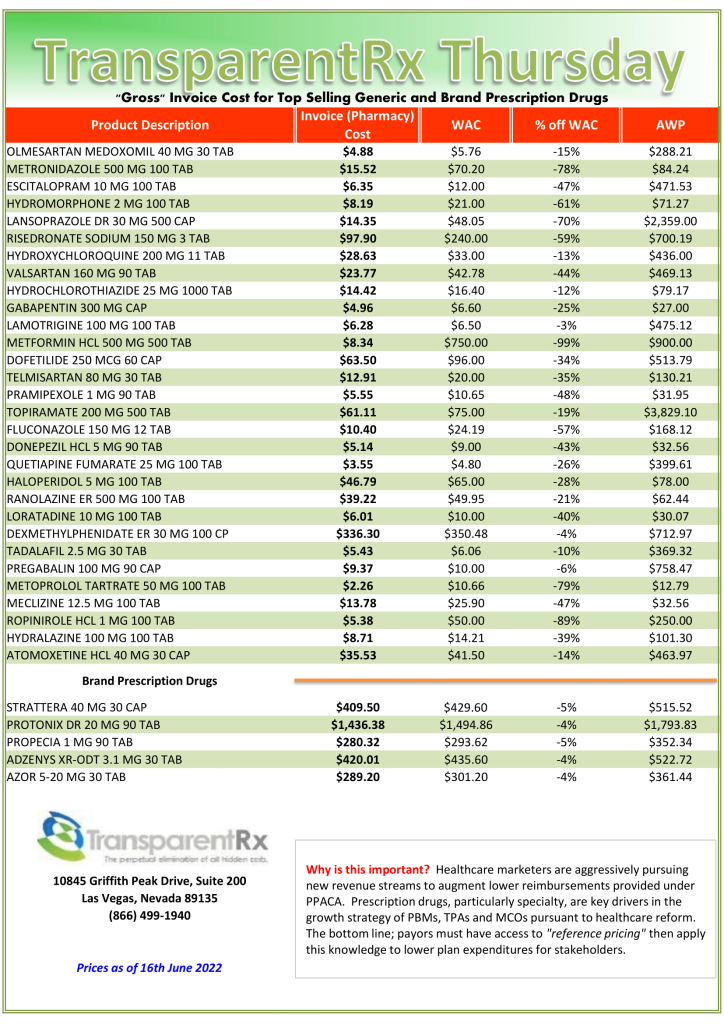

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

Claims repricings are an integral part of what a growing fiduciary-model PBM does daily. I happen to believe that plan sponsors and their advisors rely too heavily on them. In fact, I wrote recently, “each time a non-fiduciary PBM gets caught with its hand in the cookie jar you can’t go beyond the first sentence of the obfuscation without the word CONTRACT being thrown around. Yet, when you ask self-funded employers or their advisors what’s most important to them when evaluating PBM proposals you get CLAIMS REPRICING. PBM contract nomenclature sets the foundation for all the financials. A 400 question RFP might make you feel better, but it doesn’t deliver results or in this case radical transparency. PBM literacy, on the other hand, delivers results. PBM transparency is best determined by a trained eye. When the PBM operates with radical transparency, you CANNOT overpay. The same cannot be said for even the most aggressive claims repricing or rebate guarantees unaccompanied by a fiduciary standard of care and/or radical transparency.” It was written in response to the Louisiana Attorney General’s recent lawsuit against a large PBM. Keep reading for the three meaningful PBM formulary management tips to take advantage of so not to be taken advantage of.

Even though I’m not a huge fan of claims repricings, I am intrigued by the process and results. For example, in the results below (figure 1) you will see that TransparentRx’s price difference alone isn’t enough to warrant a PBM vendor change. This always concerns me as most plan sponsors don’t look beyond the claims repricing results. It isn’t until you look at the incumbent PBM’s clinical performance (product mix and utilization) that there is a problem big enough to consider that something must change. Formulary management is a clinical service. The Generic Dispense Rate or GDR is only 79%. Fortunately for us our book performance is in line with the national GDR average of 90%! Furthermore, for every 1% increase in GDR a self-insured employer can expect to reduce drug costs by 2.5%. This employer was leaving $650,000 annually on the table all because of poor clinical oversight. More specifically, drug utilization management processes were rubberstamped, and the formulary managed inefficiently. Here are three PBM formulary management tips to take advantage of so not to be taken advantage of.

Don’t give up cost control to make participants happy. At the beginning of the pandemic employers, at the behest of PBMs, decided to open the flood gates for prescription drugs. They removed safety nets such as refill too soon, quantity limits and step therapy. The only entities to benefit were the PBMs themselves as volume increased significantly. Worse yet, some of these plans have not yet reverted to pre-pandemic drug utilization management protocols. Proper pharmacy benefits management practices call for safety and efficiency first no matter the circumstances. Critics, prescribers and patients, view cost control as impeding on what’s best for them. We “had” a client who insisted their employee be allowed to have a brand drug dispensed for $2000 although the generic drug would have cost less than $200. There was no clinical reason only that the employee didn’t want to take a generic. If it were going to cost you money or put employees in danger, you wouldn’t change your manufacturing processes just to make an employee happy. So why do it in your employer-sponsored pharmacy benefits program?

Treat formularies as a cost-containment tool not a recruiting tool. Price is the most common driver of pharmacy costs. Drug pricing takes into consideration AWP discounts, inflation, and rebates, for example. Cost share is the second driver of pharmacy cost HR and finance are most familiar. Cost sharing consists of coinsurance, copays and more recently accumulator and maximization programs. However, there are two big drivers of pharmacy cost that often get overlooked and they are utilization and product mix. Since I’ve already addressed product mix let’s look at utilization. Formularies are often used in conjunction with drug utilization management tools such as refill too soon, step therapy, quantity limits, dose optimization, prior authorization, or pill splitting, for example. An efficient combination of benefit design, utilization and product mix offers the best of both worlds; maximization of participant choice while simultaneously helping to reduce final plan drug costs. If you want to learn more about plan design, formulary, or utilization management techniques, join our next Certified Pharmacy Benefits Specialist class.

Opt for a closed formulary. As an employer myself, it just never made sense to me that my peers say, “here is my checkbook have at it.” The fundamentals which allowed the business to grow are somehow lost after the business becomes successful. As a side, Carl Icahn’s documentary “The Restless Billionaire” is fascinating. Check it out if you haven’t already. He talks a lot about wasteful spending. In pharmacy benefit plans, thousands of dollars are paid for drugs when a $100 generic drug would provide similar clinical benefits. Worse yet,millions of dollars are spent on drugs with no clinical benefit. An open formulary is a list of medications which has no limitation to access to a medication by a practitioner. A closed formulary on the other hand, is a list of medications (formulary) which limits access of a practitioner to some medications. The truth is efficiency (cost control and clinical outcomes), and participant satisfaction are exceedingly difficult if not impossible to separate. The path to clinical success in pharmacy benefits management gets clearer with a closed formulary.

PBM Formulary Management Tips: Three That Are Meaningful, Conclusion

Unless it has contractually agreed to contain your costs, do not leave the responsibility of formulary management solely in the hands of the PBM. When rebates are involved, the formulary could become a tool for favoring drugs from preferred manufacturers instead of a tool to maximize clinical benefit.

6 Payor Tactics to Control Drug Spending and other notes from around the interweb:

6 Payor Tactics to Control Drug Spending. Pressure is building to shift to the medical benefit. Plans didn’t historically manage drugs on the medical benefit as strictly as the pharmacy benefit, but now there is increasing economic pressure to do so, Dr. Grant said. Payor strategies here include aggressive site-of-care optimization strategies directing patients to the most cost-effective location to receive medications, and requiring billing through specialty pharmacies, known as bagging strategies, where health systems and physician practices must accept bagged medications from pharmacies to administer to patients. The best option is gold bagging, in which a specialty pharmacy dispenses prescriptions to its own clinics for administration, she said. Some states and professional groups, such as the American Hospital Association, have banned or oppose bagging for its potential disruptions in care.

PBMs pocketing savings from generic prescriptions, report says. The new report adds to a growing body of evidence showing that consumers overpay for generics, as “pharmacy benefit managers game opaque and arcane pricing practices to pad profits,” the white paper said. Generics make up more than 90% of prescriptions in the U.S. but just 18% of drug spending. By one estimate, the use of generic and biosimilar drugs in place of their branded equivalents saved the healthcare system $338 billion in 2020 alone. However, despite generics driving down prices relative to branded drugs, consumers are not benefiting from savings, the white paper said. “Generics are overlooked when we talk about drug pricing issues in this country,” said Erin Trish, co-director of the USC Schaeffer Center, in a statement. “But the same lack of transparency that is causing outrage over high and rising spending on branded drugs is also creating issues in the generic drug space.”

How Pharmacy Benefit Managers (PBM) Make Money – PBM Accountability Project. PBMs derive much of their revenue from collecting a range of service fees and other charges from manufacturers, pharmacies, and other supply chain entities, ultimately driving up the cost of the prescription drugs. A new study by the PBM Accountability project shines a light on the PBM business model, often described as a “black box,” revealing the sources of growth in PBM gross profit between 2017 and 2019.

Federal Trade Commission opens investigation into pharmacy benefit managers. The FTC will send orders to CVS Caremark, Express Scripts Inc., OptumRx Inc., Humana Inc., Prime Therapeutics LLC and MedImpact Healthcare Systems Inc. and will examine the “impact of vertically integrated pharmacy benefit managers on the affordability and accessibility of prescription drugs,” the agency said. According to the release, the inquiry will aim to closely investigate the role of pharmacy benefit managers in the U.S. pharmaceutical system, which may entail financial and policy involvement with drug manufacturers, health insurance companies and pharmacies. These functions are often clouded by “complicated, opaque contractual relationships that are difficult or impossible to understand for patients and independent businesses across the prescription drug system,” the release said.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.