Internal Email Shows Big Three PBM Was Overcharging – And Knew It

Starting with its predecessor, a company called Catamaran that OptumRx acquired, the PBM administered prescription drugs for workers injured on the job. In all, OptumRx overcharged the bureau on more than 1.3 million claims for generic medications, the lawsuit says.

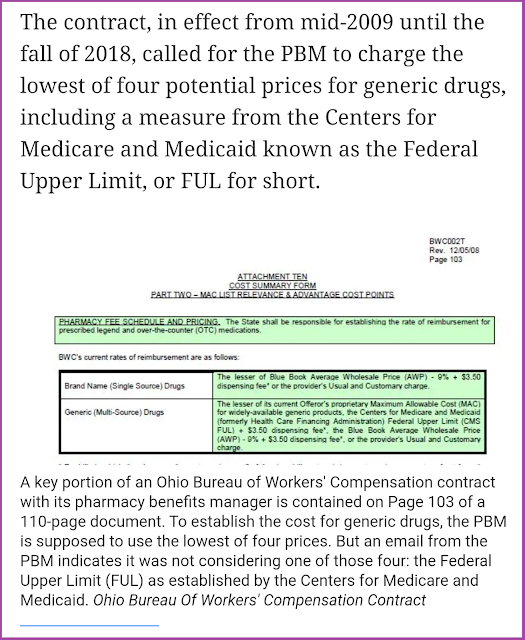

The contract, in effect from mid-2009 until the fall of 2018, called for the PBM to charge the lowest of four potential prices for generic drugs, including a measure from the Centers for Medicare and Medicaid known as the Federal Upper Limit, or FUL for short. But in a series of May 2015 emails marked as “confidential,” John Spankroy, Director of Public Sector Account Management for Catamaran, said the Federal Upper Limit was never applied, despite the contract.

|

| Click to Read Article |

Tyrone’s Commentary:

How does this go on for nearly a decade? Pharmacy Benefit Managers will provide transparency and

disclosure to a level demanded by the competitive market and generally rely on the demands of prospective clients for disclosure in negotiating their contracts. The best proponent of transparency is informed and sophisticated purchasers of PBM services. The purchaser needs to understand not only what they want to achieve in their relationship with their PBM but also the competitive market and their ability to drive disclosure of details on services important to them. Assessing transparency is done more effectively by a trained-eye with personal knowledge of the purchaser’s benefit and disclosure goals. The reason plan sponsors are overcharged is due to a gap you have in one or more of these areas:

1. Information Symmetry

2. PBM Industry Training

3. Lack of understanding in pharmacy benefit design or plan goals

Far too many brokers, PBM consultants, CFOs and HR executives are unfamiliar with the phrase “lesser of logic.” Worse yet, when given pricing sources such as AWP minus, MAC, U&C and Copayment 99% of decision-makers, who select a PBM vendor, can’t accurately calculate their own cost with lesser of logic. That’s why something like this can go on for a decade. It really just makes me sick to my stomach. It’s time to move on from the PBM, large or small, that puts profits over doing the right thing for their clients. Find a PBM partner who proactively corrects these “mistakes” for no other reason than it’s the right thing to do.

He told Susan McCreight, Senior Director of Public Sector Account Management, “Per BWC contract we are supposed to be using pricing logic that includes lower of FUL for generics. None of the BWC price schedules has FUL as a cost source.” In a separate email, Spankroy told Bryce Owens, the Illinois-based PBM’s manager for pricing and analytics, “We do not see FUL included as a cost source option.” Spankroy also acknowledged: “BWC is not aware of this (yet).”