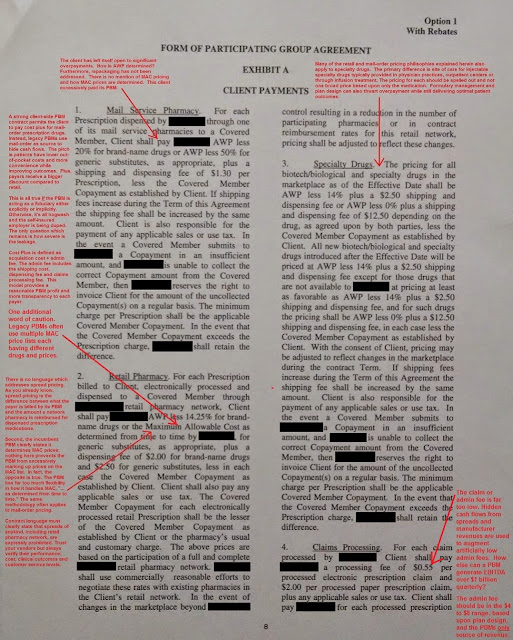

For the better part of the last decade, pharmacy costs have generally represented anywhere from 20 to 25 percent of total health plan costs. But over the past three years in particular, noticeable and sizeable growth in specialty drugs has occurred. In 2013, traditional drug trend increased by less than 1 percent, yet overall drug trend increased by 3.8 percent.

That additional growth from “non-traditional” drugs represents the emergence of specialty drugs in a matter that will act as a primary cost driver for employer health plans moving forward, as 65 percent of new drug spending over the past two years was for specialty medication. Industry projections assume that 80 percent of the top ten drugs sold in the United States will be specialty drugs by 2016.

While estimates of growth have varied mildly, general consensus in the pharmacy management industry suggests specialty costs will quadruple to around $400 billion by 2020. This estimate seems to be supported by observations that the drug-manufacturing development pipeline is ramping up efforts in the specialty fields. Currently, 50 percent of drugs in development are considered specialty in nature and around 70 percent of new drugs that will be approved to hit the market in the near-term will be defined as specialty drugs.

Until recently, most employers looked at pharmacy costs by observing two sectors: name-brand drugs and generic drugs. Current projections indicate that specialty drug spend will eclipse 33 percent of total drug spending for a health plan by 2016. Before that occurs, employers must begin looking at drug spend in three sectors in how they analyze, determine plan-guidance and build strategy: 1) Specialty drugs 2) name-brand drugs and 3) generic drugs.

What qualifies as a specialty medication?

- Generally speaking, a specialty medication meets one or more of the following criteria:

- Costs per script are greater than $750 per month

- Treats a rare and/or intensive condition not typically associated with chronic diseases

- Requires specific handling or monitoring processes

- Used in a limited distribution network

As of 2013, cancer, multiple sclerosis, rheumatoid arthritis, hepatitis C and growth hormone accounted for more than 60 percent of the specialty market. Given the investment in this drug category, costs in the specialty pharmacy arena will be diversified to include further drugs developed for HIV, hemophilia and other costly conditions that normally fall outside of the scope of typical disease management treatments for diabetes, hyperlipidemia and the like.

More than half of specialty drugs in the developmental pipeline are high-cost oral medications that intend to act as a substitute for other treatments, such as injectable drugs typically provided in physician practices, outpatient centers or through infusion treatment.

|

| Click to Enlarge |

What conditions are typically associated with specialty drugs? While this list is expansive, it will change and grow as further research and development occurs around other disease states and approval is provided. The percentages represent that condition’s estimated percent share of the specialty drug market:

- Oncology/Cancer: 30%

- Rheumatoid Arthritis: 12%

- Multiple Sclerosis: 10%

- HIV/AIDS: 8%

- Inflammatory Bowel Disease: 3%

- End Stage Renal Disease: 3%

- Intravenous Immunoglobulin: 4%

- Hemophilia: 3%

- Hepatitis C: 2%

- Growth Hormone: 3%

- Cardiovascular:3%

- Transplant: 1%

- Other: 19%

Since a small percentage of an employer population (generally less than 3 to 5 percent) will have any of the conditions that qualify for specialty drug treatments in the major areas of research and development, drug spend management will skew traditional per member per month (PMPM) metrics. A large share of medical spend will be isolated in a particularly small set of members who have these conditions.

How can an employer prepare for this significant change?

Basic observations on specialty drug spend will likely mirror an often under-emphasized, yet obvious trend that commonly occurs in medical spend: most costs are pooled in a small percentage of the population (generally far less than 10 percent of total membership) that have exceptional needs that cannot be addressed through lifestyle changes. These will quickly exceed the maximum out-of-pocket employee expenditures. In those instances, personalized and coordinated care has to exist for members to:

- Get the highest quality medical care as it relates to their needs

- Maintain medical compliance and adhere to evidence-based guidelines for treatment

- Gain assistance in navigating the medical continuum to offset costs related to waste, mismanagement and improper treatment

Since specialty pharmacy costs will mimic these resource demands, employers should be prepared to build metric-driven tactics to effectively address how specialty drug coverage is engaged at both the member level and how the costs are appropriately staged to minimize unnecessary cost.

Funding questions to consider:

- How does an employer create an opportunity to ensure specialty drugs are accessed only in situations where they are the best option?

- How does an employer build a process to ensure they are getting to most cost-effective method of delivery for specialty medications?

- How does the employer design their benefit plan to distribute the specialty medications effectively without creating an overall plan burden that will result in increased costs for the employer and overall membership base?

- How will an employer’s comprehensive plan design interact and impact this particular cost? Conversely, how will specialty drug usage interact and impact comprehensive plan design?

- How does an employer engage the specialty pharmacy process? Should it be directly through the carrier/TPA or through a vendor relationship?

- How does an employer ensure they are getting the best arrangement for specialty medication as it relates to overall medical costs?

Given the climate regarding this expansive market change, employers should prepare in a constructive manner by analyzing current risks within their population’s medical and pharmacy spend. They should work with experienced consultants and other health plan stakeholders that understand the progression in order to determine proper benchmarks and strategy for the next five years –the precise timeframe this specialty medication boom will occur.

by Chris Davis

Chris Davis, MPH, ACSM

Director of Health Mgmt &

Claims Informatics

Regions Insurance Inc