American College of Physicians Position Paper: Recommendations for PBMs to Stem the Escalating Costs of Prescription Drugs

The authors reviewed available studies, reports, and surveys related to health plans and PBMs from PubMed, Google Scholar, relevant news articles, policy documents, and Web sites and primarily looked at costs and spending associated with PBMs, PBM rebates and negotiations, and transparency.

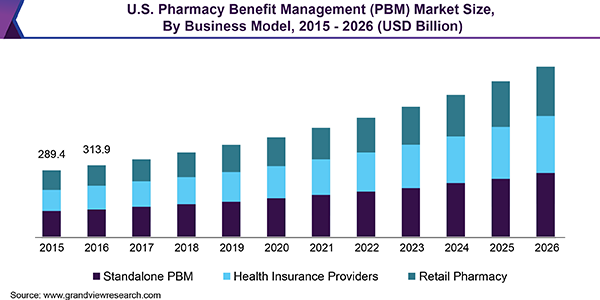

Pharmacy benefit managers originated for the purposes of claims processing, mail order pharmacy services, and retail pharmacy network management and started to evolve as employers began including broad prescription drug coverage in their employee benefit packages. Their role increased in subsequent decades, particularly after passage of the Medicare Prescription Drug, Improvement, and Modernization Act in 2003.

After passage of the act, PBMs generally represented Part D plans in negotiations with pharmaceutical manufacturers because the federal government was prohibited from negotiating prices directly with drug manufacturers. The function of a PBM is to negotiate rebates with pharmaceutical manufacturers in exchange for favorable placement of drugs on tiered formularies. The PBM then passes those rebates on to employers or plan sponsors, who in turn pass the savings from rebates on to employees or beneficiaries through lower premiums.

Tyrone’s Commentary:

Pass-through and Transparent PBM business models are often the same in name and performance. Watch the YouTube video above.

PBMs have been criticized for a lack of transparency, and there can be confusion or misinformation about how they work, how they contract with employers or purchasers, how they make decisions about formularies, how much money they take in, and how much money is actually passed on to consumers. At the state and federal level, policymakers are attempting to improve transparency for PBMs and other parts of the supply chain.