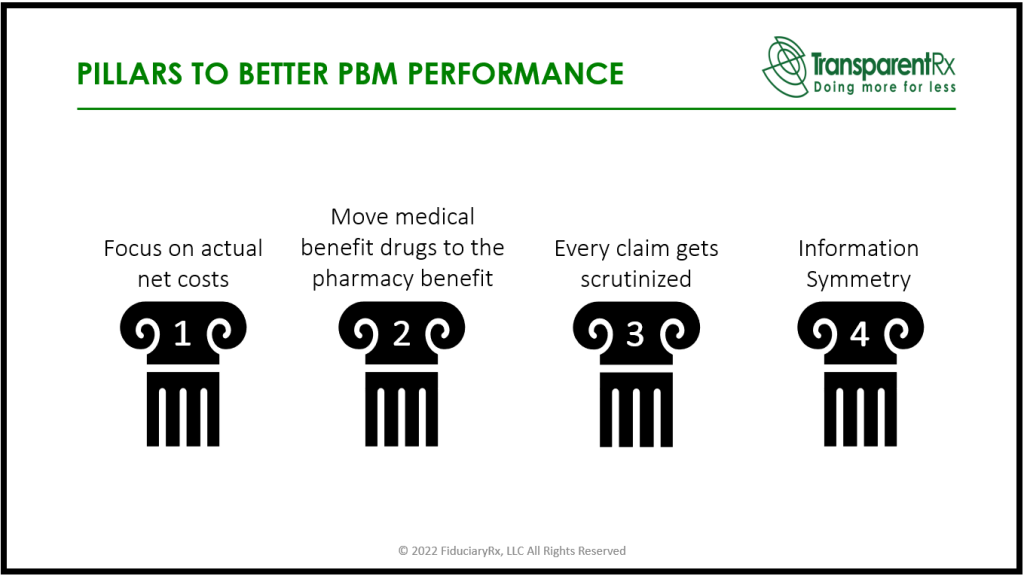

5 Things To Do Immediately About Drivers Of Pharmacy Costs

PBM selection decisions often boil down to price. It’s a common mistake as the actual cost of PBM services encompasses more than just price. There are four primary drivers of pharmacy cost price being the most obvious. Equally important drivers of pharmacy cost include product mix, utilization, and cost share. Let’s take an in-depth look at 5 things to do immediately about drivers of pharmacy costs.

Price

Contract nomenclature sets the foundation for prices in a pharmacy benefit management agreement. Without the constituent elements being spelled out, a fiduciary standard of care or radical transparency, pricing proposals are almost worthless. The price an employer pays for a prescription drug claim includes several components such as list prices, contractual discounts, acquisition costs, administrative fees, and rebates, for example.

Price receives a lot of attention deservedly so. However, far too little attention is being paid to what matters most, which is the final plan cost. A substantial chunk of what an employer pays for its pharmacy benefit is attributed to how well the PBM performs clinically. Clinical effectiveness can easily be the difference between underperformance or overperformance in a pharmacy benefit program.

Product Mix

Product Mix refers to the complete range of products that is offered for dispensation by a pharmacy. In other words, small molecule brand and generic, specialty including biologic and biosimilar drugs make up product mix. The formulary, and adherence to it, is the key determinant of product mix. Everyone knows that generic drugs are far less costly compared to brand drugs. But, did you know that for every 1% increase in GDR or generic dispense rate an employer can expect as much as a 2.5% decrease in gross ingredient costs[i]?

A non-fiduciary PBM is counting on its clients not knowing or caring about how GDR impacts cost and that you will be mesmerized by the optics of large rebates or discount guarantees. GDRs, which hover in the 80% – 86% range, are too low and costly. The non-fiduciary PBM benefits from its share of rebates on brand drugs that never should have been dispensed in the first place. Without exception the most heavily advertised and rebated drugs have therapeutic alternatives which cost up to 90% less than the rebated products.

Not only is the non-fiduciary PBM counting on you being mesmerized by artificially high discounts and rebates, but it is also counting on you not placing a dollar value on poor product mix. A pharmacy benefit manager’s (or PBM) essential job ought to be uncomplicated: act in the best interest of patients and clients while delivering lowest net cost. Instead, non-fiduciary PBMs are leveraging information failure to their financial advantage[ii].

Utilization

Contrary to mainstream opinion, utilization has little to do with the number of prescription drug claims being paid. Drug manufacturers concern themselves more with days’ supply and from which sites drugs are being dispensed. Hence, drug utilization consists of the number of utilizers, days’ supply, and channel mix (i.e. retail vs. mail). The tools being used to manage utilization are plentiful. They include but are not limited to:

- Formulary Exclusions

- Refill too soon

- Quantity Limits

- Prior Authorization (PA)

- Step Therapy (ST)

- Mandatory Generic Enforcement

- Pill Splitting

- Drug Utilization Review

- Dose Optimization

- Therapeutic Substitution

Utilization and Product Mix are part of PBM clinical programs. A PBM who performs well clinically will have a GDR at or above 90% and a generic substitution rate (GSR) above 97.5%. Just a couple of percentage points below these thresholds will lead to significant wasteful spending and an increase in PMPM cost. If you want to know if your PA or ST programs are working properly, just look at your GDR and GSR. Both are standard performance metrics upon which pharmacy benefit managers are routinely evaluated.

Cost Share

Cost Sharing or Cost Shifting is the members share of pharmacy costs which is addressed through mechanisms such as copayments, coinsurance, deductibles, and out-of-pocket limits. Recently, patients are being left poorer, not by accident or computer glitches, but by intentional acts.

A copay accumulator – or accumulator adjustment program – is a strategy used by insurance companies and pharmacy benefit managers (PBMs) that stop manufacturer copay assistance coupons from counting towards two costs: 1) the deductible and 2) the maximum out-of-pocket spending. PBMs should not profit from cost-sharing assistance programs that are intended solely to benefit patients.

Drug manufacturers have made it clear their cost-sharing assistance programs were not created to drive profit for PBMs. As drug manufacturers attempt to create programs to subsidize out-of-pocket cost for patients, the payers reduce the value of these programs by exhausting such funds while also requiring the patients to pay their deductibles and coinsurance up to their out-of-pockets to obtain their medications.

It just doesn’t make sense to me that PBMs, insurers, and third-party payers (e.g., self-insured employers) point the finger at manufacturers of high-cost medications only to turnaround and siphon the cost-sharing assistance that the manufacturer provided to the patient away from counting toward deductibles or out-of-pocket maximums. This is especially harmful when there is no low-cost therapeutic alternative for high-cost formulary drugs.

Conclusion – 5 Things To Do Immediately About Drivers Of Pharmacy Costs

Pharmacy Benefit Managers provide transparency and disclosure to a level demanded by the competitive market and rely on the demands of prospective clients for disclosure in negotiating their contracts. The best proponent of transparency is informed and sophisticated purchasers of PBM services. Here are 5 things to do immediately about drivers of pharmacy costs:

- Get your GDR above 90%

- Eliminate accumulator programs

- Continuously monitor your GSR to reach 97.5% of better

- Employers and consulting firms alike must have skilled staff with extensive PBM knowledge

- Sign PBM contracts which have no loopholes

Without #4, #5 is impossible to achieve unless you work with a fiduciary pharmacy benefit management company. In fact, 1 through 5 requires you to work with the right PBM partner.

[i] Liberman, Roebuck, “Prescription drug costs and the generic dispensing ratio”, National Library of Medicine, https://pubmed.ncbi.nlm.nih.gov/20726679/

[ii] Pettinger, 2022, “Information Failure”, Economics Help: Helping to Simplify Economics, https://www.economicshelp.org/blog/glossary/information-failure/