Why third-party payers are gobbling up PBMs

|

| Click to Learn More |

Pending remaining state approvals for that $67 billion pact and the expected clearance of the CVS-Aetna megamerger, the three largest PBMs will all be hitched to health plans. UnitedHealth created its own in 1990 with OptumRx.

The crowded landscape has drastically changed from just a decade ago when PBMs were scooping up competitors and morphed the sector into one dominated by a few behemoths controlling the prescription drug benefit for millions of Americans.

Tyrone’s Commentary:

And I quote, “The black box model is under scrutiny,” Tanquilut said. “It’s better for them to be embedded. You can kind of hide your economics.” In a June 6, 2018 blog post I wrote,“if integrating the medical and pharmacy benefit requires that you relinquish flexibility and cost controls, the disadvantages of integration far outweigh the advantages.”

“Drug pricing is becoming a mainstream national issue,” Brian Tanquilut, an analyst with Jefferies, told Healthcare Dive. Tanquilut thinks the increased scrutiny has played a role in fueling these payer-PBM acquisitions.

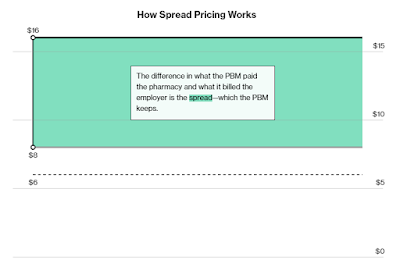

PBMs decide which drugs they will cover each year for their members and, to get a preferred status, drug manufacturers agree to rebates or discounts. It’s unclear how much of that savings actually makes it way back to patients. PBMs also use spread pricing — pocketing the difference between what they charge the pharmacy and what they bill their client.

“The black box model is under scrutiny,” Tanquilut said. “It’s better for them to be embedded. You can kind of hide your economics.”