Rent-Seeking: A Traditional PBM’s Pathway to Riches

Rent-seeking is a term economists use to describe an organization’s ability to generate above average economic returns without providing any relative incremental value. Wikipedia may explain it a bit better.

Rent-seeking is a term economists use to describe an organization’s ability to generate above average economic returns without providing any relative incremental value. Wikipedia may explain it a bit better.

Wikipedia Definition

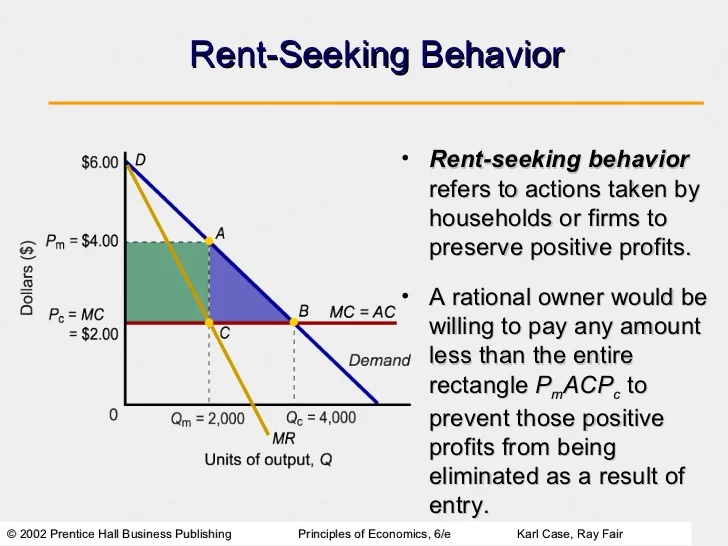

The simplest definition of rent-seeking is to expend resources in order to gain wealth by increasing one’s share of currently existing wealth instead of trying to create wealth. Since resources are expended but no new wealth is created, the net effect of rent-seeking is to reduce total social wealth. It is important to distinguish between profit-seeking and rent-seeking.

Profit-seeking is the creation of wealth, while rent-seeking is the use of social institutions such as the power of government to redistribute wealth among different groups without creating new wealth. Rent-seeking generally implies extraction of uncompensated value from others without making any contribution to productivity.

The origin of the term refers to gaining control of land or other pre-existing natural resources. In a modern economy, a more common example of rent-seeking would be political lobbying to obtain government benefits/subsidies or to impose burdensome regulations on competitors in order to increase market share.

Studies of rent-seeking focus on efforts to capture special monopoly privileges such as manipulating government regulation of free enterprise competition. The term monopoly privilege rent-seeking is an often-used label for this particular type of rent-seeking. Often-cited examples include a lobby that seeks tariff protection, quotas, subsidies, or extension of copyright law.

How does a traditional PBM employ a rent-seeking methodology?

Most recently, the FTC approved the acquisition of Medco by Express Scripts. The net effect of this purchase is not a creation of new wealth, but instead a reduction in social wealth. The FTC approval of this acquisition will ultimately benefit only the government, Express Script and Medco stockholders.

Patients won’t pay lower prices or see a real difference in their health care outcomes. Retail pharmacies and PBM competitors certainly won’t benefit from this acquisition. History tells us that greed will supersede social responsibility almost 100% of the time. Express Scripts has used the government, with powerful lobbying, to attain near monopolistic privileges.

Some state governments, Texas for example, require PBMs to take on the role of a fiduciary. The problem is that this requirement doesn’t extend to private enterprise. I say it’s a problem not because the government hasn’t interfered, but the opposite. Private enterprise hasn’t exercised its right to require a fiduciary role from their PBM. A transparent PBM, acting as a fiduciary, shares the risk and essentially agrees to be 100% transparent in all of its related business dealings.

This transparency includes sharing third party pricing contracts with pharmacies and rebates from manufacturers. It also includes offering real-time access to MAC price lists for retail and captive mail-order pharmacies. As specialty drugs become a larger part of the dispensing mix, it’s imperative to be fully aware of pricing arrangements between biotechnology companies as well. Here is an example of a typical fiduciary disclosure in a transparent PBM contract.