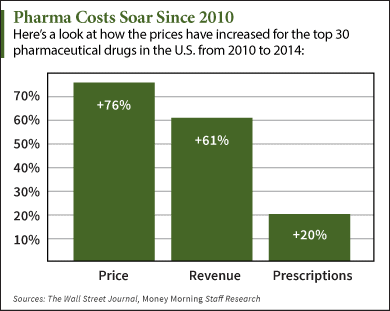

Pharmacy costs is one of the fastest-growing components of health care expense and is expected to increase by 15% per annum with no end in sight. It is estimated that 75% of employers plan to increase prescription drug spend year-over-year. Unfortunately, most organizations are unaware of their excessive remuneration for PBM services. While there is no magic pill to managing the pharmacy benefit, the following five key performance indicators can help to identify a path to lower pharmacy costs while still improving member outcomes.

Dump the Legacy RFP (Request for Proposal) Process. Employers must instead create their own airtight fiduciary contract and put it out for bid vis-à-vis reverse auction. How is it that a plan sponsor, regardless of size, can sign a deal which doesn’t hold its PBM accountable to a client-comes-first standard of care?

from Wikipedia…

“A fiduciary is someone who has undertaken to act for and on behalf of another in a particular matter in circumstances which give rise to a relationship of trust and confidence. A fiduciary duty is the highest standard of care at either equity or law. A fiduciary is expected to be extremely loyal to the person to whom he owes the duty (the “principal”): he must not put his personal interests before the duty, and must not profit from his position as a fiduciary, unless the principal consents.”

Case closed.

Promote Limited (Preferred) Pharmacy Networks. Most plans offer access to more than 60,000 retail pharmacies nationwide. The reality is that at any given street intersection 3 of the 4 corners are filled with pharmacies including CVS, Rite-Aid, Walgreens or others. Instead of allowing access to countless options, an employer can save 2 percent or more by narrowing the number of network pharmacies.

After cost-sharing, establishing preferred pharmacy networks has been a popular approach to cost management. Limited pharmacy networks, not talked of much before 2010, are much more of a consideration after the contract dispute between Walgreens and Express Scripts.

Providing the broadest access to members may no longer trump the more favorable pricing of a narrowed pharmacy network. A large and growing supply of retail pharmacies makes the limited pharmacy network approach possible.

Caveat emptor. Ballooning is a black box tactic whereby one PBM profit center drives an unusual amount of fees when another is being squeezed. It turns out payers’ cost for mail pharmacy services may increase, when a limited pharmacy network is selected, to offset the negotiated retail pharmacy network.

Implement Specialty Therapy Management. We know specialty therapies improve outcomes but we also know patients do not take medications the way they should, or in the way it was studied to produce published results. Disease specific algorithms enable us to:

- Ensure standards of care are consistently followed thereby reducing waste

- Monitor therapy to detect and resolve problems; identify opportunities for referral to MTM, PFA or clinics

- Pro-actively identify opportunities to keep patients on therapy

- Help patients become better informed about their therapy so they can more actively take charge of it

All of these initiatives either improve outcomes, reduce re-admissions or prevent emergency room visits which in turn lowers overall medical costs.

Keep Two Sets of Eyes on Your PBM. A key strategy to controlling prescription drug benefit costs is to understand and better manage the relationship with your pharmacy benefits manager (PBM). Given the complexity of prescription drug benefit programs, it is an attractive option to simply turn over management of the employee prescription drug benefit to a consultant, ASO, PBM or TPA.

However, it is important to realize that while they are serving clients’ needs, PBMs and TPAs are also in business to make a profit. Therefore, the actions that they take may not always be in the best interest of an employer. For that reason and others, employers are increasingly attempting to better understand the prescription drug benefit in order to develop new strategies to control costs and to maintain an affordable, quality drug plan for their employees.

Because more benefit dollars are shifting from medical to prescription drugs every year, payers whom have internal expertise in pharmacy are in a better position to assume greater control of their prescription drug benefit thereby reducing costs while improving patient outcomes.

Utilization of Internal Pharmacies or Reference Pricing. To illustrate this point I use the story of Meridian Health Systems, a former customer of Express Scripts, to show the sometimes drastic difference in what PBMs charge payers to fill prescriptions and what they in turn pay pharmacies to dispense those same prescriptions. This difference often leads to greater profits for the PBM and increased costs for the employer.

Robert Schenk, who oversees Meridian’s spending on employee medications, dug through the employer’s bills to discover just how pervasive the practice was. One such example he found were charges for generic amoxicillin — Meridian was billed $92.53 when an employee filled the prescription, but Express Scripts paid only $26.91 to the pharmacy to fill the same prescription.

That amounts to a “spread” of $65.62 for only one prescription. In another instance, Meridian was billed $26.87 for a prescription of the antibiotic azithromycin. Express Scripts paid the pharmacy $5.19 to dispense the prescription, creating a spread of $21.68.

As this practice persisted, Meridian’s health benefits costs skyrocketed, all while Express Scripts continually promised savings. In the first year alone, Meridian’s prescription benefits costs increased by $1.3 million. It wasn’t long before Meridian switched to a more transparent PBM to handle their prescription benefits.

The only reason Meridian Health was able to identify the spread is due to the reference pricing or pharmacy it owned. In this case, Meridian Health acted as the middle man and was able to see both sides of the transaction. Imagine for a moment, as a payer, how powerful this tool can be. There are fiduciary PBMs willing to give clients access to the same information from which Meridian Health was able to benefit. I suggest you locate one.

To read more of Meridian Health System’s story click here.