Reference Pricing: Pharmacy Invoice Cost for Top Selling Generic and Brand Prescription Drugs

The costs shared below are what our pharmacy actually pays; not AWP, MAC or WAC. The bottom line; payers must have access to “reference pricing.” Apply this knowledge to hold PBMs accountable and lower plan expenditures for stakeholders.

As of 1/23/2014 – Published Weekly on Thursdays

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list. Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions. Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our pharmacy cost then determine if a problem exists. When there is a 5% or more price differential (paid versus actual cost) we consider this a problem. Multiple price differential discoveries means that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

When better pricing is discovered the contract language should stipulate the client be indemnified. Do not allow the PBM to limit the market check language to a similar size client, benefit design and/or drug utilization. In this case, the market check language is effectually meaningless. |

The Pharmacy Benefits Manager RFP; 7 Contract Tips for a Cost Efficient Drug Benefit Design

- Skip the RFP as it is largely a waste of time and money. Instead draft an airtight FIDUCIARY contract and put it out for bid

- Acquire “reference pricing” AND relentlessly measure cost performance

- Write meaningful financial and performance guarantees

- Mandate full transparency and complete audit rights

- Create market check and carve-out rights that currently don’t exist in almost all PBM contracts

- Shorten contracts (to 2 years) and include favorable contract termination rights

- Eliminate rebate and/or savings program loopholes

Pharmacy Cost [invoice] for Top Selling Brand and Generic Prescription Drugs

The costs shared below are what our pharmacy actually pays; not AWP, MAC or WAC. The bottom line; payers must have access to “reference pricing.” Apply this knowledge to hold PBMs accountable and lower plan expenditures for stakeholders.

As of 01/16/2014 – Published Weekly on Thursdays

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list. Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions. Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our pharmacy cost then determine if a problem exists. When there is a 5% or more price differential (paid versus actual cost) we consider this a problem. Multiple price differential discoveries means that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

When better pricing is discovered the contract language should stipulate the client be indemnified. Do not allow the PBM to limit the market check language to a similar size client, benefit design and/or drug utilization. In this case, the market check language is effectually meaningless. |

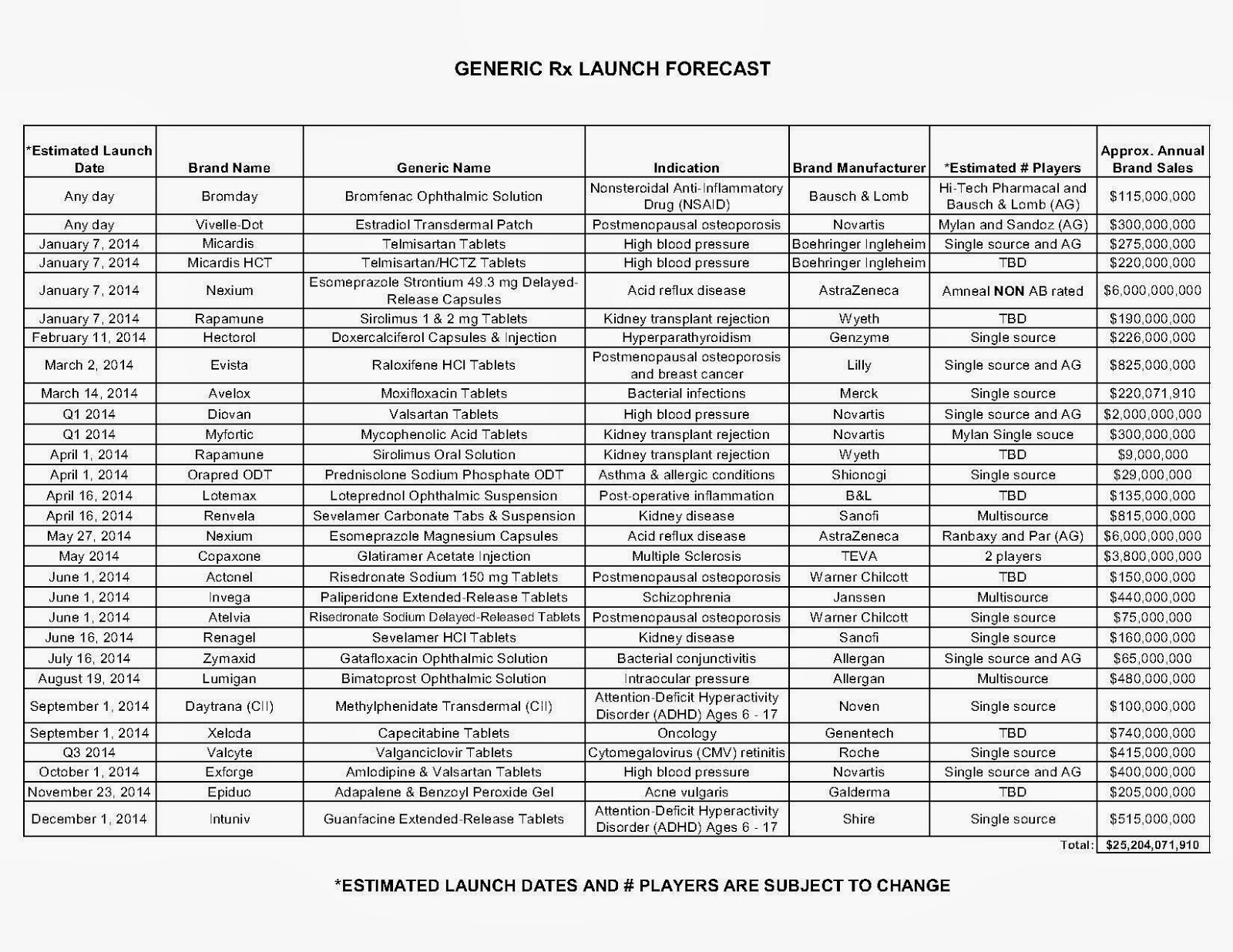

PBMs and generic drugs: Is the good news ending?

|

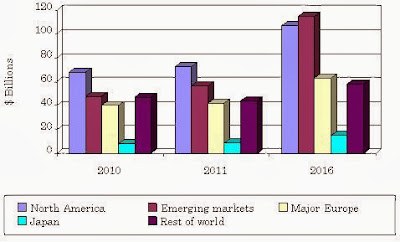

| Generic Drugs and the Global Market |

Many major brand name drugs are at the end of their patent-protected life cycles and now face generic competition. Two years ago, Lipitor and Plavix alone were at $15 billion combined revenue but are nearing the end of their revenue blitz with a projected drop to as low as $1 billion.

Pharmacy Invoice Prices (Actual) for Top Selling Generic and Brand Prescription Drugs

The costs shared below are what our pharmacy actually pays; not AWP, MAC or WAC. The bottom line; payers must have access to “reference pricing.” Apply this knowledge to hold PBMs accountable and lower plan expenditures for stakeholders.

As of 01/09/2014 – Published Weekly on Thursdays

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list. Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions. Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our pharmacy cost then determine if a problem exists. When there is a 5% or more price differential (paid versus actual cost) we consider this a problem. Multiple price differential discoveries means that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

When better pricing is discovered the contract language should stipulate the client be indemnified. Do not allow the PBM to limit the market check language to a similar size client, benefit design and/or drug utilization. In this case, the market check language is effectually meaningless. |

Mail order drug systems more cost effective than brick-n-mortar pharmacies

Pharmacy Invoice Prices (Actual) for Top Selling Generic and Brand Prescription Drugs

As of 12/19/2013 – Published Weekly on Thursdays

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list. Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions. Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our pharmacy cost then determine if a problem exists. When there is a 5% or more price differential (paid versus actual cost) we consider this a problem. Multiple price differential discoveries means that your organization or client is likely overpaying. REPEAT these steps once per month.

— Tip —

Always Include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to determine if better pricing is available in the marketplace compared to what the client is currently receiving.

When better pricing is discovered the contract language should stipulate the client be indemnified. Do not allow the PBM to limit the market check language to a similar size client, benefit design and/or drug utilization. In this case, the market check language is effectually meaningless. |

Adviser or Broker – which standard is most beneficial to plan sponsors?

Brokers (non-fiduciary)

- Must recommend “suitable” products, not necessarily best or least expensive

- Earn commissions or other transaction-based fees

- Must put clients interests before their own

- Most charge a fixed fee or percentage

A fiduciary duty is a legal and/or ethical relationship of confidence or trust between two or more parties. Typically, a fiduciary prudently takes care of money for another person. One party, for example a corporate trust company or the trust department of a bank, acts in a fiduciary capacity to the other one, who for example has funds entrusted to it for investment.

When a fiduciary duty is imposed, equity requires a different, arguably stricter, standard of behavior than the comparable tortious duty of care at common law. It is said the fiduciary has a duty not to be in a situation where personal interests and fiduciary duty conflict, a duty not to be in a situation where his fiduciary duty conflicts with another fiduciary duty, and a duty not to profit from his fiduciary position without knowledge and consent.

Resource for Payers: Acquisition Cost (pharmacy invoice) for Popular Brand & Generic Prescription Drugs

As of 12/12/2013 – Published Weekly on Thursdays

Step #1: Obtain a price list for generic prescription drugs from your broker, TPA, ASO or PBM every month.

Step #2: In addition, request an electronic copy of all your prescription transactions (claims) for the billing cycle which coincides with the date of your price list. Step #3: Compare approximately 10 to 20 prescription claims against the price list to confirm contract agreement. It’s impractical to verify all claims, but 10 is a sample size large enough to extract some good assumptions. Step #4: Now take it one step further. Check what your organization has paid, for prescription drugs, against our pharmacy cost then determine if a problem exists. When there is a 5% or more price differential (paid versus actual cost) we consider this a problem. Multiple price differential discoveries means that your organization or client is likely overpaying. REPEAT these steps once per month. |

Include a semi-annual market check in your PBM contract language. Market checks provide each payer the ability, during the contract, to see if better pricing is available in the marketplace compared to what the client is currently receiving.

When better pricing is discovered the contract language should stipulate the client be indemnified. Do not allow the PBM to limit the market check language to a similar size client, benefit design and/or drug utilization. In this case, the market check language is effectually meaningless. |

- Go to the previous page

- 1

- …

- 127

- 128

- 129

- 130

- 131

- 132

- 133

- …

- 140

- Go to the next page