The Definition of Oversee: to watch over and direct (an undertaking, a group of workers, etc.) in order to ensure a satisfactory outcome or performance.

I could go on, but you get the idea. Kick back, increase the playback speed to 1.5x or 2x and watch as I go into detail about PBM revenue streams. To learn more about bad PBM revenue streams, join the next Certified Pharmacy Benefits Specialist course. It starts on January 12, 2023!

Only three online courses per year!

The Certified Pharmacy Benefits Specialist (CPBS) program offers three different instructional formats: live online classrooms, in-person Knowledge Camps, and self-study. Every Thursday at 6 PM ET, the online class meets for roughly 1.5 hours. Every class is taped for later viewing. PBIA is approved by the Society for Human Resource Management (SHRM), HR Certification Institute (HRCI), American Council of Pharmacy Education (ACPE), and forty-six states to provide up to 20 recertification credit hours to licensed pharmacists, pharmacy technicians, life and health professionals, and human resources specialists. Since we began offering our courses in 2014, more than 1,000 students have earned the CPBS credential.

“Thanks for everything throughout the course. The firm I work for is trying to get more involved in the Plan Sponsor space, and in doing so, we have been reviewing a lot of PBM/Plan Sponsor contracts. I can’t tell you how much more confident and comfortable I am working through these PBM contracts now and what I need to be looking out for.” – Adam Farkas, Esq. Associate Attorney

Because plan sponsors don’t know how to calculate how much money pharmacy benefit managers (PBM) make, it gives PBMs all the incentive they need to overcharge. How many businesses do you know want to cut their revenues in half? That’s why traditional pharmacy benefit managers, and their stakeholders, don’t offer a fiduciary standard of care and instead opt for hidden cash flow opportunities to generate their service fees. Want to learn more?

“Thank you, Tyrone, for this informative meeting.” David Wachtel, VP

“…Great presentation! I had our two partners at the presentation as well. Very informative.” Nolan Waterfall, Agent/Benefits Specialist

A snapshot of what you will learn during this 30-minute webinar:

Hidden cash flows in the PBM Industry

Basic to intermediate level PBM terminologies

Specialty pharmacy cost-containment strategies

Examples of drugs that you might be covering that are costing you

The #1 metric to measure when evaluating PBM proposals

Understanding how PBMs make money and how much you pay them for their services is a key element in running an efficient pharmacy benefits program. Join us to learn more.

Get ready for hemophilia gene therapies at $2M-$3M and other notes from around the interweb:

ERISA-Covered Companies Must Disclose Health Plan Costs. Starting in 2022, an estimated 2.5 million employer-sponsors of health plans are required to adopt new fee and pricing transparencies due to amendments made to ERISA. While ERISA has focused on retirement service fees in the past, the spotlight is now on healthcare costs. The requirements fall under the Affordable Care Act (ACA) and Consolidated Appropriations Act, 2021 (CAA 2021), and affect organizations covered by the Employment Retirement Income Security Act of 1974 (ERISA). ERISA applies to most private companies that offer healthcare and retirement plans to employees. Complying with ERISA fiduciary duties for group health plans has been challenging due to the lack of fee transparency in the industry. However, the new transparency rules put more fee and pricing information into the hands of health plan fiduciaries and other stakeholders to shed light on these fees.

4 questions to ask before signing your next PBM service agreement. The very idea of managing pharmacy benefits might make you nauseous. That’s because drug prices are skyrocketing, creating significant challenges for your company’s bottom line. You may think that your pharmacy benefit manager (or PBM) – who is responsible for handling contractual relationships between drug manufacturers, health insurance providers, pharmacies, and patients – would negotiate the best possible deals for everyone involved. Unfortunately, recent reports from the PBM Accountability Project show otherwise: PBMs often misuse their immense power by adding secret streams of revenue for themselves. The Federal Trade Commission (FTC) has noted this trend too and announced plans in 2022 to investigate the inner workings of PBMs. But some states are taking it upon themselves to crack down on PBM business dealings, too. For example, Florida and Iowa joined Michigan in passing legislation in 2022 that regulates certain PBM practices – while Ohio’s Medicaid department is also conducting audits.

Payers and PBMs are restricting access to birth control options, report finds. Several large health insurers and pharmacy benefit managers (PBM) are limiting access to birth control medication, according to a report issued by the House Oversight and Reform Committee this week. There are more than 30 birth control products that health insurers and pharmacy benefit managers are placing cost-sharing requirements on, the report found. In other words, these healthcare stakeholders are making patients pay to cover part of the prescription drug cost — or else restricting coverage. The Affordable Care Act (ACA) requires that private health insurance plans cover birth control options that are approved by the Food and Drug Administration without asking for copays. Among the 34 birth control products identified in the report, 12 don’t have equivalent options on the market.

Get ready for hemophilia gene therapies at $2M-$3M. ICER says it’s fair for BioMarin and CSL to price incoming hemophilia gene therapies at $2M-$3M. Get ready for million-plus-dollar gene therapies to become the norm rather than the exception, and in some cases, the Boston-based drug pricing watchdog ICER is coming on board. The nonprofit ICER (Institute for Clinical and Economic Review) on Wednesday unveiled a new report finding that CSL Behring’s potential gene therapy etranacogene dezaparvovec for hemophilia B, which is due for an FDA approval decision by the end of this month, could be priced at around $3 million. ICER also updated its previous assessment of BioMarin’s EU-authorized hemophilia A gene therapy Roctavian, which ICER said could be fairly priced at about $2 million. “The new gene therapies can result in successfully treated patients appearing ‘cured’ for at least a period of time,” ICER chief medical officer David Rind said in a statement. “During this period, these gene therapies will eliminate the need for expensive prophylactic treatment. However, the duration of this ‘cure’ and the safety of therapies remains important uncertainties.”

In addition to 6 things every transparent PBM should do, PBM duties may include creating retail pharmacy networks, maintaining drug formularies, claims adjudication, and negotiating rebates with drug manufacturers. To help health insurance control drug costs, PBMs were developed in the 1960s. By moving demand among rival replacement medications, PBMs can encourage price competition among prescription drugmakers.

Manufacturers also provide rebates to PBMs in exchange for having their medications included favorably on a pharmacy formulary. PBMs then pass these rebates on to insurance or employers. For rebates to truly benefit final consumers, the PBM industry must be transparent [i].

6 Things Every Transparent PBM Should Do:

Provide unrestricted access to claims data. Unions, health plans, health systems, commercial and public sector employers shouldn’t get any push back when requesting claims data. Minimum data elements include NDC, date dispensed, quantity, days’ supply, and pharmacy identifier (i.e., NABP, NCDPD or NPI).

Allow clients to terminate, for any reason, with 90 days’ notice. Opaque pharmacy benefit managers are unwilling to sacrifice revenue streams that are bad for customers. Terminating one of these deals early requires an act of congress.

Lower the copayment to match the total cost of the drug. Prescription drug overpayments (also known as “clawbacks”) occur when commercially insured patients’ copayments exceed the total cost of the drug to their insurer or pharmacy benefit manager[ii].

Disclose or not take spreads. A spread is the difference between what a PBM takes in (cash) and the amount it pays out. Therefore, spreads occur with ingredient cost and rebates. Spreads are harmful when third-party payers are unaware or unable to perform a full accounting of the total amount of spread being paid.

Deliver a 90% or better generic dispense rate (GDR). High GDRs are driven primarily by cost-effective formulary and drug utilization management programs.

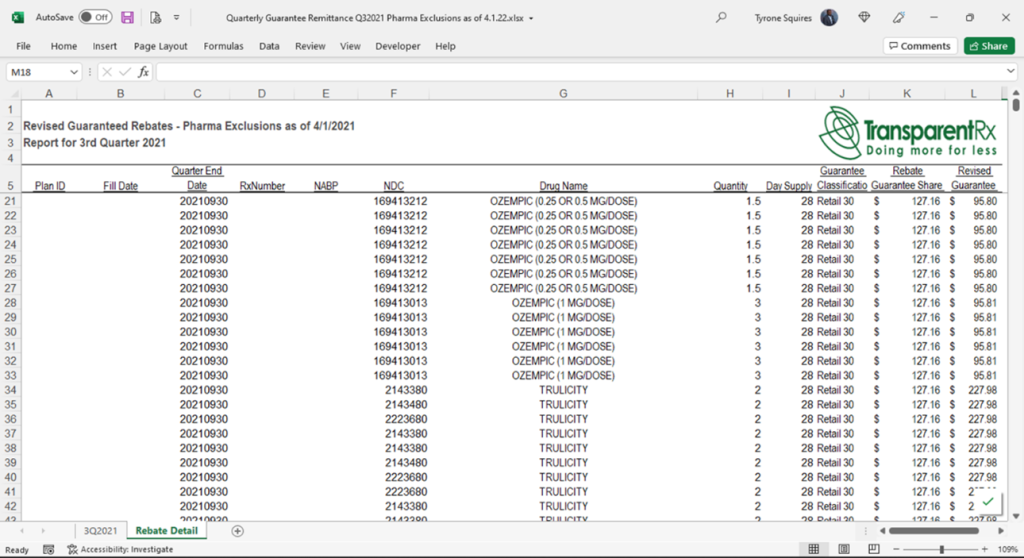

Provide every client with a rebate remittance report. A rebate remittance report is like a claims file with two additional data elements; rebate guarantee amount and rebate amount collected. Rebate remittance reports allow plan sponsors to compare notes.

Sample Rebate Remittance Report

5 Things Every Transparent PBM Should Do

What PBMs are (completely) passing on in rebates and network discounts is unclear. In fact, some economists contend that the PBM market’s consolidation and opaque pricing are two factors contributing to rising pharmaceutical prices. Health insurers have started vertically integrating with PBMs, in reaction to this insufficient pass-through of rebates. Because of this, the biggest insurers in the nation as well as several smaller ones already own their own PBMs or share an owner with one.

How the 10 largest PBMs hold huge sway in health care marketplace and other notes from around the interweb:

How the 10 largest PBMs hold huge sway in health care marketplace. The American Medical Association has gathered first-of-its-kind data on pharmacy benefit managers (PBMs) and its analysis finds a widespread high degree of market concentration in local markets across the U.S. where PBMs provide services to commercial health insurers. The AMA Policy Research Perspectives report, “Competition in Commercial PBM Markets and Vertical Integration of Health Insurers with PBMs” (PDF) presents the two largest PBM market shares and concentration levels for all states and metropolitan areas. The analysis found that 37% of the national markets for two services—formulary management and benefit design—were managed in-house by health insurers rather than buying those services from the PBM market. Commercial insurers largely use a PBM for three services—rebate negotiation, retail network management and claims adjudication—rather than conducting them in-house, which is why the report assesses market competition for those three PBM services.

4 questions to ask before signing your next PBM service agreement. The very idea of managing pharmacy benefits might make you nauseous. That’s because drug prices are skyrocketing, creating significant challenges for your company’s bottom line. You may think that your pharmacy benefit manager (or PBM) – who is responsible for handling contractual relationships between drug manufacturers, health insurance providers, pharmacies, and patients – would negotiate the best possible deals for everyone involved. Unfortunately, recent reports from the PBM Accountability Project show otherwise: PBMs often misuse their immense power by adding secret streams of revenue for themselves. The Federal Trade Commission (FTC) has noted this trend too and announced plans in 2022 to investigate the inner workings of PBMs. But some states are taking it upon themselves to crack down on PBM business dealings, too. For example, Florida and Iowa joined Michigan in passing legislation in 2022 that regulates certain PBM practices – while Ohio’s Medicaid department is also conducting audits.

Payers and PBMs are restricting access to birth control options, report finds. Several large health insurers and pharmacy benefit managers (PBM) are limiting access to birth control medication, according to a report issued by the House Oversight and Reform Committee this week. There are more than 30 birth control products that health insurers and pharmacy benefit managers are placing cost-sharing requirements on, the report found. In other words, these healthcare stakeholders are making patients pay to cover part of the prescription drug cost — or else restricting coverage. The Affordable Care Act (ACA) requires that private health insurance plans cover birth control options that are approved by the Food and Drug Administration without asking for copays. Among the 34 birth control products identified in the report, 12 don’t have equivalent options on the market.

Kroger seeks to end deal with Cigna’s Express Scripts over drug pricing. Grocery retailer Kroger Co said on Friday it has sent Cigna Corp’s subsidiary Express Scripts a written notice of its plan to terminate their pharmacy provider agreement for commercial customers due to an “unsustainable” pricing model. Kroger said it has made several attempts since February to negotiate with the pharmacy benefit manager for a “more equitable and fair contract that lowers cost, increases access, and delivers greater transparency, but there has been little to no progress to date”. Kroger said more than 90% of Kroger Health’s customers will not be affected by a termination of the deal, but if a new agreement is not reached by Dec. 31, most Express Scripts’ commercial customers won’t be able to fill prescriptions at Kroger stores. Cigna bought Express Scripts in 2018 in a $54-billion deal, creating one of the biggest providers of pharmacy benefits and insurance plans in the United States.

3 Axis Advisors new report clears up misunderstandings about drug pricing benchmarks. The just released comprehensive report, Understanding Pharmacy Reimbursement Trends in Oregon makes general representations that are applicable to any state or group, not just Oregon.

Five key takeaways:

The drug price benchmark (i.e., AWP, NADAC, MAC etc.) used to determine a drug’s price does not matter when the PBM doesn’t take a spread.

An invisible floor exists on the reimbursement amount pharmacies are willing to accept

Then, what matters most is how close the billed (plan sponsor) amount gets to pharmacy reimbursement on a per claim basis

NADAC is compiled from a voluntary monthly invoice cost survey of 2,500 randomly selected retail pharmacies with 450-600 respondents.

Don’t forget to tack on the dispensing fee (page 29) when comparing NADAC to AWP minus for ingredient cost analysis

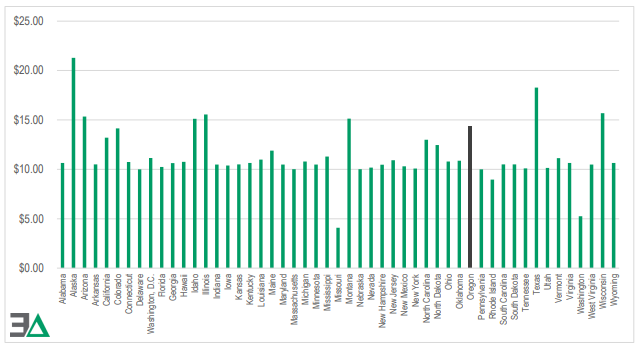

Medicaid Maximum Retail Dispensing Fees by State (2022)

Conclusion, New Report Clears Up Misunderstandings About Drug Pricing Benchmarks

This all assumes the PBM has negotiated aggressively with pharmacy networks. If not, all bets are off. The ability of a PBM to negotiate discounts and rebates varies with fire in the belly, experience, and education level of decision-makers sitting at the table.

New inflation-linked drug rebates have gone into effect and other notes from around the interweb:

4 questions to ask before signing your next PBM service agreement. The very idea of managing pharmacy benefits might make you nauseous. That’s because drug prices are skyrocketing, creating significant challenges for your company’s bottom line. You may think that your pharmacy benefit manager (or PBM) – who is responsible for handling contractual relationships between drug manufacturers, health insurance providers, pharmacies, and patients – would negotiate the best possible deals for everyone involved. Unfortunately, recent reports from the PBM Accountability Project show otherwise: PBMs often misuse their immense power by adding secret streams of revenue for themselves. The Federal Trade Commission (FTC) has noted this trend too and announced plans in 2022 to investigate the inner workings of PBMs. But some states are taking it upon themselves to crack down on PBM business dealings, too. For example, Florida and Iowa joined Michigan in passing legislation in 2022 that regulates certain PBM practices – while Ohio’s Medicaid department is also conducting audits.

New inflation-linked drug rebates have gone into effect. The new rebates are part of the newly signed Inflation Reduction Act, which introduces this new requirement that manufacturers pay rebates to Medicare for Part D drugs whose price increases exceed inflation, and in January 2023, the same will occur with Part B drugs. The rebate system “was designed to reduce the frequency and size of drug price increases,” HHS says. The IRA also includes a provision that allows CMS to negotiate and/or cap the prices of 10 of the most expensive drugs. While those negotiations will be limited, the rebates paid by the industry may be significant. HHS released a new report on Friday outlining what the IRA could do as more than 1,200 drug price increases from July 2021 to July 2022 exceeded the inflation rate of 8.5% for that time period. The report notes most price increases occur at the beginning of January, with more than 3000 drugs experiencing a price increase in 2022, up from 2650 in 2016. The number of July price increases trended downward from 613 NDCs in 2016 to 203 in 2021, but in July of 2022, the number of increases rose to a level similar to that observed in 2016, with 601 increases.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

Kroger seeks to end deal with Cigna’s Express Scripts over drug pricing. Grocery retailer Kroger Co said on Friday it has sent Cigna Corp’s subsidiary Express Scripts a written notice of its plan to terminate their pharmacy provider agreement for commercial customers due to an “unsustainable” pricing model. Kroger said it has made several attempts since February to negotiate with the pharmacy benefit manager for a “more equitable and fair contract that lowers cost, increases access, and delivers greater transparency, but there has been little to no progress to date”. Kroger said more than 90% of Kroger Health’s customers will not be affected by a termination of the deal, but if a new agreement is not reached by Dec. 31, most Express Scripts’ commercial customers won’t be able to fill prescriptions at Kroger stores. Cigna bought Express Scripts in 2018 in a $54-billion deal, creating one of the biggest providers of pharmacy benefits and insurance plans in the United States.

4 questions to ask before signing your next PBM service agreement and other notes from around the interweb:

4 questions to ask before signing your next PBM service agreement. The very idea of managing pharmacy benefits might make you nauseous. That’s because drug prices are skyrocketing, creating significant challenges for your company’s bottom line. You may think that your pharmacy benefit manager (or PBM) – who is responsible for handling contractual relationships between drug manufacturers, health insurance providers, pharmacies, and patients – would negotiate the best possible deals for everyone involved. Unfortunately, recent reports from the PBM Accountability Project show otherwise: PBMs often misuse their immense power by adding secret streams of revenue for themselves. The Federal Trade Commission (FTC) has noted this trend too and announced plans in 2022 to investigate the inner workings of PBMs. But some states are taking it upon themselves to crack down on PBM business dealings, too. For example, Florida and Iowa joined Michigan in passing legislation in 2022 that regulates certain PBM practices – while Ohio’s Medicaid department is also conducting audits.

Lawsuit Challenges Federal Copay Accumulator Policy. On August 30, 2022, a coalition led by the HIV and Hepatitis Policy Institute filed a new lawsuit in federal district court in DC to challenge a Trump-era policy that allows insurers and pharmacy benefit managers (PBMs) to not apply financial support from a drug manufacturer towards a patient’s deductible or annual out-of-pocket maximum. If an insurer or PBM adopts such a policy, the enrollee cannot “count” a copay or other drug manufacturer coupon—typically used to help reduce patient costs at the pharmacy counter—towards a patient’s overall annual out-of-pocket costs. This policy was adopted in May 2020 in the final 2021 notice of benefit and payment parameters and has not been altered since. More than two years later, the plaintiffs argue that this policy is unlawful because it conflicts with the Affordable Care Act (ACA), is inconsistent with other agency regulations, and is arbitrary and capricious under the Administrative Procedure Act. They ask the court to set aside this policy. The timing of the lawsuit may be designed to influence the forthcoming proposed 2024 notice of benefit and payment parameters, which is expected later this year.

How specialty drug ‘solution stacking’ can rein in pharmacy benefit costs. Brokers and employer groups alike know that 5% to 10% percent of insured workers and their dependents drive 50% to 60% of the cost of pharmacy claims. A few members with prescriptions for a specialty drug with a five-figure price tag can easily represent most of an entire group’s pharmacy spend. These drugs are often lifesaving or provide a dramatic quality of life improvement for those who take them. No one would question the necessity of using them. But when a group can mitigate some of the cost without affecting the clinical outcome, it can be a game changer. The broker who unlocks these savings becomes a trusted ally.

Senate Bill and FTC 6(b) Study Turn the Heat on Pharmacy Benefit Managers Amid Drug Pricing Concerns. Introduced on May 24, 2022, the Pharmacy Benefit Manager Transparency Act of 2022 is a bipartisan bill co-sponsored by Senators Maria Cantwell (D-WA) and Charles Grassley (R-IA) that imposes compulsory disclosure requirements on PBMs while seeking to limit certain controversial PBM practices such as spread pricing. The Act also empowers the FTC and state attorneys general to take enforcement action against PBMs that engage in “unfair and deceptive acts” or “dissemination of false information” related to PBM services. The proposed legislation expressly prohibits three types of controversial PBM activities that may be considered “unfair or deceptive,”4 including: (1) Charging a health plan or payer a different sum for a prescription drug’s ingredient cost or dispensing fee than the PBM reimburses a pharmacy for the prescription drug’s ingredient cost or dispensing fee, then retaining the difference as profit, a practice known as “spread pricing.”

My pharmacy background started with Eli Lilly & Company, a top twenty pharmaceutical manufacturer by sales. It was one of the best jobs I ever had and not just because of the perks. We talked a lot about helping patients get better which made me feel good about what I was doing. That being said, I’m not naive. We wanted to sell as much type 2 diabetes products as we could. To do that, we relied heavily on lax formulary and drug utilization management on the part of plan sponsors. Here are three underappreciated reasons for micromanaging pharmacy benefits.

Reason #1 – Drugmakers are making it easier to get access to high-cost specialty drugs

Prescription medicine is moving increasingly online with direct-to-consumer advertising by adopting a more assertive catchphrase: Talk to a doctor now. I haven’t checked every brand drug, but I suspect all of them have a dedicated website. These websites are now incorporating built-in buttons Talk to a Doctor Now for everything from sickle cell disease to migraine drug therapies. One communication about IBS or irritable bowel syndrome even reads, “you deserve to feel better.”

Reason #2 – PBMs too often permit high-cost brand drugs to be dispensed in place of lower cost generic equivalents

When plan sponsors forgo efficiency for participant satisfaction PBMs take financial advantage of the decision. High participant satisfaction usually means the patient getting the exact prescription drug, prescribed by the doctor, without any scrutiny. In my time with Eli Lilly, I took a territory ranked #600 to #11 in one year by persuading doctors to dispense a new type 2 diabetes brand drug (Actos) over a proven and much less costly generic Metformin. Actos provided no significant A1C improvements compared to metformin. A1C is the primary performance metric for antidiabetic agents. It is a simple blood test that measures average blood sugar levels. Below is an audio file (click the image) of a similar conversation between a PBM and broker. The president of a brokerage firm based in the south sent this to me. The PBM has forced Zytiga over its lower cost generic equivalent Abiraterone Acetate. My instincts tell me this PBM has a distribution deal for Zytiga. Depending upon the pharmacy, the retail price of brand Zytiga is easily 30x the generic version.

Reason #3 – One of the largest electronic prior authorization (ePA) companies in the world, CoverMyMeds, is owned by a drug wholesaler. Do I need to say more?

Three Underappreciated Reasons for Micromanaging Pharmacy Benefits Conclusion

Employers have been reluctant actors in the U.S. pharmacy distribution and reimbursement system, relying on third parties who may not have their best interests in mind. Some companies, like Honeywell and Caterpillar, have taken tough steps to control costs, with no loss in employee satisfaction. It is impossible to run an efficient pharmacy benefits management program without elements of micromanagement. Micromanagement in pharmacy benefits means every claim gets scrutinized with a focus on the lowest net cost. To minimize the impact of PBM, pharmaceutical manufacturer, and drug wholesaler efforts to pad their own pockets at employers’ expense, employ and measure the effectiveness of drug utilization management tools like step therapy, prior authorization, and mandatory generic enforcement programs. Oh, and don’t forget about DAW codes.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.