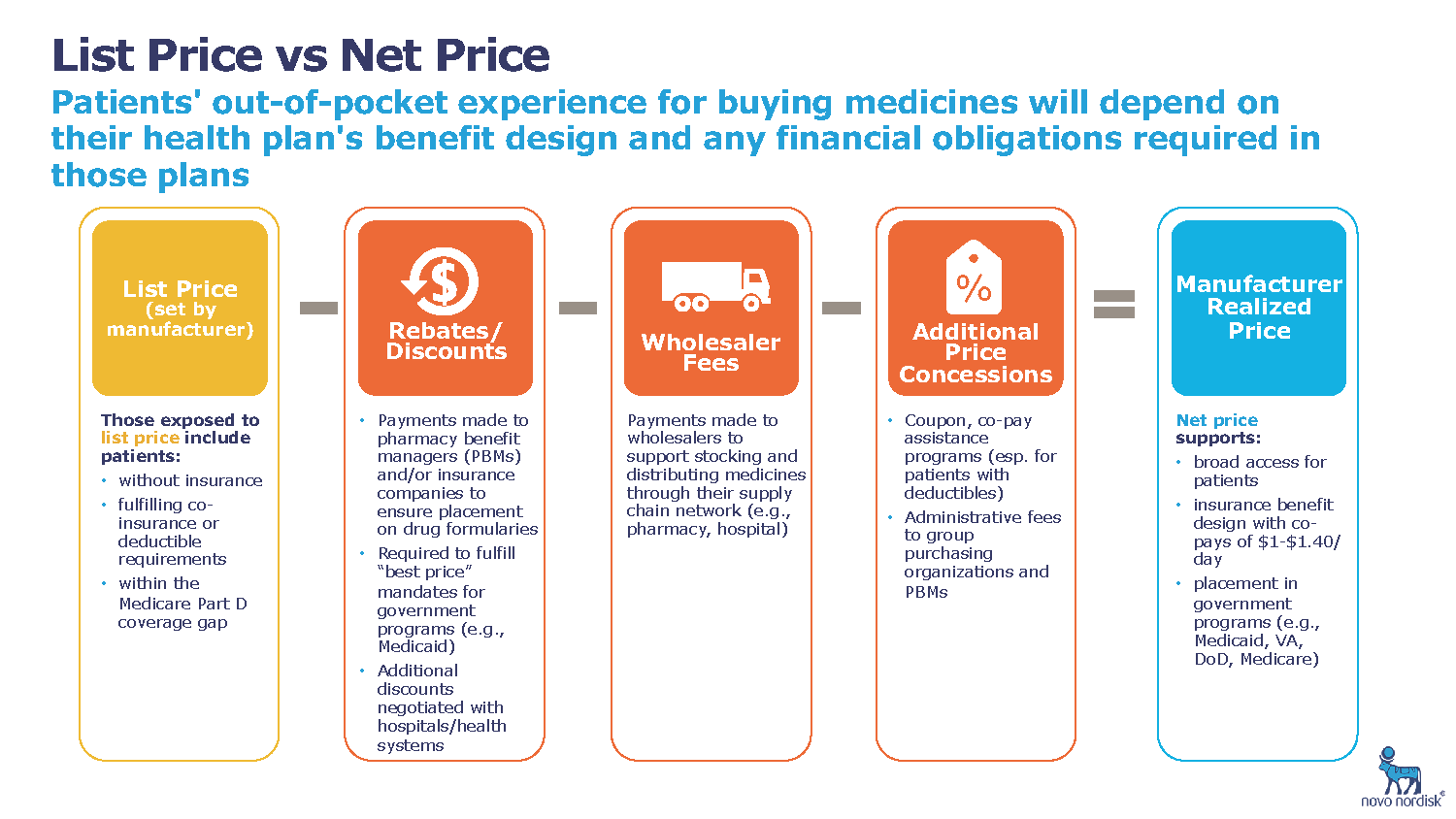

Insurers cutting back on drug coupons amid concerns over consumer costs

But some insurers, including in Illinois, are limiting how those discounts may be applied amid concerns they’re driving up health care costs for everyone. Curbing the coupons could mean more money out of consumers’ pockets in the short term, but in the long run could also help hold down drug prices and health care costs, say critics of the cards and coupons.

|

| Ex. Drug Coupon |

Blue Cross and Blue Shield of Illinois told its members with individual plans this year they can still take advantage of the discounts, but they won’t get credit toward their deductibles or out-of-pocket maximums. Cigna only allows coupons to be used for specialty drugs — medications used to treat rare or complex conditions. UnitedHealthcare and Aetna declined to comment on their policies on the discounts.

A number of experts and advocates for lower drug prices applaud any actions aimed at stemming the use of copay cards and coupons, which are available online, through the mail or from doctors.

Tyrone’s comment: I’m not one of those individuals who doesn’t like drug coupons. However, I do agree that patients should not be rewarded by having coupon amounts applied to their deductible or MOOP. Let’s keep it real, non-fiduciary PBMs and health plans don’t like coupons because typically the products with coupons available won’t pay rebates which takes away from the revenue they would have earned from those products which do pay rebates. Plan sponsors follow suit because their PBM or carrier says it’s a bad thing. If a patient is unable to start or complete specialty drug therapy, due to cost which a coupon may have alleviated, the resulting hospital bill will cost more in the long run. Is it about the patient or not?

Typically, patients with individual and employer-based plans can use the cards or coupons to save money on their insurance copays for certain prescription medications at the pharmacy. While a coupon can reduce all or part of a patient’s copay, the insurance company still has to pay its full portion for what might be a high-priced drug — a cost that opponents of the discounts say is ultimately passed on to all consumers in the form of higher insurance premiums.

Such discounts made news last year amid outcry over the skyrocketing costs of EpiPens, sold by Mylan. As part of its response to the uproar, Mylan offered $300 savings cards to patients with nongovernment insurance to help lower their out-of-pocket costs. Mylan still faced criticism that the discounts wouldn’t help everyone as much as simply lowering the price would.

“The copay coupons are a scam by the drug companies,” said David Mitchell, president and founder of Patients for Affordable Drugs, a nonprofit that doesn’t take money from drug companies or insurers. “Effectively we wind up, all of us, paying a higher price for our health insurance because they just steered us to a more expensive drug that ultimately gets paid for by someone.”