Unpacking the Concept of Pass-Through Pharmacy Benefit Managers: Benefits and Challenges

A pharmacy benefit manager (PBM) pass-through is a pricing arrangement in which the PBM does not retain any portion of the spread which is the difference between the reimbursement it receives from the payer and the cost of the drug it pays to the pharmacy or refunds paid by a rebate aggregator. Instead, the full spread is passed on to the pharmacy and refunds to the employer. This arrangement allows for increased transparency and helps to control drug costs for payers and patients. When unpacking the concept of pass-through pharmacy benefit managers consider these benefits and challenges.

Benefits

- Cost savings: A pass-through PBM can help employers reduce their overall drug costs by passing on the full spread between the reimbursement received from the payer and the cost of the drug to the pharmacy.

- Improved transparency: A pass-through PBM provides increased transparency in pricing and reimbursement, allowing employers to better understand and manage their drug costs.

- Increased negotiating power: By eliminating the PBM’s profit margin, a pass-through PBM provides employers with greater negotiating power when it comes to securing favorable prices for drugs.

- Better alignment of incentives: With a pass-through PBM, the incentives of the PBM are aligned with the employer’s goals of controlling drug costs, as the PBM does not benefit from higher drug prices.

- Improved patient outcomes: A pass-through PBM can help improve patient outcomes by ensuring that patients have access to the most appropriate and cost-effective medications. This can also lead to improved employee health and productivity, which can benefit the employer.

Challenges

- Retention of rebates or discounts received from drug manufacturers: If a PBM retains any portion of rebates or discounts received from drug manufacturers, it cannot be considered a true pass-through PBM.

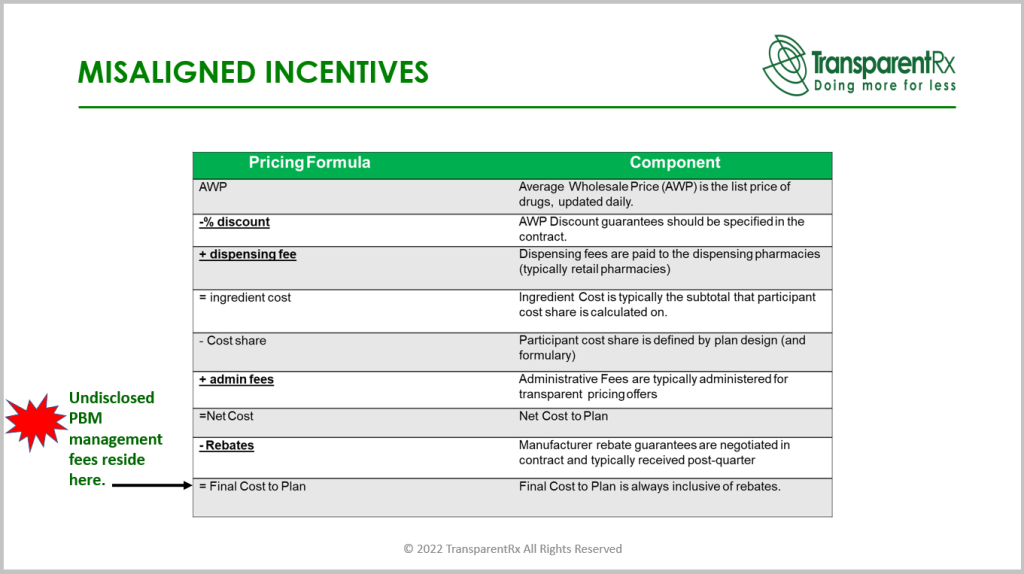

- Undisclosed management fees: If a PBM hides management fees, it may not be considered a pass-through PBM as these fees increase the costs passed on to the employer. In pharmacy benefits management, these management fees are referred to as earnings after cash disbursements (EACD).

- Misuse of the spread: If a PBM misuses the spread by using it for purposes other than covering its administrative costs, it cannot be considered a pass-through PBM.

- Steering patients to higher-cost drugs: If a PBM steers patients to higher-cost drugs to increase the spread, ingredient cost or rebate, it cannot be considered a pass-through PBM.

- Lack of transparency in pricing and reimbursement: If a PBM does not provide clear and transparent information on pricing and reimbursement, it may not be considered a pass-through PBM. This lack of transparency makes it difficult for pharmacies to accurately determine the cost of drugs and determine if they are receiving a fair price.

Management fees are the PBM’s cash balance after bills have been paid. Those bills include but are not limited to ingredient costs, dispensing fees, and refunds or rebates. Two things are required for a PBM to be considered pass-through; disclosure of management fees and the data necessary to verify the accuracy of management fees paid to the PBM. High management fees are paid when a PBM profits from ingredient cost and rebate spreads. Exorbitant management fees are paid when employers don’t know what their management fee (EACD) is.

PBMs know what employers want to see so they give it to them. Slide decks, proposals, and conversations all point to pass-through business models. How those same PBMs behave once the group goes live more closely resembles rent-seeking. Unpacking the concept of pass-through pharmacy benefit managers is not without its challenges. Consultants and HR must be astute in evaluating PBM contract language, for instance. A pass-through PBM will share its management fee and the data for verification. If a PBM is unwilling to share its management fee and provide the data necessary to verify accuracy, assume it is hiding something.