If you are a self-funded employer, your health plan is the payer of last resort. Every hidden spread, every rebate-driven formulary choice, every “mandatory” specialty pharmacy shift, every opaque fee that is not clearly defined in writing comes out of plan assets. That is money you could have used to lower contributions, avoid benefit cuts, or invest in people.

The conflict problem is not theoretical. Federal and state findings describe a market that is both highly concentrated and heavily vertically integrated. The Federal Trade Commission’s interim staff report found the top three PBMs processed nearly 80 percent of U.S. prescriptions in 2023 and the top six processed more than 90 percent, with the largest PBMs integrated into insurers and pharmacies (1). The same FTC report found PBM-affiliated pharmacies account for nearly 70 percent of specialty drug revenue and documented two specialty-generic case studies where PBM-affiliated pharmacies were often paid 20 to 40 times the National Average Drug Acquisition Cost (NADAC), with nearly $1.6 billion in dispensing revenue above NADAC for those two drugs (2020 through part of 2022).

Regulators are now putting “fiduciary standard of care” into the PBM conversation in a way that self-funded employers have wanted for years. In early 2026, DOL proposed a PBM fee disclosure rule under ERISA section 408(b)(2) designed to force disclosure of direct and indirect compensation and to give plan fiduciaries audit rights (2). In February 2026, Congress enacted the Consolidated Appropriations Act, 2026 (Public Law 119-75), adding major PBM oversight and transparency provisions for group health plans and, critically, wiring 100 percent pass-through of “rebates, fees, alternative discounts, and other remuneration” into ERISA plan contracting standards on a defined timeline (3).

Why self-funded employers become the “payer of last resort”

Self-funded plans do not “buy insurance” for the pharmacy benefit in the way fully insured groups do. They fund claims. That makes PBM incentives a governance issue, not just a procurement issue.

ERISA already expects plan fiduciaries to understand what service providers are paid and to ensure compensation is reasonable. In 2014, the ERISA Advisory Council examined whether PBMs should be required to disclose fees and compensation so plan sponsors could meet ERISA’s “reasonable compensation” expectations under section 408(b)(2) (4). Twelve years later, DOL’s 2026 proposed rule is basically the government acknowledging the obvious: PBM compensation is complex, can come from multiple directions, and is difficult for fiduciaries to evaluate without standardized disclosure and audit rights (5).

A second layer that self-funded employers often underestimate is the broker/consultant channel. A STAT investigation reported that some consulting firms may be paid by PBMs on a per-prescription basis, with sources describing at least $1 per prescription and up to $5 per prescription in extreme cases, plus other forms of compensation. Whether every allegation in the market pans out is almost beside the point: if your advisor is compensated by the entity they are supposed to challenge, it weakens your fiduciary posture and your negotiating leverage. “Vendor selection” becomes “vendor placement.”

If your PBM, your broker, or your consultant cannot give you a clean compensation story in writing, they are not operating at a fiduciary standard of care. They are operating at a sales standard.

The conflict map: how PBMs make money and how each conflict hits employers

PBMs offer real services: network contracting, claims adjudication, formularies, utilization management, and rebate negotiation. The problem starts when the PBM’s profit depends on decisions that make the plan spend more, not less.

To keep this practical, here are the main conflict types you asked for, framed as “what it is,” “how the PBM wins,” and “how the self-funded employer loses.”

Rebate steering and rebate-driven formularies: manufacturers pay rebates and fees tied to formulary placement and market share. Those arrangements can reward high list prices and large rebates rather than low net cost. The FTC has warned that rebate and fee agreements used to secure exclusion of lower-cost products may incentivize steering to higher-cost drugs and block competition from cheaper generics and biosimilars (6). A self-funded employer loses twice: higher gross ingredient cost today, and a plan design reality where members’ deductibles/coinsurance are often based on gross prices, not net prices after rebates.

Formulary control as a profit center: formulary placement is not just “clinical.” It is a pricing lever. Economic research on rebate contracting and formulary design shows how formulary position can be traded for rebate value, which means the PBM’s “preferred drug” is not automatically the plan’s lowest net option (7). Employers get marketing language about “rebate guarantees” and “discounts,” but the real harm shows up in which drugs get preferred tier status and which lower-cost competitors get boxed out.

Spread pricing: spread is the margin between what the plan (or its carrier/TPA) pays the PBM and what the PBM reimburses the pharmacy. State audits show how large this can be in public programs. Ohio’s Auditor found total spread of $224.8 million in a 12-month period (Apr 2017–Mar 2018), with generic spread representing 31.4 percent of amounts paid for generics in that dataset (8). Kentucky’s “Opening the Black Box” report found PBMs were paid $957.7 million through MCOs for spread-pricing contracts in CY2018, with $123.5 million (12.9 percent) not paid to pharmacies and kept by PBMs as spread (9). Self-funded employers should treat these as warnings because the same mechanics exist in commercial contracts, just with fewer public audit rights.

PBM ownership of specialty pharmacies and specialty steering: vertical integration turns “benefit management” into self-preferencing. The FTC found PBM-affiliated pharmacies now account for nearly 70 percent of specialty drug revenue, and documented steering mechanisms and pricing outcomes that favor affiliated channels (1). When the PBM owns the specialty pharmacy, the plan is effectively negotiating with a party that can move volume to itself and capture dispensing margin. As one industry benefits leader put it, the Big 3 control both the “rebate pipeline” and the “utilization pipeline,” creating a closed loop.

Gag clauses and “clawbacks” at the pharmacy counter: historically, some contracts limited pharmacists from telling patients when a cheaper cash price existed. Congress passed two laws in 2018 aimed at banning gag clauses in private plans and Medicare, reflecting the view that these restrictions caused overpayment at the point of sale (10). Even after gag clause bans, disputes continue around cost-sharing that can exceed the pharmacy’s negotiated price. In Negron v. Cigna/OptumRx litigation, plaintiffs alleged schemes where insureds were charged more than the negotiated amounts and excess money was remitted back, described as “clawbacks.” (11) For self-funded employers, this is not just member pain. It can increase overall plan costs and trigger fiduciary litigation risk when participants claim the plan allowed unjustified pricing.

Opaque “pass-through” promises and hidden remuneration: “pass-through” is often marketed as “we pass rebates.” In reality, compensation can show up as many categories: manufacturer admin fees, data fees, pharmacy DIR-like fees/recoupments, spread on specific channels, price protection terms, rebate aggregation retained amounts, and affiliate payments. DOL’s Jan 2026 fact sheet explicitly calls out categories like spread compensation, pharmacy clawbacks, and price protection arrangements as reportable compensation categories, and proposes audit rights so fiduciaries can verify accuracy (12). The DOL proposal also notes concerns about rebate aggregators/GPOs formed outside the U.S. and the need to capture compensation flowing to “agents” that do not fit neat affiliate/subcontractor definitions (5).

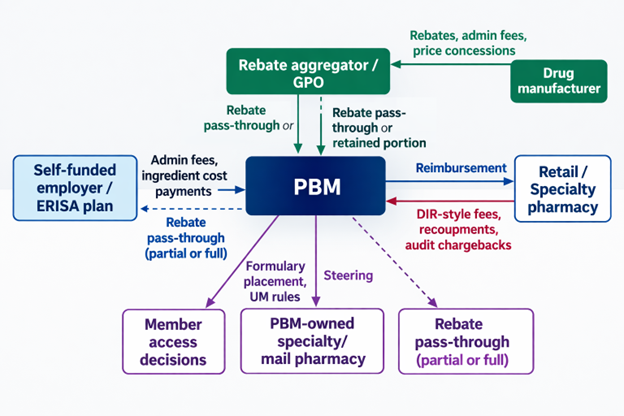

A simple visual of where conflicts show up in a typical commercial flow is below. It matches the structure described in state Medicaid reporting and federal discussions, even though the exact contract terms vary widely.

What the public record shows: quantified impacts, lawsuits, enforcement

The data problem for employers is that the strongest transparency is often found in government audits and enforcement, not in commercial PBM sales decks. Still, the public record has enough signal to justify hard questions in every RFP and renewal.

The dollars are concentrated where conflicts pay: in Ohio’s Medicaid managed care audit period, generics were 86.1 percent of claims but only 26.2 percent of spend, while brand drugs were 13.4 percent of claims but 49.3 percent of spend, and specialty was 0.5 percent of claims but 24.4 percent of spend (8). That pattern is why rebate-driven and specialty steering conflicts matter so much in employer plans too.

The chart above uses Ohio Medicaid managed care (Apr 2017–Mar 2018) because it is audited and publicly documented. It should not be treated as your plan’s exact mix, but it is a useful reminder that “generic discounts” are not where most dollars sit.

Spread can be massive when it exists. In Ohio, the Auditor’s table shows $224.8 million in total spread over that 12-month period, with $208.4 million of spread on generics alone. In Kentucky CY2018, PBMs reported $123.5 million in spread (12.9 percent) on $957.7 million paid through MCO spread contracts. These are not “rounding errors.” They are business model revenue.

The FTC’s specialty-generic case studies show another way the money leaks: dispensing margins at PBM-affiliated pharmacies that can dwarf what employers assume is “reasonable.” The interim staff report states PBM-affiliated pharmacies were often paid 20 to 40 times NADAC for the two case study drugs, and retained nearly $1.6 billion in dispensing revenue in excess of NADAC (2020 through part of 2022).

Litigation and enforcement are now explicitly tying rebating practices to inflated list prices and restricted access. In September 2024, the FTC sued the three largest PBMs and their affiliated GPOs alleging anticompetitive and unfair rebating practices that inflated insulin list prices and impaired access to lower list-price products (13). In February 2026, the FTC announced a settlement with Express Scripts requiring major business practice changes and projecting up to $7 billion in out-of-pocket savings over 10 years (14). The FTC framed this as patient relief, but for self-funded employers, “out-of-pocket” is only one part of the story. A pharmacy claim has a plan-paid portion too, and insulin is routinely a material spend category in large plans.

The employer fiduciary risk is rising alongside enforcement. In March 2025, plan participants filed an ERISA class action against JPMorgan alleging mismanagement of prescription drug benefits and inflated drug prices tied to PBM contracting and oversight failures (15). Courts are also publishing decisions that outline how PBM-related pricing disputes get framed under ERISA, even when cases are dismissed on standing grounds.

You do not want your “PBM oversight program” to be invented for you by the plaintiffs’ bar. Build it now, document it, and tie it to a fiduciary standard of care.

Regulation and enforcement: where the ground is shifting

A lot has happened fast, and it is not going back to the old “trust us, it’s proprietary” era. Key federal moves affecting self-funded employers include:

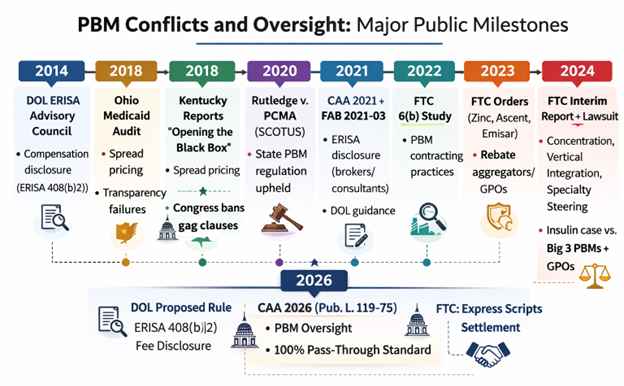

- State authority to regulate PBMs has expanded in practical terms since Rutledge v. PCMA (2020), where the Supreme Court held Arkansas’s PBM law was not preempted by ERISA.

- Congress banned gag clauses in 2018 for private plans (Patient Right to Know Drug Prices Act, Public Law 115–263) and for Medicare (Know the Lowest Price Act, Public Law 115–262).

- ERISA compensation disclosure for group health plan brokers and consultants was added via the Consolidated Appropriations Act, 2021, with DOL guidance in Field Assistance Bulletin 2021-03.

- FTC launched its 6(b) study in 2022 and expanded orders to rebate aggregators/GPOs in 2023.

- FTC’s July 2024 interim staff report put vertical integration, specialty steering, and rebate-driven competition issues into a single federal narrative.

- DOL’s January 2026 proposed PBM fee disclosure rule under ERISA 408(b)(2) is designed to force upfront and semiannual disclosure of PBM compensation and give fiduciaries audit rights.

- The Consolidated Appropriations Act, 2026 (Public Law 119-75) created a new statutory framework for PBM oversight and reporting to group health plans, with semiannual reporting and the ability to request quarterly reports in certain cases.

- The same 2026 law also hard-wires a 100 percent pass-through standard into ERISA reasonableness for PBM contracting, requiring PBMs to remit 100 percent of “rebates, fees, alternative discounts, and other remuneration” related to utilization or drug spending under the plan, subject to the law’s effective-date structure.

The takeaway for self-funded employers: the “fiduciary standard of care” is becoming enforceable expectations, not marketing language. DOL’s proposed rule and the 2026 statute both treat PBM compensation and data access as fiduciary essentials, not optional add-ons.

Prioritized Sources

Top primary and official sources used (ordered by practical importance for a self-funded employer fiduciary):

How We Can Work Together

Whether you’re a plan sponsor trying to get control of pharmacy spend, or a broker guiding clients through PBM decisions, education is the fastest way to improve outcomes. If you want a focused, high-value session your team can actually use, here are several ways we can work together.

Option 1: Get Certified

American College of Benefit Specialists (ACoBS) equips benefits professionals with practical knowledge across pharmacy, medical, retirement, and voluntary benefits. Organizations working with ACoBS-certified consultants gain better plan oversight, stronger vendor accountability, and more disciplined cost control. The certification signals a clear commitment to fiduciary guidance and protecting plan assets.

Option 2: Book a Webinar

A clean, educational session for employers, brokers, or TPAs. We’ll cover the most common PBM profit tactics, how to spot contract red flags, and what a fiduciary standard of care looks like in pharmacy benefits. Great for client education and thought leadership.

Option 3: Join the Virtual Roundtable

Bring your internal team (HR, Finance, and Benefits) or your broker group. I’ll lead a live discussion focused on PBM oversight, cost drivers, and what to ask your PBM right now. You’ll leave with a short action list you can use immediately.

Option 4: Get a Quote

Pharmacy benefits now rival medical spend for many plans. Yet most are still governed by contracts few have fully read and pricing models few can clearly explain. That is a fiduciary risk, not just a cost issue.

If you want lower spend, tighter oversight, and alignment you can defend in front of a board or audit committee, act with intent. Certify your team. Educate your clients. Pressure test your PBM. Run an RFP that exposes the full economics.

Hope is not a strategy. Oversight is. The employers who win in pharmacy benefits are not lucky. They are informed, disciplined, and unwilling to outsource accountability.