The Definition of Oversee: to watch over and direct (an undertaking, a group of workers, etc.) in order to ensure a satisfactory outcome or performance.

Because plan sponsors don’t know how to calculate how much money pharmacy benefit managers (PBM) make, it gives PBMs all the incentive they need to overcharge. How many businesses do you know want to cut their revenues in half? That’s why traditional pharmacy benefit managers, and their stakeholders, don’t offer a fiduciary standard of care and instead opt for hidden cash flow opportunities to generate their service fees. Want to learn more?

“Thank you, Tyrone, for this informative meeting.” David Wachtel, VP

“…Great presentation! I had our two partners at the presentation as well. Very informative.” Nolan Waterfall, Agent/Benefits Specialist

A snapshot of what you will learn during this 30-minute webinar:

Hidden cash flows in the PBM Industry

Basic to intermediate level PBM terminologies

Specialty pharmacy cost-containment strategies

Examples of drugs that you might be covering that are costing you

The #1 metric to measure when evaluating PBM proposals

Understanding how PBMs make money and how much you pay them for their services is a key element in running an efficient pharmacy benefits program. Join us to learn more.

2023 Large Employers’ Health Care Strategy and Plan Design Survey and other notes from around the interweb:

2023 Large Employers’ Health Care Strategy and Plan Design Survey. The recently reported, 2023 Large Employers’ Health Care Strategy and Plan Design Survey, released by the Business Group on Health, surveyed 135 large employers that covered more than 18 million people. Respondents were contacted between May 31, 2022, and July 13, 2022. Affordability remains a top concern for employers. It is one they haven’t been as successful in addressing via remediation and negotiation efforts when compared to other areas of patient engagement, including experience, access, and quality. Employers will continue to assert market influence in addressing affordability with their partners. However, they are also keenly focused on policy efforts regarding affordability. For this reason, lowering health care costs and prescription drug expenses and making more affordable coverage possible are among employers’ top future health care reform priorities. Employers are particularly concerned about both the affordability of maintenance medications and newer gene therapies.

Six Things to Look Out for Within the Rebates Section of Your Pharmacy Benefit Management Contract. Prior to signing your Pharmacy Benefit Management (PBM) contract, it’s essential to pay particularly close attention to the pharmacy services that provide cost-containment strategies. One vital component you should focus on is the rebate administration. Today, we are sharing six areas within the rebate section of your PBM contract, to help you maximize savings and mitigate risk.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

3 reasons why owning pharmacy benefits data matters. The Federal Trade Commission is pushing PBMs for greater transparency to help employers take control of their prescription costs. But what is transparency without access to plan data or performance analytics? Currently, employers are disempowered because too many don’t own their data, must pay extra to get access to what should already be theirs, or only receive partial access. These PBM practices of obscuring data have led to significant distrust from all stakeholders. To fix a broken system, the data being hidden by these third parties needs to be freed to provide employers and plan members with the information they need to find the path to lower costs.

In pharmacy benefit management (PBM) competitive bidding processes, a broker or consultant identifies 3 – 10 pharmacy benefit managers and invites each to submit a proposal. The entire bidding process, from development of the request for proposal (RFP) packet to selection of the winning bidder, can take as little as a month to two years. The latter is reserved for larger clients such as unions, state, or federal plans. The conventional PBM RFP process is flawed read on to learn how to fix it.

The packet a PBM receives from a consultant as part of the RFP process can include claims data, census data such as date of birth, sex, name, dependent status, or address, and incumbent PBM contracts. Once all bids are collected the consultant then plugs them into their in-house Excel spreadsheet or a third-party bid analyzer software platform. This is where the problems begin more on that in a bit.

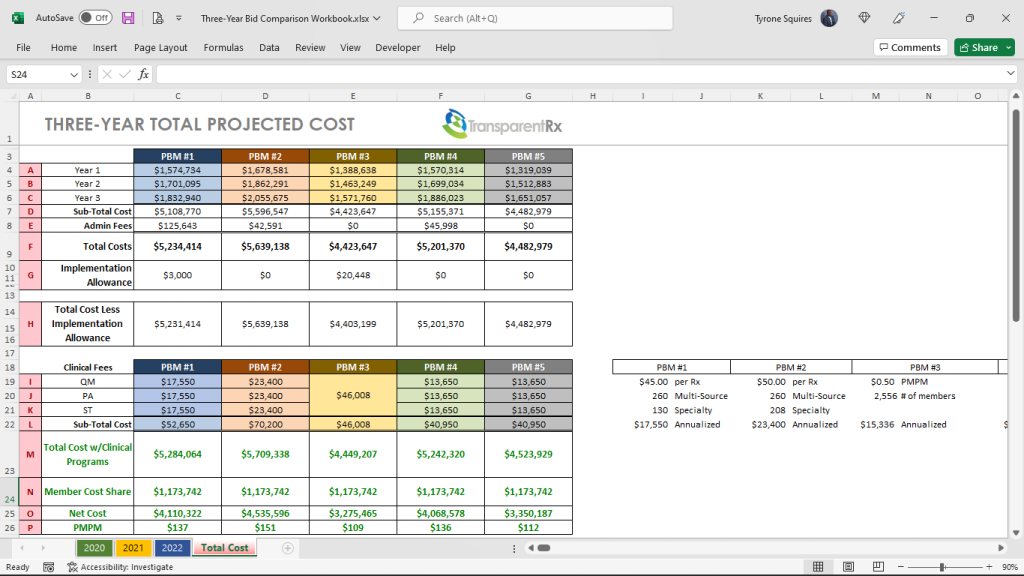

Figure 1: Three-Year PBM Bid Comparison Workbook

Figure 1 provides a glimpse into the pricing a consultant, CFO, or CHRO might look at when evaluating PBM bids. Financials are just one criterion others include but are not limited to:

Accreditation support to pharmacy UM and Credentialing (5%)

Clinical support services (15%)

Explaining Differentiators (5%)

Health support services, including data integration (10%)

Implementation plan (10%)

Member service capabilities (5%)

Pricing and Transparency (50%)

Each criterion is usually scored, with a weighted average, based upon client needs. Since pricing is most important to the client in the example above, pricing weighs the heaviest (50%) in the final score. Because most evaluators in a PBM competitive bidding process are not experts, they tend to rely on what they know which is two is less than three. I wish it were that simple. Michael Critelli, former CEO at Pitney Bowes, sent me a message a few years back tackling this very point.

I’ve been teaching pharmacy benefits management for six years and just recently came to realize the forethought of his message. Michael wrote, “I am pleased that you authored the essay I downloaded. Many corporate benefits departments do not understand that they are overmatched in negotiating with pharmacy benefit managers, as are the “independent consultants” who routinely advise them. The first step in being wise and insightful is admitting what we do not know, and you have humbled anyone who touches this field.” There is a tidal wave of increased drug [specialty] spending on the horizon. One change will level set corporate benefits departments against pharmacy benefit managers at the negotiating table.

The one change corporate benefits departments orsteering committees must make is to put the PBM contract at the front of the competitive bidding process and keep it there. It is unthinkable that many corporate benefits departments select a winning PBM bid before even looking at or finalizing the contract. The PBM services agreement sets the foundation for all the financials.

Staff, including legal, have inadequate knowledge of the PBM industry especially around contracting and driving meaningful transparency. Achieving optimal outcomes, cost and clinical, will be more effectively done by a trained eye with personal knowledge of the purchaser’s benefit and disclosure goals. Drafting, negotiating, and finalizing a contract with a PBM are the three most important tasks during an RFP. Here are some additional steps to take:

Require consulting firms to have skilled staff working on the deal with extensive PBM knowledge. Twenty years of consulting experience, CEBS, SHRM-SCP, JD or PharmD alone doesn’t come close to fulfilling this requirement. Pharmacy benefits are more complicated than medical benefits. Verifying PBM knowledge will require third-party attestations such as CPBSTM.

Require consulting firms to draft, negotiate, and finalize the PBM contract before a winner is announced.

Conduct extensive legal negotiations memorializing increasingly better terms and prices; every PBM will have made some changes.

Require consulting firms to sign disclosure forms identifying all PBM $$$ and relationships.

Draft an entirely different contract that eliminates all loopholes including blanks for pricing terms & guarantees PBMs will fill in with their offers. In lieu, sign an agreement with a PBM who offers the full extent of ERISA fiduciary language.

The Conventional PBM RFP Process Is Flawed – Here’s the #1 Way to Fix It (Conclusion)

In figure 1 which financial bid is better? It is impossible to know, with any degree of certainty, without first conducting an expert review of the contract starting with the definitions. PBM financial proposals are easily diluted with opaque contract language. The winning PBM can easily explain your YOY costs increasing by blaming new high-cost claimants, for instance. Furthermore, large PBMs have staff analysts whose primary responsibility is to pull levers left available to them, via opaque contract language, taking margins from 10% to 30% of your final plan cost. If a plan spends $10,000,000 on pharmacy benefits, $3,000,000 of that spend should never be attributable to the PBM’s management fee or take home. A lack of meaningful transparency should be a dealbreaker. The #1 way to fix the conventional PBM RFP process is to make the PBM contract the most important part of the competitive bidding process. PBM services, while especially important, have been commoditized, don’t treat them like the Hope diamond.

PBM Ordered to Pay Aids Healthcare Foundation (AHF) $23 million and other notes from around the interweb:

PBM Ordered to Pay Aids Healthcare Foundation (AHF) $23 million. The United States District Court for the District of Arizona has confirmed an earlier arbitration judgment of $23 million awarded to AIDS Healthcare Foundation (AHF) against Caremark LLC, a subsidiary of the pharmacy giant CVS, for unfair reimbursement practices. In November 2019, AHF filed suit with the American Arbitration Association against Caremark LLC, a pharmacy benefits manager (PBM), for breach of agreement and the covenant of good faith and fair dealing. The dispute arose from Caremark’s unfair practice of chargebacks on prescriptions filled by AHF pharmacies on behalf of insurance prescription plan sponsors such as those covering Medicare Plan D beneficiaries. As a result of the chargebacks by Caremark, for several years AHF was being reimbursed less than what Part D plan sponsors received in prescription reimbursement from public Part D monies.

Six Things to Look Out for Within the Rebates Section of Your Pharmacy Benefit Management Contract. Prior to signing your Pharmacy Benefit Management (PBM) contract, it’s essential to pay particularly close attention to the pharmacy services that provide cost-containment strategies. One vital component you should focus on is the rebate administration. Today, we are sharing six areas within the rebate section of your PBM contract, to help you maximize savings and mitigate risk.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

3 reasons why owning pharmacy benefits data matters. The Federal Trade Commission is pushing PBMs for greater transparency to help employers take control of their prescription costs. But what is transparency without access to plan data or performance analytics? Currently, employers are disempowered because too many don’t own their data, must pay extra to get access to what should already be theirs, or only receive partial access. These PBM practices of obscuring data have led to significant distrust from all stakeholders. To fix a broken system, the data being hidden by these third parties needs to be freed to provide employers and plan members with the information they need to find the path to lower costs.

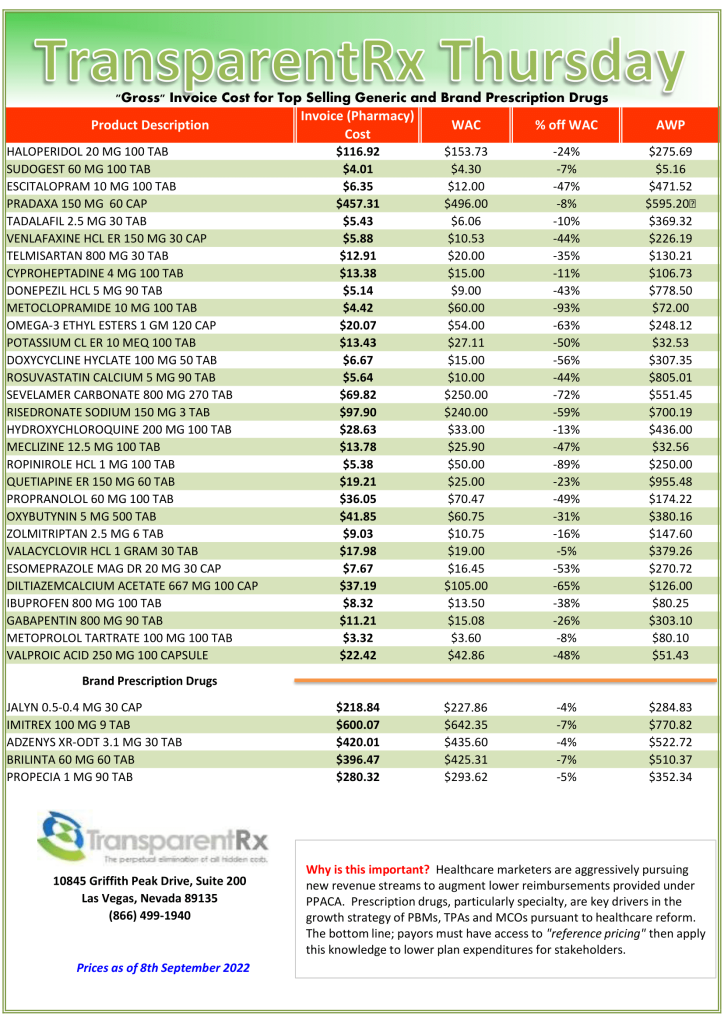

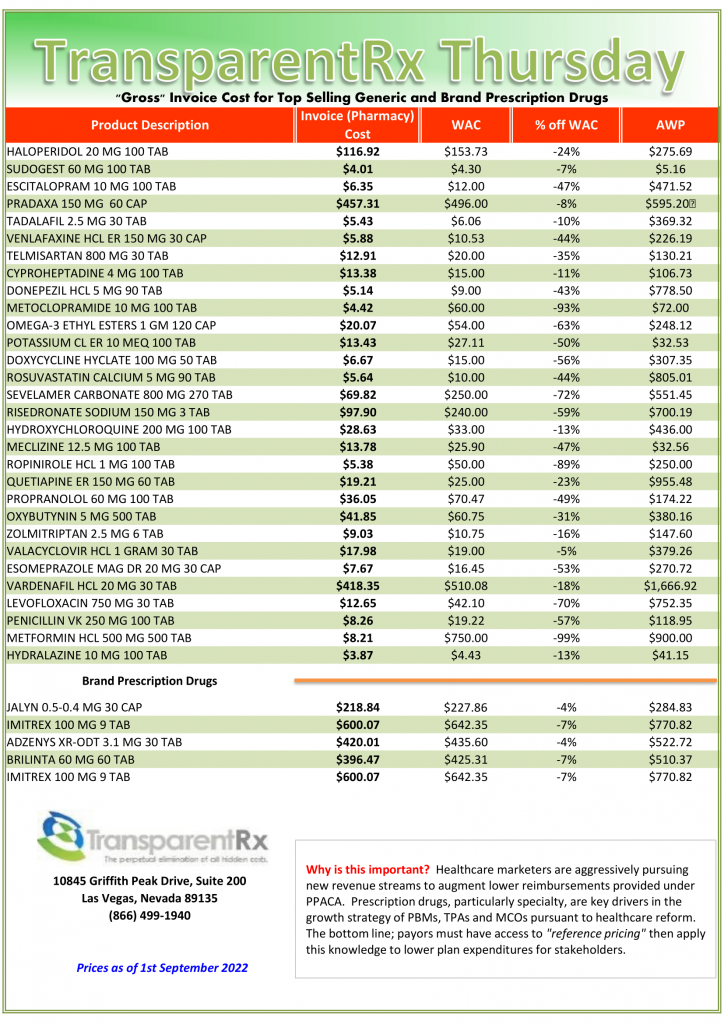

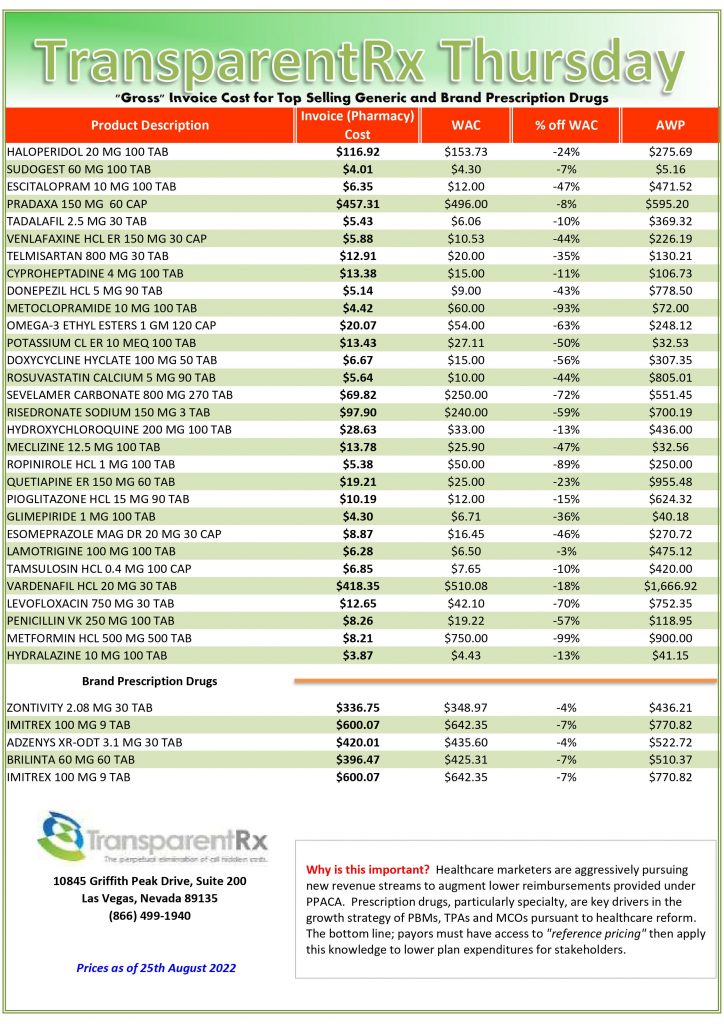

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

In pharmacy benefit management, pass-through doesn’t mean what you think it means hence the title of this post 6 Indicators Your PBM is Hoarding Rebates. A logical person would surmise that when a pharmacy benefit manager (PBM) professes it is pass-through, any discounts it has negotiated are distributed back to the client. Au contraire mon frere.

Pass-through pricing means that the PBM passes the discounts, rebates, other revenues, and actual costs charged by the pharmacy or paid by a pharmaceutical company (in the form of refunds) directly on to the plan sponsor. In actual use, it can have various definitions according to the understanding of the parties.

When a PBM salesperson tells you its organization is pass-through, they aren’t necessarily being untruthful. What they and you must understand is that in practice they are passing through only the discounts or refunds required by the contractual terms. The typical PBM salesperson is working with limited industry knowledge, so they don’t know any better. If there is a loophole, you must assume the PBM will take financial advantage of it.

The term pass-through must be carefully defined in the contract in every instance it is used since there is no industry-accepted definition. If the term is not included in the contract, add it. I spoke with a broker recently who was adamant that the deal they negotiated for their client was pass-through. When I pushed back the broker insisted that the contract was pass-through because the PBM told him so.

The base administrative fee for services related to pharmacy benefits management including, but not limited to, mail services, clinical services, and customer service was $0.00. I asked, rhetorically, how can the PBM make a profit if not through hidden cash flow streams when there is no administrative fee? It is not possible for a PBM contract to be truly pass-through when it waives the administrative fee. Here are 6 indicators your PBM is hoarding rebates.

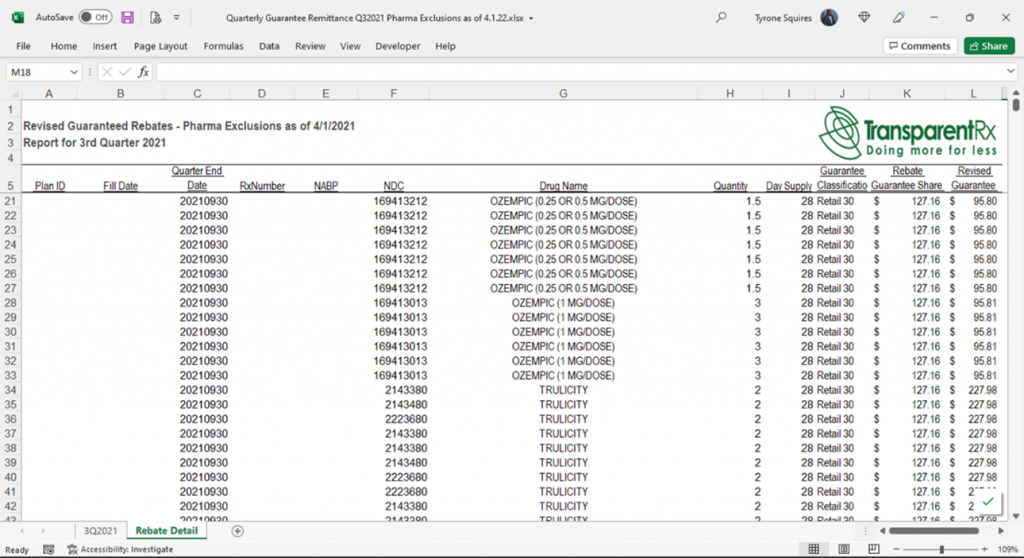

Figure 1. Actual Rebate Remittance Summary Report

The base administrative fee for services related to pharmacy benefits management including, but not limited to, mail services, clinical services, and customer service is artificially too low. It is not possible for a PBM to be truly pass-through when it waives the administrative fee or doesn’t charge enough to cover overhead.

The definition for rebates in the contract language is opaque. One example is “…and directly attributable to the Formulary and Covered Product utilization by Eligible Persons.” Allowing contract language such as this the broker unknowingly permits the PBM to retain at least 15% of rebate dollars.

You forgo all or a portion of rebates to take a credit on the medical administrative fee. Heck, you may as well call it for what it is – a bonus payment. The PBM’s pricing analysts will shift costs to make up for any “credit.” What’s more, these credits incentivize the PBM to dispense more brand drugs. An 87% generic dispense rate (GDR) is not good. It is below average. An 80% or higher prior authorization approval rate is not good either. In fact, it is way too high. High PA approval rates don’t improve outcomes, but it does increase drug spending unnecessarily. Rebate credits reward PBMs for rubberstamping drug utilization management programs. Never forgo rebates for any reason including medical benefit drug rebates.

The PBM excludes claims with DAW codes 1, 3 or 5 from rebate eligibility. There is no reason on god’s green earth for these claims to be excluded other than the PBM taking financial advantage of its client. DAW code exclusions are driven by PBMs who profit from an opaque revenue model.

The PBM does not provide claim (NDC) level reporting. A Rebate Remittance Summary Report is a summary of the total payments received from manufacturers, on a per client basis, which includes the total allocations for these payments, NDC, pharmacy identifier, claim number, fill date, and plan identification. The information in this report will reflect the guarantee and payment received on each specific claim.

The PBM service agreement ought to incorporate year-over-year increments on rebate or refund rates. This increment will assist with guaranteeing that your agreement is working every year. When long-term agreements are set up, it’s particularly vital to increase rebate rates every year to adjust for inflation and provide price protection. One more method for tending to this yearly rebate rate increment is through a market check. The market check helps to ensure you are getting the best rates year-over-year. In a perfect world, you would incorporate both the year-over-year increments of rebate rates, as well as an annual market check provision in the PBM service agreement.

Conclusion – 6 Indicators Your PBM is Hoarding Rebates

The Lehigh County Controller’s Office reviewed Lehigh County’s prescription drug plan which lost savings of almost $1.4 million, while battling a lack of transparency and openness about drug costs[i]. Lehigh County elected to choose a fixed discount structure, meaning that it received a flat rate savings for each employee on its healthcare plan. Lehigh County is self-insured. It could have elected to take full rebate value which results from savings passed from the pharmaceutical company to the pharmacy benefit manager but chose not to do this. In 2019, Lehigh County found that the actual rebate value exceeded the fixed discount by $700,000. The Controller’s Office also identified $654,749 in potential drug cost savings through a market check.

Bloomberg Law writes, “among employers’ concerns are a lack of transparency into whether PBMs are fully refunding rebates and discounts negotiated with drug manufacturers; how PBMs profit from manufacturer discounts; and whether they are including expensive drugs on formularies to increase their own profits.” It seems Bloomberg Law and Lehigh County have a lot in common.

[i] Siegel. J. 2021, January 29. Lehigh County Controller Takes on Highmark Health Insurance. PR Newswire. https://www.prnewswire.com/news-releases/lehigh-county-controller-takes-on-highmark-health-insurance-301218070.html.

4 PBM Trends to Watch — And, Yes, Transparency is One of Them and other notes from around the interweb:

4 PBM Trends to Watch — And, Yes, Transparency is One of Them. The industry’s tradition of conducting complicated reviews of a year of claims and drug spend and advice to clients based on those copious reports needs to change to one that uses software and automation to review claims (and rebates) in near real time. Continuous Monitoring or CM identifies performance issues before they get out of hand. Audits typically occur 12 – 24 months after the fact which is too late to recoup most of any potential overpayments. Continuous Monitoring on the other hand, catches and resolves overpayments or other issues much faster.

Six Things to Look Out for Within the Rebates Section of Your Pharmacy Benefit Management Contract. Prior to signing your Pharmacy Benefit Management (PBM) contract, it’s essential to pay particularly close attention to the pharmacy services that provide cost-containment strategies. One vital component you should focus on is the rebate administration. Today, we are sharing six areas within the rebate section of your PBM contract, to help you maximize savings and mitigate risk.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

3 reasons why owning pharmacy benefits data matters. The Federal Trade Commission is pushing PBMs for greater transparency to help employers take control of their prescription costs. But what is transparency without access to plan data or performance analytics? Currently, employers are disempowered because too many don’t own their data, must pay extra to get access to what should already be theirs, or only receive partial access. These PBM practices of obscuring data have led to significant distrust from all stakeholders. To fix a broken system, the data being hidden by these third parties needs to be freed to provide employers and plan members with the information they need to find the path to lower costs.

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

Is self-funding the solution to growing medical and drug costs and other notes from around the interweb:

Is self-funding the solution to growing medical and drug costs? So, is self-funding the solution? First, let’s debunk the myths about self-funding and examine its advantages and disadvantages to determine whether it is right for your organization. Self-funding, especially for smaller organizations, is more common than most employers think. According to Kaiser Family Foundation, in 2020, 23% of employers with two to 199 plan participants were self-funded. From 100 – 199 plan participants, the percentage of employers that were self-funded grew significantly and from 200 – 1,000 participants, nearly 60% of employers were self-funded. Still, many smaller organizations with fewer than 200 employees believe they can’t self-fund because they don’t have a large enough group. Employers with at least 100 participants typically have enough data to make educated decisions around their funding and can have more opportunities for savings.

Six Things to Look Out for Within the Rebates Section of Your Pharmacy Benefit Management Contract. Prior to signing your Pharmacy Benefit Management (PBM) contract, it’s essential to pay particularly close attention to the pharmacy services that provide cost-containment strategies. One vital component you should focus on is the rebate administration. Today, we are sharing six areas within the rebate section of your PBM contract, to help you maximize savings and mitigate risk.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

Newly launched U.S. drugs head toward record-high prices in 2022. Drugmakers are launching new medicines at record-high prices this year, a Reuters analysis has found. The median annual price of 13 novel drugs approved for chronic conditions by the U.S. Food and Drug Administration so far this year is $257,000, Reuters found. They were in good company: seven other newly launched drugs were priced above $200,000. Three other drugs launched in 2022 are used only intermittently and were not included in the calculation. Last year, the median annual price rose to $180,000 for the 30 drugs first marketed through mid-July 2021, according to a study published recently in JAMA. While the Reuters tally does not completely replicate the work of that study, it shows that the direction of new drug prices continues to be on the rise.

This document is updated weekly, but why is it important? Healthcare marketers are aggressively pursuing new revenue streams to augment lower reimbursements provided under PPACA. Prescription drugs, particularly specialty, are key drivers in the growth strategies of PBMs, TPAs, and MCOs pursuant to health care reform.

How to Determine if Your Company [or Client] is Overpaying

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list.

Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions.

Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our acquisition costs then determine if a problem exists. When there is more than a 5% price differential for brand drugs or 25% (paid versus actual cost) for generic drugs we consider this a potential problem thus further investigation is warranted.

Multiple price differential discoveries mean that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

Once all bids are collected the consultant then plugs them into their in-house Excel spreadsheet or a third-party bid analyzer software platform. This is where the problems begin more on that in a bit.

Once all bids are collected the consultant then plugs them into their in-house Excel spreadsheet or a third-party bid analyzer software platform. This is where the problems begin more on that in a bit.