How Self-Funded Employers Can Use Point Solutions to Manage Pharmaceutical Costs [Weekly Roundup]

How Self-Funded Employers Can Use Point Solutions to Manage Pharmaceutical Costs and other notes from around the interweb:

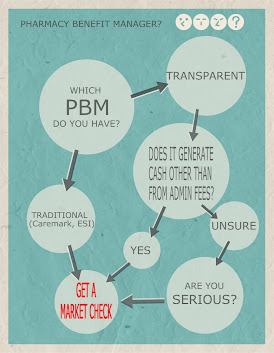

- How Self-Funded Employers Can Use Point Solutions to Manage Pharmaceutical Costs. Point solutions are specialized tools or platforms designed to address specific issues or challenges faced by organizations. In the context of pharmaceutical cost management, point solutions provide targeted assistance in identifying cost-saving opportunities, improving medication adherence, streamlining prescription processes, and enhancing overall health outcomes. Before delving into the benefits of point solutions, it is essential for self-funded employers to gain a comprehensive understanding of their pharmaceutical costs. This entails assessing the utilization patterns, identifying high-cost drugs, analyzing prescription data, and exploring trends in pharmacy benefit claims. By closely examining these factors, employers can identify areas of potential savings and develop tailored strategies to optimize their pharmacy benefit plans.

- Employers are suing their health plan for claims data in increasing numbers. Lawsuits from large companies and employers are increasingly being filed against third-party health plan administrators to access complete employee medical claims data. Through lawsuits recently filed against Aetna, Elevance Health and BCBS Massachusetts, employers claim payers have breached their fiduciary duties by not allowing complete access to claims data and how claims are processed. In a June 30 complaint, Kraft Heinz alleged Aetna has used its role as its TPA “to enrich itself to Kraft Heinz’s detriment” through undisclosed fees and processing medical and dental claims without human review. In December, bricklayer and metal worker unions filed a lawsuit against Elevance Health, alleging the payer does not allow self-insured plans to access their own claims data and charges the plans higher rates than it had negotiated with hospitals. A labor union in Massachusetts sued BCBS Massachusetts in April over similar allegations. These lawsuits are largely being driven by the Consolidated Appropriations Act and the hospital price transparency rule that took effect in 2021, according to a July 6 Bloomberg Law report.

- Playbook for Employers – Addressing PBM Misalignment. The guide, released by the National Alliance of Healthcare Purchaser Coalitions, identifies several key strategic recommendations that employers can adopt when looking to better navigate their relationship with PBMs. For one, the playbook recommends that employers find advisers that are genuinely putting in the work for them. Advisers should be independent and transparent, according to the guidebook, and contracts should be designed to ensure that PBMs act in the employer’s best interest. “As we uncover these increasingly apparent anomalies, I think we’ve got to challenge ourselves to do better and most importantly require that our advisers, our middlemen and our intermediaries do better on our behalf,” Mike Thompson, CEO of the alliance, told Fierce Healthcare.

- STAT News investigation takes deep dive into PBM broker conflicts of interest. Employers across the country — from big names like Boeing and UPS to local school systems — pay consulting firms to handle a straightforward task with their prescription drug coverage: Get the best deals possible, and make sure the industry’s middlemen, known as pharmacy benefit managers, aren’t ripping them off with unfair contracts. But a largely hidden flow of money between major consulting conglomerates and PBMs compromises that relationship, a STAT investigation shows. Some consulting firms often are getting paid more — a lot more — by the PBMs and health insurance carriers that they are supposed to scrutinize than by companies they are supposed to be looking out for.