Loaded Dice: How Non-Fiduciary PBMs are Winning the Cash and Rebate Game

Since 2011, I’ve been writing about non-fiduciary PBMs and how they’re misleading clients with regard to the gargantuan amounts of money they earn from rebates or manufacturer revenue. And at almost every turn my advice has been ignored by health insurance brokers, benefits consultants and HR executives alike. Taken from a scene in the holiday classic, A Christmas Story, I double dog dare you now to ignore the new information I’m about to share with you.

Since 2011, I’ve been writing about non-fiduciary PBMs and how they’re misleading clients with regard to the gargantuan amounts of money they earn from rebates or manufacturer revenue. And at almost every turn my advice has been ignored by health insurance brokers, benefits consultants and HR executives alike. Taken from a scene in the holiday classic, A Christmas Story, I double dog dare you now to ignore the new information I’m about to share with you. On May 16, 2017 Express Scripts filed a Complaint against drugmaker kaleo. The Complaint revolves around the opioid overdose treatment, Evzio, which kaleo manufactures. Express Scripts’ attorneys redacted the Complaint, but did not redact some information that Express Scripts has long regarded as proprietary thus not typically made available to the public.

According to Express Scripts, it entered into rebate agreements with kaleo for Evzio that required kaleo to pay Express Scripts not just for rebates but also administrative fees. The Complaint reveals that in four of its invoices to kaleo, Express Scripts billed kaleo $26,812 in total for “formulary rebates” and $363,160 in total for “administrative fees.” That’s right, administrative fees amounted to almost 15 times more than the formulary rebates!

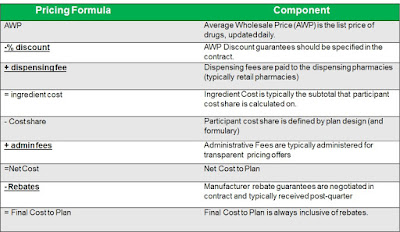

While plan sponsors believe they retain as much as 95% of rebate dollars (non-fiduciary PBM theoretically retains only the 5% difference), the truth is plan sponsors are retaining far less than 50% of rebates or earned manufacturer revenue! Remember, the primary point of rebates is to reduce net plan costs (table 1).

|

| Table 1: How net plan cost is calculated |

Rebates are not to be treated as “free” money by HR decision-makers who face budget shortfalls. In fact, I have it on good authority that is exactly what HR executives are doing not realizing that non-fiduciary PBMs rely on this sort of naivete in order to gain agreement on contracts that do not offer binding transparency.

The impact of entering into less than true pass-though pricing arrangements goes far beyond dollars and cents. In some cases, the consequences are life and death; not just “belly buttons” as some in the biz so poorly refer to patients. It makes my skin crawl when I here consultants refer to people as “belly buttons.” The metaphor clearly illustrates how out of touch they are with what is actually happening at the site-of-care because some of the people don’t have belly buttons but I digress.

The pass-through pricing arrangement you think you have entered into is nothing more than a traditional pricing arrangement expertly disguised as a pass-through one. Before going on, I believe it’s important that we stop here and define true pass-through pricing:

Pass-through pricing: the cost of a drug after adjustments are made for any and all financial benefits the PBM might receive in the form of discounts, dispensing fees, rebates, credits, grants, etc.

Express Scripts is not the only PBM that is playing with loaded dice. You’re safe to assume that every non-fiduciary PBM is generating huge sums of money for itself while engaging in similar secretive rebate arrangements. You, the client, are not being put first above shareholders.

|

| Click to learn more |

Evzio is an auto-injector that delivers a single dose of Naloxone, a life-saving drug that, if timely administered, can reverse the effects of an opioid overdose. In 2014, Evzio cost approximately $690 for a two-pack of single use auto-injectors. Depending on dosage strength, generics made by Hospira and Mylan ranged from about $23 to about $63 for a single injectable vial.

And there’s a third product that the FDA approved in 2015 – a nasal spray containing Naloxone called Narcan – which cost approximately $150 for a two-pack. Evzio is an innovative product that talks to those using it and explains how to use the auto-injector, as reflected in this kaleo video. But the generic injectors work just as well, as does the nasal spray Narcan (as long as a person is breathing).

The proverbial “cat is out of the bag” so let’s dig a little deeper into the information revealed in the Complaint. Express Scripts also included an additional provision in its contracts if kaleo increased the price of Evzio. The provision is called price protection rebates. These provisions typically state something like the following: ‘If the manufacturer increases the drug’s list price by more than _%, the manufacturer must provide a price protection rebate reimbursing the PBM for all price increases above the stated amount.’

In one invoice, May 2016, the formulary rebate amounted to only $9937.50 while administrative fees and price protection rebates amounted to $137,162.51 and 2,286,092.01, respectively. I’ve long known that non-fiduciary PBMs profited, excessively, from drug price increases above and beyond inflation. It should now be painfully clear to you now that they in fact generate massive sums of money in the back-end all the while detesting rapid price increases in the front-end or through the media.

Because Express Scripts and other non-fiduciary PBMs are not passing manufacturer revenue in full back to clients, exposing them to higher prices, it’s the epitome of hypocrisy. The best proponent of transparency is informed and sophisticated purchasers of PBM services. PBMs will provide transparency and disclosure to a level demanded by the competitive market and generally rely on the demands of prospective clients for disclosure in negotiating their contracts.

The point is assessing transparency is done more effectively by a trained eye with personal knowledge of the purchaser’s benefit and disclosure goals. The possibilities of eliminating hidden PBM cash flow are only limited by your level of knowledge and, of course, applicable law.