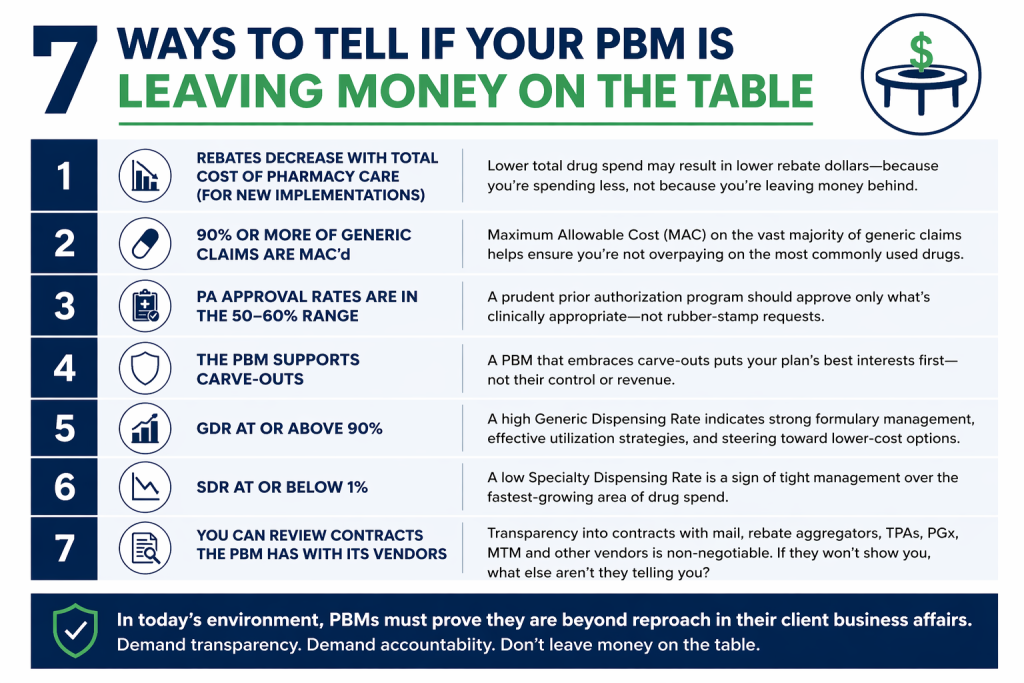

I Asked ChatGPT to Score Our PBA Services Agreement and Was Surprised by What I Learned

I recently asked ChatGPT to score our pharmacy benefit administrator (PBA) services agreement on how much control and transparency it gives self-funded employers. Here was the prompt: “Act as an ERISA attorney and pharmacy benefits expert. Score the attached contract on a scale of 1 to 10 on how much control and transparency it provides to self-funded employers.” The score came back 9.6 out of 10. Skeptical? Good. You should be.

In pharmacy benefits, big transparency claims deserve pressure testing. So call my bluff. Ask for the agreement. Read the audit clause. Review the rebate language. Look at who controls the formulary, specialty pharmacy arrangements, network strategy, data access, and plan economics.

Then do the same with your current PBM or PBA agreement. Use the same prompt. Pressure test the contract you already have in place. The answer may show whether your agreement gives the plan sponsor enforceable control, or whether it relies too heavily on vendor promises. What surprised me was not the score itself. It was how much the score changed when the contract posture changed.

Prompt: Act as an ERISA attorney and pharmacy benefits expert. Score the attached contract on a scale of 1 to 10 on how much control and transparency it provides to self-funded employers.

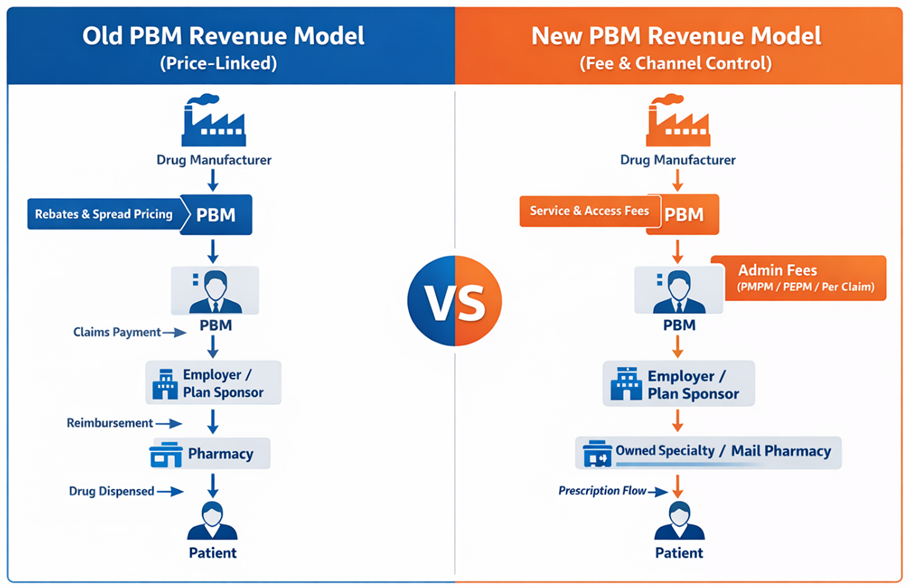

The existing version, built around a fiduciary pharmacy benefit administrator model, scored 9.6 out of 10. The reason was straightforward. The agreement gave the employer final authority over plan design, formulary, utilization management, pharmacy network decisions, manufacturer contracting, rebate strategy, and coverage policy. TransparentRx did not have discretionary authority over those decisions. It also included broad audit rights, pass-through economics, specialty compensation disclosure, and client ownership of plan-attributable rebates, credits, discounts, fees, and other financial benefits.

Then I asked a different question: what happens if the fiduciary language is removed and the contract describes the company as a pharmacy benefit manager instead of an administrator?

The score dropped to roughly 7.2 out of 10. That is not a cosmetic change. It affects money, oversight, and CAA documentation. Contract posture has financial and compliance consequences. If an agreement reads like a conventional PBM contract, the employer may lose leverage over the very items that determine whether the plan is truly being managed in its best interest:

- Rebate strategy and whether all plan-attributable rebates are disclosed, reconciled, and returned.

- Specialty pharmacy economics, including margins, referral arrangements, data fees, service fees, and affiliate relationships.

- Audit access to claims-level data, pharmacy reimbursement records, MAC list application, manufacturer payments, aggregator records, and subcontractor compensation.

- CAA RxDC reporting at the plan level, not just the vendor’s aggregate book of business. Aggregate reporting may help a vendor complete a filing, but it does not give the employer enough visibility to verify its own prescription drug spend, rebates, high-cost drugs, top drugs, member cost-sharing, or vendor compensation. Plan-level reporting ties the data back to the employer’s actual claims experience, which is what fiduciaries need for cost oversight, renewal decisions, rebate reconciliation, and CAA documentation.

- Fiduciary documentation. A weaker contract can make it harder for the plan sponsor to show it had the contractual right to obtain, review, and verify the financial data behind pharmacy spend.

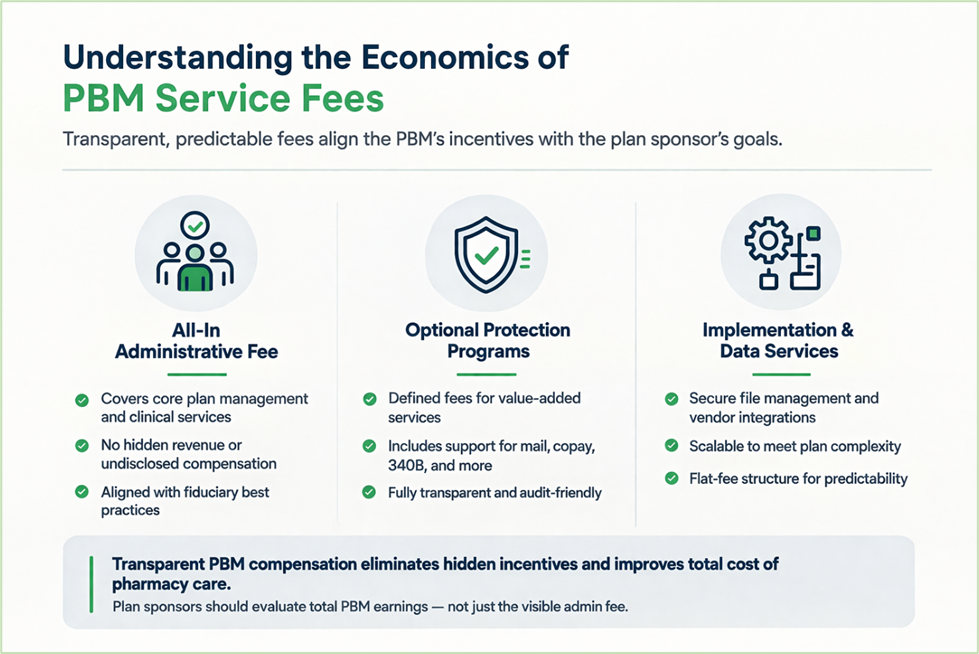

Transparency is not meaningless. It is essential, but it has to be enforceable.

A vendor can say it is transparent, but the contract must give the plan sponsor the right to obtain, audit, reconcile, and use the data needed to manage the plan, verify financial performance, and meet reporting obligations. In pharmacy benefits, transparency without contractual rights is just a talking point.

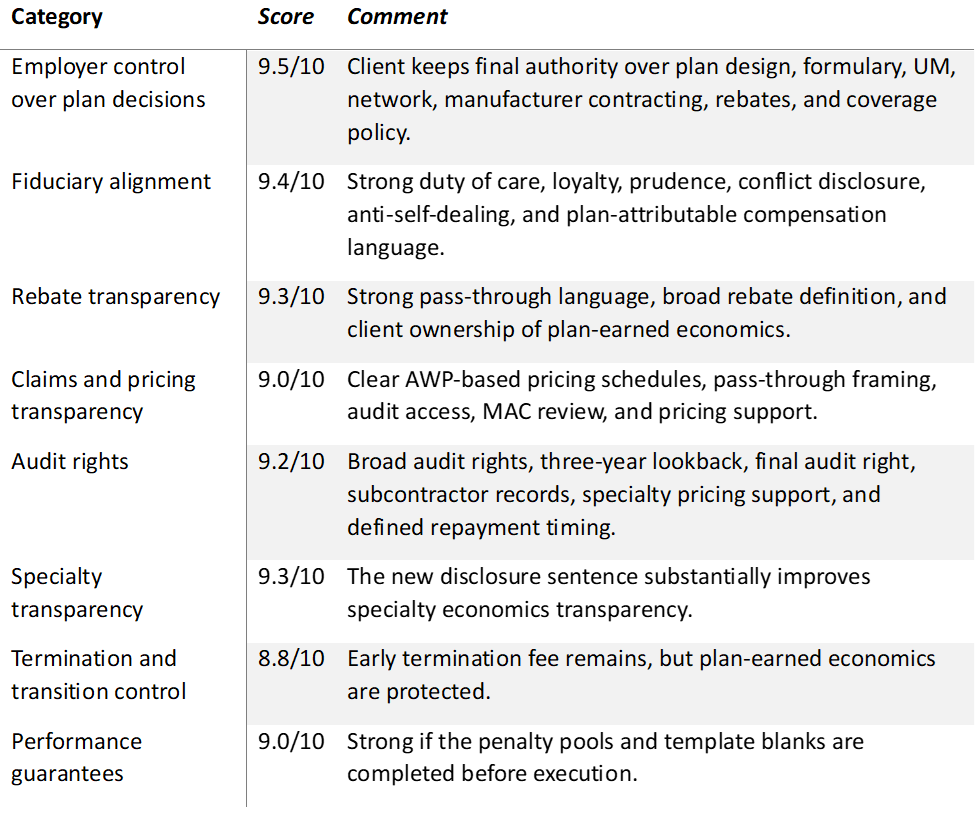

Here is the scorecard under the existing service agreement:

The lesson is simple: contract labels matter, but contract authority matters more.

A self-funded employer should know exactly where control sits. That means knowing who controls the plan, formulary, rebate strategy, and pharmacy network. It also means knowing who owns the data, who can audit the financial flows, and who receives every dollar tied to the plan.

Brokers, consultants, and Benefit Directors should not stop at “transparent PBM” language. Ask for the agreement. Read the audit clause. Review rebate ownership. Check specialty compensation. Confirm who has final decision-making authority. Then ask one direct question: does this agreement give the plan sponsor enforceable control, or does it leave the employer relying on vendor promises?

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM.