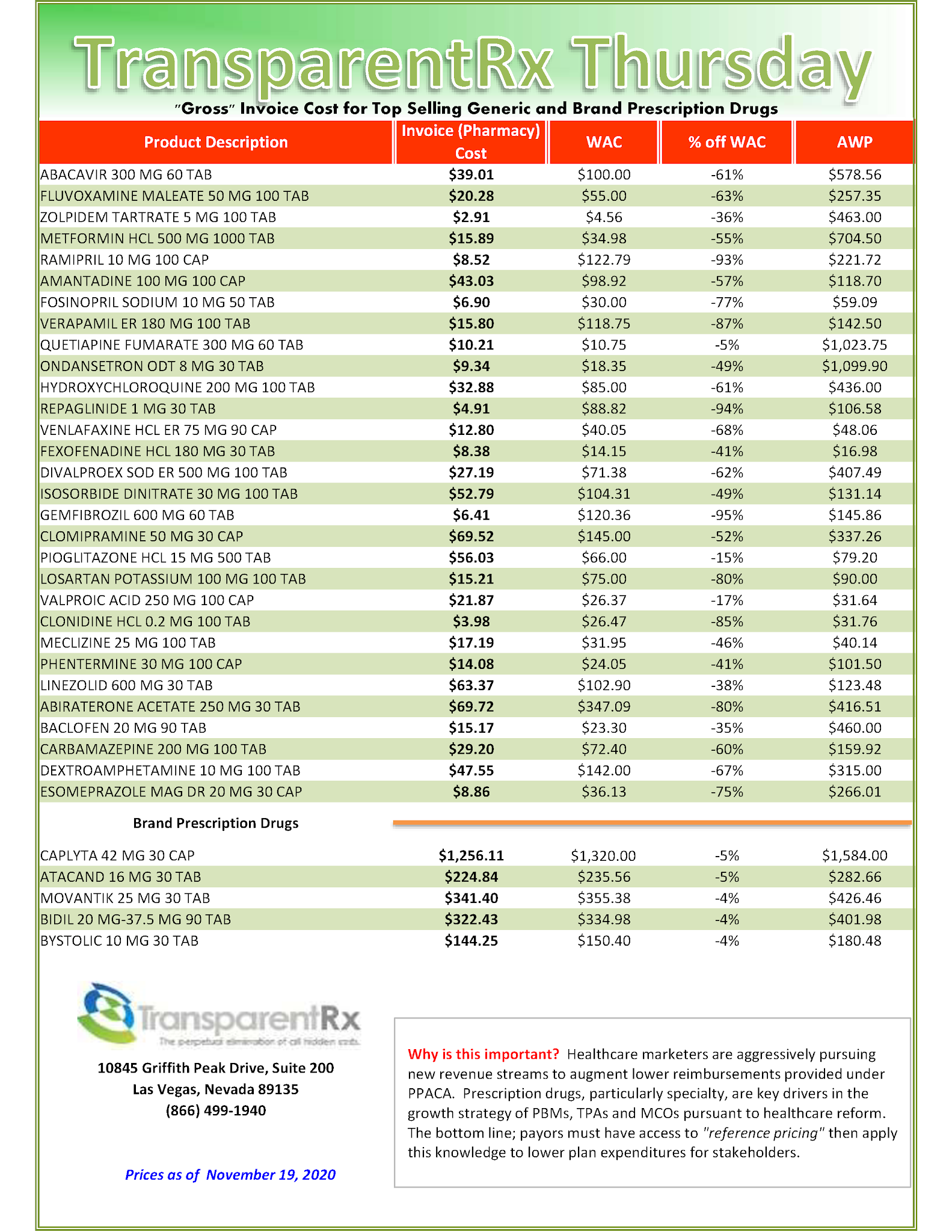

What is a Copay Accumulator Program and How Does It Work?

A copay accumulator – or accumulator adjustment program – is a strategy used by insurance companies and Pharmacy Benefits Managers (PBMs) that stop manufacturer copay assistance coupons from counting towards two things: 1) the deductible and 2) the maximum out-of-pocket spending. What does this mean?

Previously, a person could receive financial assistance from companies that make a drug, and that would count towards their deductible and/or out-of-pocket costs, depending upon the insurance plan. Pharmaceutical companies often provide financial assistance (such as a co-pay card) to help underinsured individuals afford expensive medications. This means that the person paying for the drug would end up saving money, often thousands of dollars.

Why Is This an Issue?

As the AIDS Institute explains it, “ … the trend in health insurance benefit design is to shift more of the cost of health care to patients through high deductibles and coinsurance rates …In order to afford the medicine they need, patients increasingly rely on manufacturer copay assistance.”

Tyrone’s Commentary:

Blanket statements like, “with copay accumulators, the individuals who need assistance the most will be unable to receive it, and will end up paying more for their treatments” are misleading. In many cases, the patients pay less than what was intended by the benefit design. But, if there was no actual out-of-pocket why should it [copay assistance] count toward the deductible? It seems no one will be happy until employers are on the hook for 100% of the cost.

As a copay program provider, TrialCard believes accumulators have a negative effect on a pharmaceutical manufacturer’s ability to deliver patient assistance for high-cost specialty medications, many of which do not have generic alternatives.

“We’ve been educating employer groups on the impact of copay accumulators beyond just financial savings tools and have analyzed their effects on employee productivity and long-term healthcare costs,” Zemcik explained. “Our role as a copay program provider working on behalf of our manufacturer clients is to help design their programs in a way that’s going to best address all of the complex issues.”