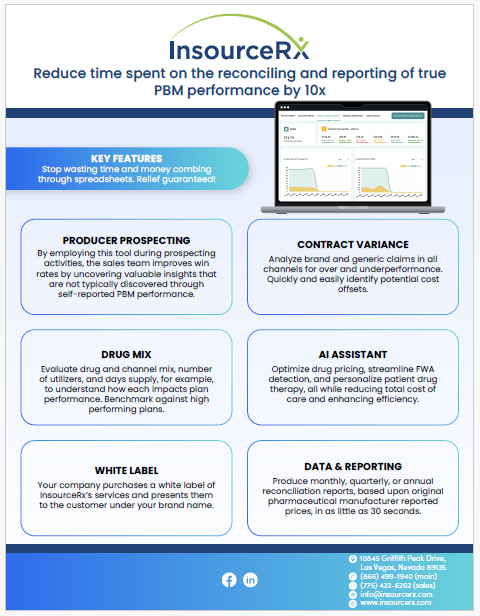

Leveraging Data Analytics in PBM: A Strategic Imperative for Decision Makers

In the complex and dynamic realm of Pharmacy Benefit Management (PBM), the strategic use of data analytics stands as a cornerstone for achieving competitive advantage, cost efficiency, and superior patient outcomes. As decision-makers—pharmacy benefit consultants, employee benefit brokers, CFOs, and CHROs—it’s imperative to understand the transformative role of leveraging data analytics in PBM and the critical need for a shift towards digital transformation, moving beyond traditional reliance on spreadsheets.

The Strategic Role of PBM Data Analytics

Data analytics in PBM transcends mere number crunching; it’s about deriving actionable insights that drive strategic decisions. This involves analyzing diverse datasets, including prescription claims, patient demographics, drug pricing, and pharmacy networks, to:

- Enhance Cost Management: Strategically reduce costs while maintaining or improving care quality.

- Improve Fraud Detection: Employ sophisticated analytics to identify and mitigate fraudulent activities effectively.

- Optimize Patient Care: Utilize data to personalize medication management, improving health outcomes.

- Boost Operational Efficiency: Identify and address inefficiencies, streamlining processes for better performance.

Why Digital Transformation is Essential

The reliance on spreadsheets for managing and analyzing PBM data is increasingly becoming a bottleneck in an era defined by big data. Here’s why embracing digital transformation is not just an option but a necessity for industry leaders:

Scalability and Complexity

As organizations grow, the volume and complexity of data escalate, making spreadsheets impractical. Digital analytics platforms are designed to handle large datasets effortlessly, providing the scalability needed to adapt and thrive.

Enhanced Accuracy and Reliability

The manual processes associated with spreadsheets are prone to errors. Digital solutions automate data processing, significantly reducing the risk of inaccuracies and enhancing the reliability of insights.

Advanced Analytical Tools

Digital transformation opens the door to advanced analytics, including predictive modeling, machine learning, and AI, offering deeper insights and foresight that are invaluable for strategic planning and decision-making.

Seamless Data Integration

Integrating data from various sources is crucial for a comprehensive view of PBM operations. Digital platforms facilitate this integration, breaking down silos and enabling a unified analysis.

Regulatory Compliance and Data Security

In the healthcare sector, data security and regulatory compliance are paramount. Digital platforms offer sophisticated security features and compliance capabilities, ensuring data is managed responsibly and securely.

Charting the Path Forward

For decision-makers in the PBM space, the move towards digital analytics is a strategic imperative. Here’s how to navigate this transition:

- Conduct a Thorough Assessment: Evaluate your current data management and analytics practices to identify gaps and opportunities for improvement.

- Invest in the Right Technology: Choose data analytics platforms that align with your strategic goals and operational needs.

- Develop Skills and Knowledge: Ensure your team is equipped to leverage new technologies through training and professional development.

- Implement Robust Data Governance: Establish clear policies for data management to ensure accuracy, security, and compliance.

Conclusion

For pharmacy benefit consultants, employee benefit brokers, CFOs, and CHROs, the journey towards leveraging data analytics in PBM is not just about adopting new technologies; it’s about strategically positioning your organization for success in a rapidly changing landscape. By embracing advanced data analytics, you can unlock unparalleled opportunities for cost savings, operational excellence, and improved patient care. The future of PBM is data-driven, and the time to act is now.