Specialty Drug Costs Prompt Employers to Tighten Their Belts

A survey released last week by the National Business Group on Health found that benefit cost increases are expected to remain firm next year as a result of changes many employers are making to benefit plans. Meanwhile, almost half of the 140 large national employers surveyed indicated that if additional measures to control costs are not taken, at least one of their health plans will reach the benchmark that triggers the “Cadillac” excise tax under the Affordable Care Act in 2018.

“The need to control rising health care benefits costs has never been greater,” said Brian Marcotte, president and CEO of the National Business Group on Health. “Rising costs have plagued employers for many years, and now the looming excise tax is adding pressure. Employers only have 2 more years to bend the cost curve before the excise tax goes into effect in 2018. And while employers are pursuing several strategies to keep their plans under the excise tax threshold, they estimate their actions will only delay the impact by 2 to 3 years.”

The survey found that employers project health care benefit costs to increase 6% in 2016, which would mirror the increase employers would have seen this year if there were no changes made to their plan design. Many employers project increases to remain at 5% for the third consecutive year through these plan changes, which include greater cost-sharing provisions, the adoption of consumer-directed health plans (CDHPs), and increased wellness initiatives.

The survey found that by 2020, nearly 72% of employers anticipate one of their plans to trigger the excise tax, as the benefit plan with the greatest enrollment could only lag one year behind. To delay the impact of the excise tax, 76% of employers said they will add or expand CDHPs and consumerism tools, with 70% stating they will expand current wellness programs.

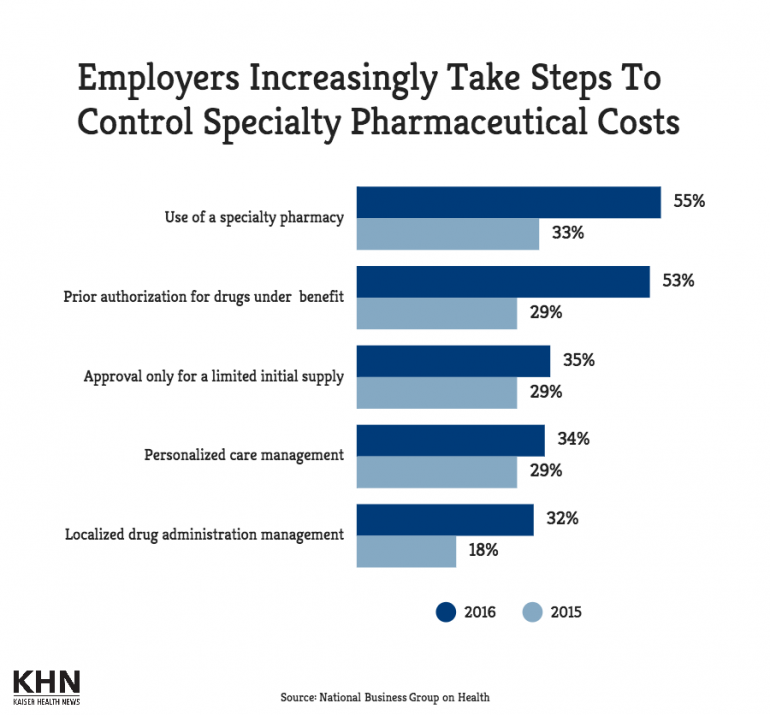

The survey results showed that for 43% of employers, the top driver of rising health care costs is high cost claimants. Meanwhile, the growing cost of specialty pharmacy, specific diseases or conditions, and overall medical inflation were also implicated for spending increases.

None of the employers said they plan to eliminate health care coverage and pay the penalty for it, but some indicated they will continue to examine whether private exchanges are viable. By the end of 2015, 3% of employers will have moved active employees to a private exchange, the study noted.

– See more at: http://www.specialtypharmacytimes.com/news/specialty-drug-costs-prompt-employers-to-tighten-their-belts#sthash.0yfRbyBl.dpuf