Why Medication Adherence Matters

Medication adherence determines whether a therapy delivers any value. In chronic disease, roughly half of all patients do not take their medications as prescribed. High out-of-pocket costs, poor care coordination, and unnecessary hurdles all contribute to missed fills or long gaps in therapy.

Employers feel the financial impact. Nonadherence drives avoidable hospitalizations, emergency room visits, and complications that spill into the medical plan. Lost productivity adds another layer of expense when conditions flare up because medications aren’t taken consistently. When prescriptions go unfilled, the employer pays for a benefit that never produces the expected clinical or financial return. (1)

This is why affordability matters. When members skip medications due to cost, adherence falls and overall costs rise. A PBM operating under a fiduciary standard has a duty to remove barriers, track adherence, and intervene early. Most PBMs do not. They track dispensing, not outcomes, and employers end up carrying the downstream burden. (2)

How Adherence Is Measured: MPR and PDC

Because it’s impractical to observe directly whether every patient takes every pill, the industry relies on proxy metrics using refill/claims data. Two widely accepted measures are:

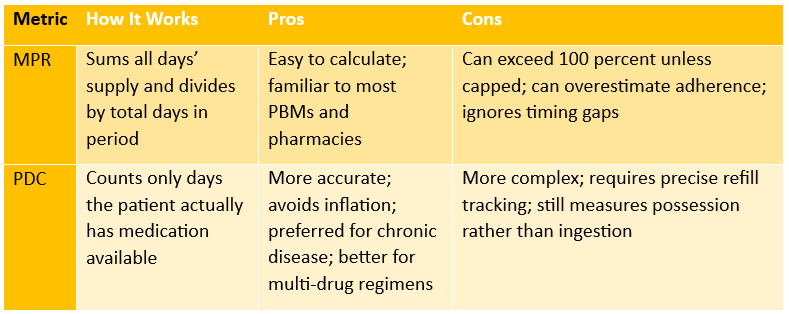

Medication Possession Ratio (MPR)

- MPR = (total days’ supply dispensed over a given period) ÷ (number of days in that period) (3)

- Example: If over a 365-day period a patient receives a total of 300 days’ worth of medication, MPR = 300 / 365 = 82.2%.

Proportion of Days Covered (PDC)

- PDC = (number of days within period when patient has medication on-hand) ÷ (number of days in the period) (4)

- Example: A member receives a 30-day supply of a maintenance medication on January 1. They refill on February 5 with another 30-day supply. The first fill covers January 1 through January 30. The refill on February 5 extends coverage from January 31 through March 1. The member is without medication from January 31 through February 4, which creates a 5-day gap. Over a 60-day measurement period, they have medication available for 55 days. Their PDC is 55 divided by 60, which equals 91.6%.

What Happens When Employers / PBMs Don’t Prioritize Adherence

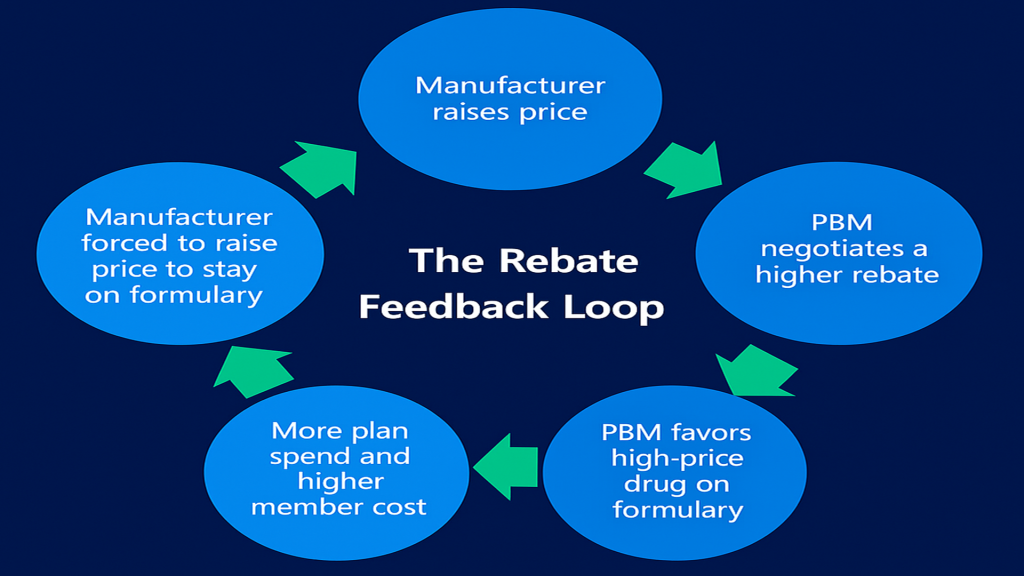

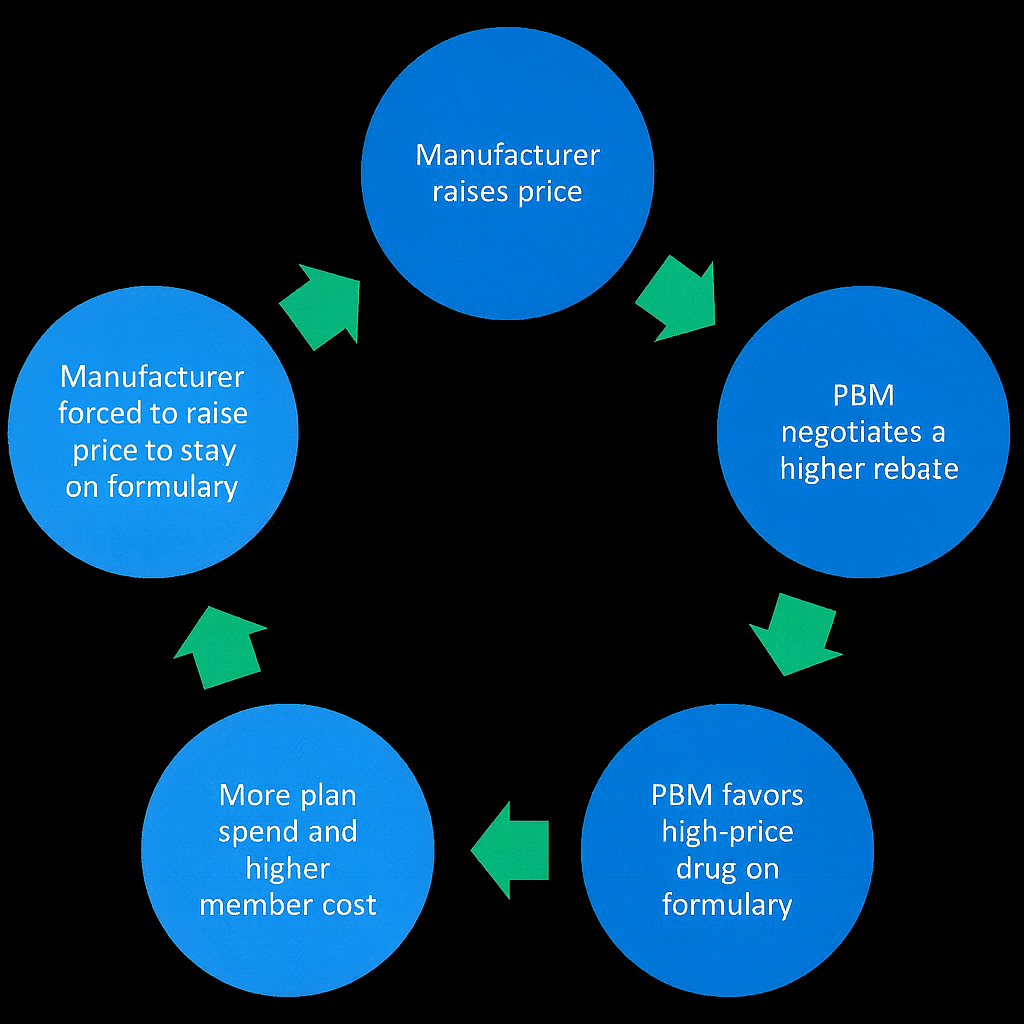

If a PBM or employer-sponsored plan focuses only on lowering drug spend through rebates, discounts, and formularies but ignores adherence, the expected savings often disappear.

- Low adherence undermines drug effectiveness. Patients may skip doses or not refill at all due to cost or confusion. That undercuts the clinical value of the benefit design.

- Poor adherence drives higher medical utilization. More hospitalizations, ER visits, complications from unmanaged chronic diseases. That increases overall plan costs.

- Lost productivity. Employees missing work, using sick days or disability leave. For example, studies show that improving adherence among a population with diabetes can reduce short-term disability days significantly, saving employers real dollars. (5)

- Waste: money spent on pharmacy benefit (drugs) that never deliver outcomes. If drugs are filled but not taken, the employer essentially paid for no clinical value.

Without adherence oversight, PBMs have little incentive to ensure refills translate into medication use, particularly when their revenue depends on dispensing volume or rebate maximization rather than outcomes.

A fiduciary PBM treats adherence as core to cost management. It monitors MPR and PDC, identifies members falling off therapy, addresses affordability barriers, and reports adherence trends transparently. Employers see fewer surprises in the medical plan and better outcomes across their population.

Sources:

- HealthLinks Certified: Medication adherence guide

- GoodRx: How affordability impacts adherence

- Pharmacy Times: Differences between adherence measures

- World Pharmacy Council: Best practices for measuring adherence

- Michigan Public Health: Impact of adherence on health outcomes and disability